Fill Your G 45 Hawaii Template

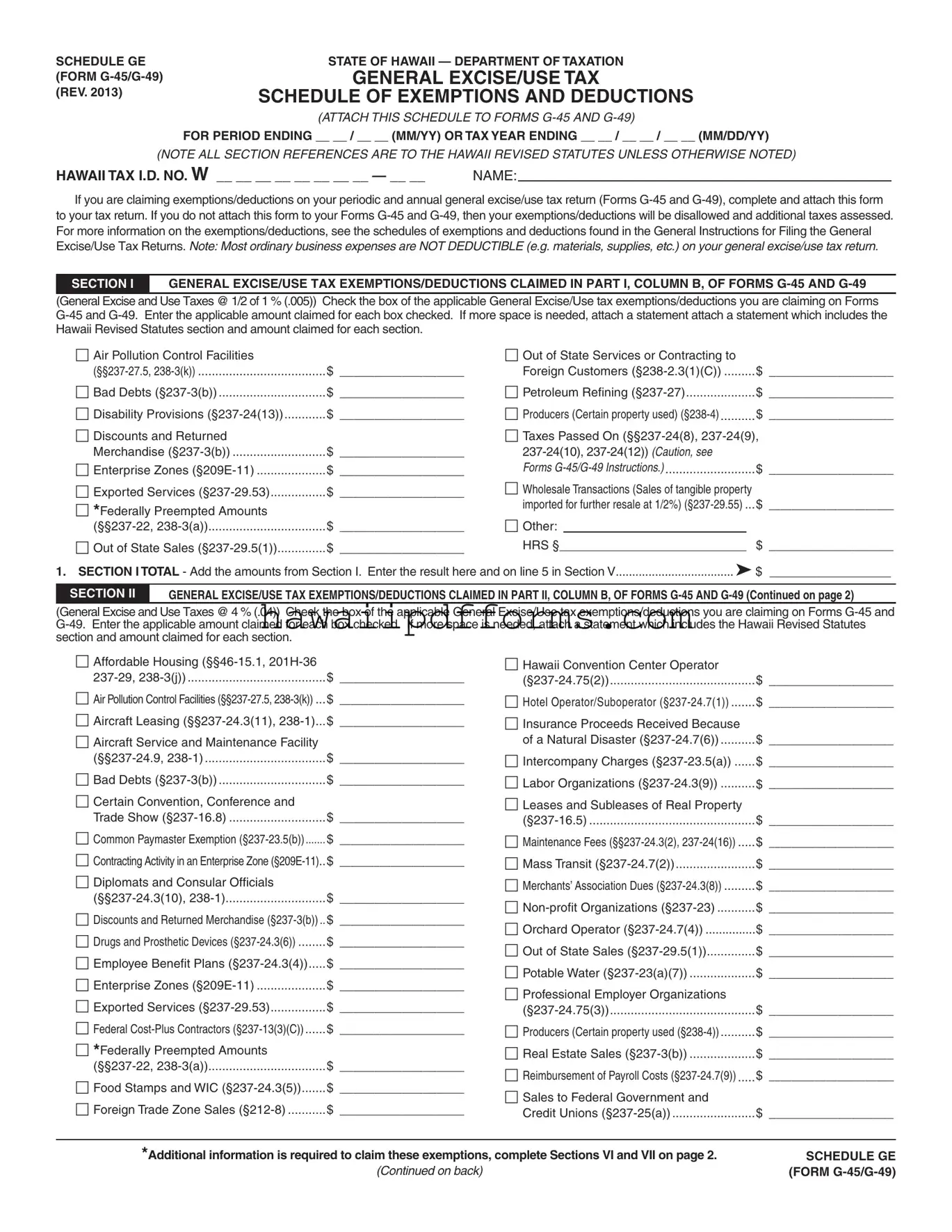

The G-45 Hawaii form, officially recognized as Schedule GE by the State of Hawaii Department of Taxation, represents a critical facet of tax documentation for entities conducting business within the state, primarily because it details the exemptions and deductions applicable to the general excise/use tax returns through Forms G-45 and G-49. This schedule itemizes various tax exemptions and deductions that businesses are eligible to claim, ranging from air pollution control facilities and bad debts to more specific inclusions like exported services and wholesale transactions. The necessity of attaching Schedule GE to Forms G-45 and G-49 cannot be understated; failure to do so results in the disallowance of these exemptions/deductions, leading to potential additional tax assessments. Moreover, it is imperative to note that most regular business expenses do not qualify as deductions under this tax category, highlighting the importance of understanding what expenses can be rightfully claimed. The form also includes requisite sections for detailed information regarding federally preempted amounts and subcontract deductions, underscoring the need for accurate reporting and substantiation of claims for exemptions. This document, updated for the 2013 revision, thus serves not only as a means to reduce taxable liability but also as a compliance requirement for businesses benefiting from Hawaii's varied tax exemption and deduction statutes.

