Fill Your Hawaii G 17 Template

When navigating the intricacies of business transactions in Hawaii, the Form G-17, issued by the State of Hawaii's Department of Taxation, plays a pivotal role, particularly for those engaged in the sale of goods. This comprehensive form serves as a resale certificate, allowing businesses to purchase goods without paying sales tax at the time of purchase, under the condition that the items are to be resold in the normal course of operations. As such, it acts as a tangible link between the purchaser and seller, ensuring compliance with the General Excise Tax Law of Hawaii. The form encapsulates crucial information, such as the purchaser's Hawaii Tax Identification Number, the nature of the purchaser’s business, and a declaration that all purchases made using this certificate are intended for resale, either at retail or wholesale. Additionally, it obligates the purchaser to compensate the seller for any additional taxes imposed due to transactions covered by the certificate. It's important to note that this form, once filled and signed, should be retained by the seller for record-keeping purposes and not sent to the Department of Taxation, emphasizing the trust-based nature of tax compliance in the state. With penalties outlined for misrepresentation, the Form G-17 underscores the legal and financial responsibilities of both parties in the transaction chain.

Document Example

FORM |

STATE OF HAWAII — DEPARTMENT OF TAXATION |

|

(REV. 2016) |

||

|

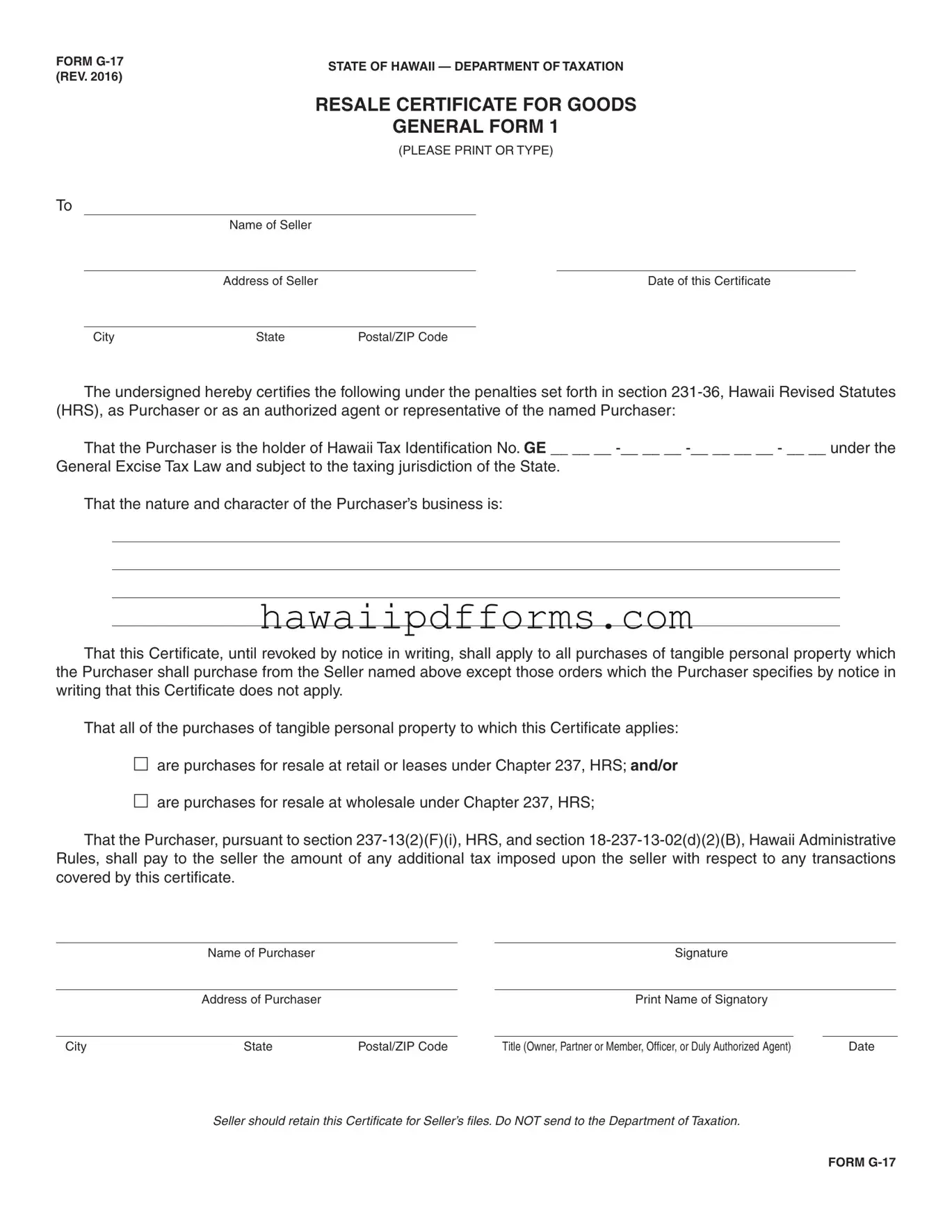

RESALE CERTIFICATE FOR GOODS

GENERAL FORM 1

(PLEASE PRINT OR TYPE)

To

Name of Seller

|

Address of Seller |

|

Date of this Certificate |

|

|

|

|

City |

State |

Postal/ZIP Code |

|

The undersigned hereby certifies the following under the penalties set forth in section

That the Purchaser is the holder of Hawaii Tax Identification No. GE __ __ __

That the nature and character of the Purchaser’s business is:

That this Certificate, until revoked by notice in writing, shall apply to all purchases of tangible personal property which the Purchaser shall purchase from the Seller named above except those orders which the Purchaser specifies by notice in writing that this Certificate does not apply.

That all of the purchases of tangible personal property to which this Certificate applies:

are purchases for resale at retail or leases under Chapter 237, HRS; AND/OR

are purchases for resale at wholesale under Chapter 237, HRS;

That the Purchaser, pursuant to section

|

Name of Purchaser |

|

|

Signature |

|

|

|

|

|

|

|

|

|

|

|

|

Address of Purchaser |

|

|

Print Name of Signatory |

|

|

|

|

|

|

|

|

|

|

|

City |

State |