Document Example

SCHEDULE GE |

STATE OF HAWAII — DEPARTMENT OF TAXATION |

(FORM |

GENERAL EXCISE/USE TAX |

(REV. 2013) |

SCHEDULE OF EXEMPTIONS AND DEDUCTIONS |

|

|

|

(ATTACH THIS SCHEDULE TO FORMS |

|

FOR PERIOD ENDING __ __ / __ __ (MM/YY) OR TAX YEAR ENDING __ __ / __ __ / __ __ (MM/DD/YY) |

(NOTE ALL SECTION REFERENCES ARE TO THE HAWAII REVISED STATUTES UNLESS OTHERWISE NOTED)

HAWAII TAX I.D. NO. W __ __ __ __ __ __ __ __ — __ __ |

NAME: |

If you are claiming exemptions/deductions on your periodic and annual general excise/use tax return (Forms

SECTION I GENERAL EXCISE/USE TAX EXEMPTIONS/DEDUCTIONS CLAIMED IN PART I, COLUMN B, OF FORMS

(General Excise and Use Taxes @ 1/2 of 1 % (.005)) Check the box of the applicable General Excise/Use tax exemptions/deductions you are claiming on Forms

Air Pollution Control Facilities |

|

Out of State Services or Contracting to |

|

|

|

|

||

$ __________________ |

Foreign Customers |

|

$ |

__________________ |

||||

Bad Debts |

$ __________________ |

Petroleum Refining |

|

$ |

__________________ |

|||

Disability Provisions |

$ __________________ |

Producers (Certain property used) |

|

$ |

__________________ |

|||

Discounts and Returned |

|

Taxes Passed On |

|

|||||

Merchandise |

$ __________________ |

|

|

|

|

|||

Enterprise Zones |

$ __________________ |

FORMS |

|

$ |

__________________ |

|||

Exported Services |

$ __________________ |

Wholesale Transactions (Sales of tangible property |

$ |

|

||||

*Federally Preempted Amounts |

|

imported for further resale at 1/2%) |

______________________ |

|||||

|

Other: |

|

|

|

|

|

||

$ __________________ |

|

|

|

|

|

|||

Out of State Sales |

$ __________________ |

HRS § |

|

|

|

$ |

__________________ |

|

|

|

|

||||||

1. SECTION I TOTAL - Add the amounts from Section I. Enter the result here and on line 5 in Section V |

$ |

__________________ |

||||||

SECTION II GENERAL EXCISE/USE TAX EXEMPTIONS/DEDUCTIONS CLAIMED IN PART II, COLUMN B, OF FORMS

(General Excise and Use Taxes @ 4 % (.04)) Check the box of the applicable General Excise/Use tax exemptions/deductions you are claiming on Forms

Affordable Housing |

|

Hawaii Convention Center Operator |

|

|

|

$ __________________ |

$ |

__________________ |

|||

|

|

||||

Air Pollution Control Facilities |

$ ______________________ |

Hotel Operator/Suboperator |

$ |

______________________ |

|

Aircraft Leasing |

$ __________________ |

Insurance Proceeds Received Because |

|

|

|

Aircraft Service and Maintenance Facility |

|

of a Natural Disaster |

$ |

__________________ |

|

$ __________________ |

Intercompany Charges |

$ |

__________________ |

||

Bad Debts |

$ __________________ |

Labor Organizations |

$ |

__________________ |

|

Certain Convention, Conference and |

|

Leases and Subleases of Real Property |

|

|

|

Trade Show |

$ __________________ |

$ |

__________________ |

||

|

|

||||

Common Paymaster Exemption |

$ ______________________ |

Maintenance Fees |

$ |

______________________ |

|

Contracting Activity in an Enterprise Zone |

$ ______________________ |

Mass Transit |

$ |

__________________ |

|

Diplomats and Consular Officials |

|

Merchants’ Association Dues |

$ |

______________________ |

|

$ __________________ |

|

$ |

__________________ |

||

Discounts and Returned Merchandise |

$ ______________________ |

||||

Orchard Operator |

$ |

__________________ |

|||

Drugs and Prosthetic Devices |

$ __________________ |

||||

Out of State Sales |

$ |

__________________ |

|||

Employee Benefit Plans |

$ __________________ |

||||

Potable Water |

$ |

__________________ |

|||

Enterprise Zones |

$ __________________ |

||||

Professional Employer Organizations |

|

|

|||

Exported Services |

$ __________________ |

|

|

||

$ |

__________________ |

||||

Federal |

$ ______________________ |

Producers (Certain property used |

$ |

__________________ |

|

*Federally Preempted Amounts |

|

Real Estate Sales |

$ |

__________________ |

|

$ __________________ |

Reimbursement of Payroll Costs |

______________________ |

|||

Food Stamps and WIC |

$ __________________ |

||||

Sales to Federal Government and |

|

|

|||

Foreign Trade Zone Sales |

$ __________________ |

|

|

||

Credit Unions |

$ |

__________________ |

|||

|

|

|

|||

*Additional information is required to claim these exemptions, complete Sections VI and VII on page 2. |

|

SCHEDULE GE |

|||

|

(Continued on back) |

|

|

(FORM |

|

SCHEDULE GE (FORM

Name

PAGE 2

Hawaii Tax I.D. Number |

Period Ending (MM/YY) or |

|

Tax Year Ending (MM/DD/YY) |

|

|

SECTION II GENERAL EXCISE/USE TAX EXEMPTIONS/DEDUCTIONS CLAIMED IN PART II, COLUMN B, OF FORMS

Scientific Contracts |

$ __________________ |

*Subcontract Deduction |

$ |

__________________ |

||||

Services Related to Ships and Aircraft |

|

Sugar Cane Payments to Independent |

|

|

|

|||

$ __________________ |

Producers |

$ |

__________________ |

|||||

Shipbuilding and Ship Repairs |

$ __________________ |

Taxes Passed On |

|

|

|

|||

Shipping and Handling of Agricultural |

|

|

|

|||||

|

______________________ |

|||||||

Commodities |

$ __________________ |

|||||||

|

|

|

|

|

|

|||

Small Business Innovation Research |

|

TRICARE |

$ |

__________________ |

||||

|

Wholesale Amusements |

$ |

__________________ |

|||||

Grants |

$ __________________ |

|||||||

Stock Exchange Transactions |

Other: |

|

|

|

|

|||

|

|

|

|

|||||

|

|

HRS § |

|

|

$ |

__________________ |

||

2. SECTION II TOTAL - Add the amounts from Section II. Enter the result here and on line 6 in Section V |

$ |

__________________ |

||||||

SECTION III GENERAL EXCISE/USE TAX EXEMPTIONS/DEDUCTIONS CLAIMED IN PART III, COLUMN B, OF FORMS

(Insurance Commissions taxed @ .15% (.0015)) Check the box of the applicable General Excise/Use tax exemptions/deductions you are claiming on Forms

Bad Debts |

$ __________________ |

Other: |

|

|

|

|

|

||

|

|

|

HRS § |

|

|

$ |

__________________ |

||

3. SECTION III TOTAL - Add the amounts from Section III. Enter the result here and on line 7 in Section V |

$ |

__________________ |

|||||||

|

|

||||||||

SECTION IV |

COUNTY SURCHARGE EXEMPTIONS/DEDUCTIONS CLAIMED IN PART IV, COLUMN B, OF FORMS |

||||||||

(City and County of Honolulu Surcharge Tax @ 1/2 of 1% (.005)) Select the County Surcharge Tax exemptions/deductions that you are claiming. Enter the total amount claimed for each exemption/deduction.

|

Certain Contracts Entered into Before |

|

Subleases of Real Property |

$ |

__________________ |

||

|

6/30/2006 |

$ __________________ |

Wholesale Amusements |

$ |

__________________ |

||

|

Certain Oahu Sales |

|

|||||

|

$ __________________ |

|

|

|

|

||

4. |

SECTION IV TOTAL - Add the amounts from Section IV. Enter the result here and on line 8 in Section V |

$ |

__________________ |

||||

|

|

|

|

|

|

||

|

SECTION V |

TOTAL EXEMPTIONS/DEDUCTIONS CLAIMED ON FORMS |

|

|

|

||

5. |

Section I Total - Enter the amount from Section I, line 1 |

|

$ |

__________________ |

|||

6. |

Section II Total - Enter the amount from Section II, line 2 |

|

$ |

__________________ |

|||

7. |

Section III Total - Enter the amount from Section III, line 3 |

|

$ |

__________________ |

|||

8. |

Section IV Total - Enter the amount from Section IV, line 4 |

|

$ |

__________________ |

|||

9. |

GRAND TOTAL. Add lines 5 through 8 and enter the result on this line and on Form |

|

|

|

|||

|

or Form |

|

$ |

__________________ |

|||

|

|

|

|

|

|

||

|

SECTION VI |

ADDITIONAL INFORMATION REQUIRED FOR FEDERALLY PREEMPTED AMOUNTS CLAIMED |

|

|

|

||

If the amount claimed is exempt due to federal preemption, provide an explanation of the exemption and the federal statute (i.e., title and section of the United States Code) under which the exemption is being claimed (If more space is needed, attach a statement):

SECTION VII |

ADDITIONAL INFORMATION REQUIRED FOR SUBCONTRACT DEDUCTIONS AMOUNTS CLAIMED |

If you are claiming an deduction for payments made to a subcontractor or a specialty contractor, complete the required information below:

(If more space is needed, attach a statement. Include the total subcontract deductions claimed from any attachments in the total line below.)

SUBCONTRACTOR’S NAME AND/OR DBA NAME

SUBCONTRACTOR’S HAWAII TAX I.D. NO.

AMOUNT OF DEDUCTION

TOTAL SUBCONTRACT DEDUCTIONS CLAIMED |

$ |

*Additional information is required to claim these exemptions, complete Sections VI and VII.

SCHEDULE GE (Form

Document Characteristics

| Fact Name | Description |

|---|---|

| Document Title | Schedule GE - General Excise/Use Tax Schedule of Exemptions and Deductions |

| Form Number | G-45/G-49 |

| Revision Year | 2013 |

| Purpose | For claiming exemptions/deductions on periodic and annual general excise/use tax returns in Hawaii |

| Requirement | Must be attached to Forms G-45 and G-49; otherwise, exemptions/deductions will be disallowed |

| Exemption/Deduction Types | Includes air pollution control facilities, out-of-state services, bad debts, disability provisions, amongst others |

| Governing Law | Hawaii Revised Statutes |

| Special Notes | Ordinary business expenses are not deductible; specific exemptions require additional information |

| Sections for Additional Information | Sections VI and VII for federally preempted amounts and subcontract deductions |

Guidelines on Utilizing G 45 Hawaii

For entities operating within Hawaii and eligible for certain exemptions or deductions on their general excise and/or use tax obligations, the G-45 form is a critical document. Proper completion and attachment of this form are requisite steps in the process of filing periodic and annual general excise/use tax returns, specifically forms G-45 and G-49. It's essential to understand which deductions and exemptions apply to a specific entity to avoid disallowed claims and resultant additional taxes. The form not only requires the identification of qualified exemptions or deductions but also necessitates accurate calculation and documentation of these financial figures.

Steps for Filling Out the G-45 Hawaii Form

- Begin by providing the period ending (MM/YY) or the tax year ending (MM/DD/YY) at the top of the form.

- Enter the Hawaii Tax I.D. No. in the designated space.

- Fill in the “Name” section with the registered name of the entity claiming the exemption or deduction.

- Review each section starting from SECTION I to IV to identify applicable exemptions or deductions. Check the box next to the applicable General Excise/Use tax exemptions/deductions you are claiming on Forms G-45 and G-49.

- For each checked exemption or deduction, enter the applicable amount claimed in the space provided.

- If additional space is required for documenting exemptions/deductions, attach a separate statement, including the Hawaii Revised Statutes section and the amount claimed for each section.

- In Section V, calculate the total exemptions/deductions claimed by adding the amounts from Section I through IV. Enter the totals in the respective lines provided.

- For federally preempted amounts, complete Section VI by providing an explanation of the exemption and the federal statute (title and section of the United States Code) under which the exemption is being claimed. If more space is needed, attach a separate statement.

- For subcontract deductions, complete Section VII with the required information for each subcontractor or specialty contractor, including their name, Hawaii Tax I.D. No., and the amount of deduction. Include the total subcontract deductions claimed at the end of this section.

- Confirm all entered information for accuracy. Ensure that all applicable sections are completed and attach the Schedule GE to your Forms G-45 and G-49 upon submission.

Once the G-45 form is accurately completed and attached, entities can confidently proceed with their submission, knowing they have efficiently documented their exemptions and deductions. This careful preparation supports compliance and optimizes the entity's tax positions related to general excise and use taxes in Hawaii.

Understanding G 45 Hawaii

FAQ: G-45 Hawaii Form - General Excise/Use Tax

-

What is the purpose of the G-45 Hawaii form?

The G-45 Hawaii form, also known as the General Excise/Use Tax Return, is essential for reporting periodic general excise tax and use tax. Attached to this form is Schedule GE, which specifically helps taxpayers to claim various tax exemptions or deductions that are applicable to their situation. It is crucial for businesses and individuals engaging in taxable activities in Hawaii to fill out and submit this form along with any claimed exemptions or deductions to ensure compliance with state tax obligations.

-

How do I claim exemptions or deductions on the G-45 form?

To claim exemptions or deductions on your General Excise/Use Tax Return (Form G-45), you must accurately complete and attach the Schedule GE. This schedule enables you to detail the specific exemptions or deductions you are claiming, based on the types of goods or services provided. It's important to check the applicable boxes for the exemptions/deductions being claimed and to enter the corresponding amounts. Additionally, if more space is needed or if you are claiming federally preempted amounts or subcontract deductions, you must provide the necessary additional information as outlined in Sections VI and VII of the schedule.

-

Are ordinary business expenses deductible on my general excise/use tax return?

No, most ordinary business expenses, such as costs for materials and supplies, are not deductible on your general excise/use tax return. The Form G-45 focuses on tax-exempt transactions rather than the deduction of business expenses. The schedule of exemptions and deductions (Schedule GE) is designed to list specific types of transactions or activities that are eligible for exemption from or reduction in tax, not to provide general business expense deductions.

-

What happens if I don't attach the Schedule GE to my G-45 or G-49 forms?

If you fail to attach the completed Schedule GE to your G-45 (periodic) or G-49 (annual) general excise/use tax return, your claimed exemptions or deductions may be disallowed. This oversight could result in the assessment of additional taxes. The Schedule GE is a critical part of your tax submission, serving as the documentation that supports your exemption and deduction claims. Therefore, ensuring that it is properly filled out and attached to your tax return is necessary to avoid unanticipated tax liabilities.

Common mistakes

When filling out the G-45 Hawaii form, several common errors are frequently encountered. These mistakes can lead to delays and potentially incorrect tax assessments. To ensure accurate and timely processing, individuals are encouraged to pay close attention to detail when completing their forms.

Not attaching the Schedule GE to Forms G-45 and G-49 is a common oversight. This schedule is essential for claiming any exemptions or deductions. Without it, the claimed exemptions and deductions will be disregarded, resulting in additional taxes being assessed.

Another misstep involves misdetermining which exemptions or deductions apply to their situation. Given the specific nature of exemptions, such as those for out-of-state sales or services and exported services, misunderstanding the criteria can lead to erroneous claims.

Incorrectly calculating the total exemptions and deductions at the end of each section and not transferring these totals accurately to the main forms (G-45 or G-49) can lead to inconsistencies in reported figures, affecting the tax liability.

Failing to provide additional required information for federally preempted amounts and subcontract deductions amounts claimed in Sections VI and VII, respectively. This oversight can invalidate an otherwise legitimate deduction or exemption, as the lack of detailed explanation or substantiation leaves the claim unsupported.

Overlooking the need to check the applicable boxes for each claimed exemption or deduction and not entering the corresponding amounts can result in an incomplete submission. This incomplete information might lead to the rejection of valid exemptions or deductions.

Being vigilant in avoiding these errors can significantly streamline the processing of the G-45 Hawaii form. Taxpayers should carefully review each section, ensure all applicable exemptions and deductions are properly claimed, and provide complete information to support their claims.

Documents used along the form

When managing taxes in Hawaii, particularly focusing on general excise and use tax, the Form G-45 is a crucial document. However, it's often not the only document needed to navigate through Hawaii's tax system. Various forms and documents complement the Form G-45, each serving a specific purpose, making tax reporting more accurate and tailored to individual circumstances. It’s important to familiarize oneself with these documents to ensure compliance with state tax laws and to take advantage of any applicable deductions and exemptions.

- Form G-49: This is the Annual Return & Reconciliation form. It summarizes the tax year's activity and reconciles the taxes paid quarterly or monthly on Form G-45 with the annual liability.

- Form G-6: The Application for Exemption from General Excise Taxes form is used by organizations to apply for tax-exempt status.

- Form BB-1: The State of Hawaii Basic Business Application is used to register with the Department of Taxation and other state agencies, a necessity for businesses starting up.

- Form G-75: This form documents sales allocated to each county, aiding in the calculation of county surcharge taxes.

- Form TA-1: The Transient Accommodations Tax Return is necessary for those offering short-term lodging, a common situation in Hawaii given its tourism industry.

- Form HW-14: This Withholding Tax Return is filed by employers to report tax withheld from employees’ wages.

Form N-200V:

This Payment Voucher for Hawaii Individual Income Tax is used when making an income tax payment separately from the tax return filing.VP-1:

The Vehicle and Vessel Owner’s Registration Information Update Form is utilized for updating the ownership information on the registration records for tax purposes related to vehicle and vessel transactions.- Form U-6: Report of Sales of Tangible Personal Property Outside Hawaii is crucial for businesses conducting sales outside of Hawaii, ensuring accurate reporting and exemption claims for out-of-state sales.

Understanding and utilizing these forms, along with the Schedule GE attached to Form G-45 (General Excise/Use Tax Return), will not only ensure compliance with Hawaii's tax regulations but also help in managing the tax liabilities and deductions more effectively. It's important to consult with a tax professional to make sure that all forms are completed correctly and filed on time. Whether you are a small business owner, a new entrepreneur, or an individual taxpayer, being proactive about tax responsibilities protects you against unforeseen penalties and helps in financial planning.

Similar forms

The G-45 Hawaii form is notably similar to other state tax exemption and deduction forms, which serve as attachments to the main tax return filings. These forms are designed to provide detailed information on specific exemptions or deductions the taxpayer is claiming. Their structure and purpose have considerable overlap with forms used in various jurisdictions for similar tax purposes.

For instance, the Schedule A (Form 1040), used for itemizing deductions on the federal income tax return, shares a functional similarity. Both forms require the taxpayer to list specific deductions or exemptions they're claiming, offering a detailed breakdown that supports the figures entered on the main tax form. However, Schedule A focuses on personal income tax deductions such as mortgage interest, medical expenses, and charitable contributions, contrasting with the G-45's emphasis on business-related exemptions and deductions.

Another parallel can be drawn with California’s Sales and Use Tax Return, as both forms address the taxes imposed on the sale and consumption of goods and services. Each form allows businesses to claim exemptions or deductions on taxable activities, specifying amounts that adjust the tax owed. Key differences lie in their geographical applicability and specific types of exemptions covered, tailored to the legal and economic environment of the respective state.

The similarity extends to the Form ST-5 Sales Tax Exempt Purchaser Certificate used in states like Massachusetts. This form is provided by tax-exempt entities when purchasing goods, to exempt them from sales tax at the point of sale. It pertains to exemption at the transaction level rather than cumulative deductions over a tax period. Nonetheless, both forms play pivotal roles in the administration of tax exemptions within their specific frameworks.

Dos and Don'ts

Filling out the G-45 Hawaii form, a document crucial for reporting general excise/use tax, requires attention to detail and an understanding of the relevant tax exemptions and deductions. Below are the recommended dos and don'ts to ensure the process is both efficient and effective.

Dos:

Ensure all information is accurate and complete before submission. Incorrect details can lead to unnecessary delays or the rejection of the form.

Identify and understand the specific exemptions and deductions that apply to your situation. This will help maximize your potential savings and ensure compliance with Hawaii tax laws.

Attach the required schedules and documents that substantiate your claims for exemptions and deductions. Failure to do so may result in disallowed claims.

Use the correct tax identification number and business name as registered with the Hawaii Department of Taxation to prevent processing errors.

Review the form and attached documents for accuracy before submitting them to the Hawaii Department of Taxation.

Keep a copy of the completed form and all supporting documents for your records. These may be needed for future reference or in case of an audit.

Be aware of the submission deadlines to avoid penalties and interest for late filings.

Don'ts:

Do not overlook the additional information required for claiming federally preempted amounts and subcontract deductions. Incomplete sections can lead to disqualification of the claimed exemption.

Avoid guessing when filling out the form. If you are unsure about a specific section, it's better to seek clarification from a tax professional or the Hawaii Department of Taxation.

Do not claim ordinary business expenses as deductions or exemptions on this form. The G-45 form does not allow deductions for such expenses.

Refrain from submitting the form without checking the applicable exemption and deduction boxes in Section I and II, as applicable. Failing to check these boxes might lead to missed benefits.

Do not ignore the instructions provided in the form. They are designed to guide you through the process and help you comply with the filing requirements.

Avoid delays in submitting any additional statements or documents required to support your exemptions or deductions if the space provided on the form is insufficient.

Do not underestimate the importance of the County Surcharge Exemptions/Deductions if your business transactions are relevant to such surcharges.

Misconceptions

When it comes to completing and filing the G-45 Hawaii form, a variety of misconceptions can lead people astray. Understanding these misconceptions is key to correctly claiming exemptions and deductions on your general excise/use tax returns.

- Misconception #1: All business expenses are deductible. Many people mistakenly believe that all typical business expenses can be deducted on the G-45 form. However, the reality is most ordinary business expenses, like costs for materials and supplies, do not qualify as deductions under the general excise/use tax.

- Misconception #2: Filing the Schedule GE is optional. Another common misunderstanding is that completing and attaching the Schedule GE to your Forms G-45 and G-49 is not mandatory. In truth, if the Schedule GE is not attached, any claimed exemptions or deductions will be disallowed, potentially resulting in additional taxes being assessed.

- Misconception #3: Exemptions and deductions apply at the same rate. Some taxpayers assume that the exemptions and deductions they claim will apply across the board at a single rate. In reality, different types of transactions are taxed at varying rates, and the exemptions/deductions that apply might differ in percentage based on the nature of the transaction.

- Misconception #4: Federally preempted amounts do not require additional documentation. It is often presumed that if an amount is exempt due to federal preemption, simply checking a box is sufficient. Yet, detailed information about the federal exemption and relevant statutes must be provided on the form or via attached documentation.

- Misconception #5: All sales outside of Hawaii are exempt from general excise tax. While certain out-of-state sales and services are exempt from Hawaii's general excise tax, not all interstate or foreign sales are automatically exempt. Detailed criteria determine taxability, including the nature of the service provided and how the transaction is conducted.

Correctly understanding and applying the rules surrounding the G-45 form ensures that businesses can take advantage of applicable exemptions and deductions without inadvertently increasing their tax liability. Always consult the general instructions or a tax professional for assistance with specific situations.

Key takeaways

When completing the G-45 Hawaii Form, it's crucial to understand some key points about exemptions and deductions to ensure accurate filing:

- Always attach Schedule GE to Forms G-45 and G-49 when claiming any exemptions or deductions. Failing to do so will result in the disallowance of these claims, leading to potential additional tax assessments.

- Making a claim for exemptions or deductions requires checking the appropriate boxes in Section I or Section II of the form and entering the amount claimed for each exemption or deduction selected.

- Ordinary business expenses, such as costs for materials and supplies, cannot be deducted on your general excise/use tax return. This highlights the specific nature of allowable exemptions and deductions under Hawaii tax law.

- If the space provided is insufficient for listing all your exemptions or deductions, you're allowed to attach an additional statement. This statement should include the necessary details, like the Hawaii Revised Statutes section and the associated amount claimed for each section.

- Certain exemptions require additional information to be provided, specifically federally preempted amounts and subcontract deductions. Sections VI and VII on page 2 are dedicated to these details, and should be completed if relevant to your claims.

- In addition to understanding deductions for general excise and use taxes, filers must also be aware of county surcharge exemptions/deductions if operating within applicable areas like the City and County of Honolulu. This is detailed in Section IV of the schedule.

- The completed Form G-45 Hawaii allows for a clear presentation of all exemptions and deductions being claimed. It's important to add these up correctly and enter the totals in the specified lines in Section V to ensure your returns are accurate and complete.

Accurately filling out the G-45 Hawaii form and its attachments is essential for correctly reporting your tax obligations and taking advantage of permissible exemptions and deductions. Remember that each deduction or exemption claimed must be properly documented and justifiable under Hawaii's tax laws.

Create Common PDFs

Restraining Order Hawaii - Violation of the temporary restraining order is considered a misdemeanor with specified penalties.

Divorce Papers Hawaii - Structured to clarify the responsibilities regarding alimony, with options for its disbursement and termination conditions.