Postal/ZIP Code |

|

Title (Owner, Partner or Member, Officer, or Duly Authorized Agent) |

|

Date |

|

Seller should retain this Certificate for Seller’s files. Do NOT send to the Department of Taxation.

FORM

Document Characteristics

| Fact | Details |

|---|---|

| Form Name and State | Form G-17, Hawaii |

| Issuing Department | Department of Taxation |

| Form Revision Year | 2016 |

| Purpose | Resale Certificate for Goods General Form |

| Key Use | Allows the purchaser to buy tangible personal property for resale without paying general excise tax at the time of purchase. |

| Governing Laws | Hawaii Revised Statutes (HRS) Section 231-36 for penalties; Chapter 237, HRS for resales; and Section 18-237-13-02(d)(2)(B), Hawaii Administrative Rules for applicable taxes. |

Guidelines on Utilizing Hawaii G 17

Once you've determined that a purchase or series of purchases qualify for the use of the Hawaii G-17 form, completing it accurately becomes a critical step. This certificate helps businesses in Hawaii manage tax obligations related to resale activities more effectively. It effectively communicates to sellers that the purchase falls under specific tax exemptions as outlined by Hawaii tax laws. Here are the step-by-step instructions to fill out the form correctly, ensuring both clarity and compliance.

- Start by entering the Name of Seller in the designated space. This should be the business name of the company from which you are purchasing goods for resale.

- Fill in the Address of Seller section with the business address of the seller, making sure to include the city, state, and postal/ZIP code.

- Indicate the Date of this Certificate on which the form is being filled out to ensure the document is timely and relevant.

- Under "The undersigned hereby certifies the following," enter your Hawaii Tax Identification No. This is a critical identification number that ties the certificate to your business and its tax obligations.

- Describe the nature and character of the Purchaser’s business in the space provided. This helps establish the context for the purchase and its intended use in your operations.

- Tick the appropriate box(es) under the section that starts with "That all of the purchases of tangible personal property to which this Certificate applies" to specify whether the goods are for resale at retail or for resale at wholesale, as outlined under Chapter 237, HRS.

- In the section meant for the Purchaser’s information, fill in the Name of Purchaser, ensuring it matches the name registered with your Hawaii Tax Identification No.

- Sign the certificate in the space provided next to Signature. This indicates your agreement and certification of the information provided as accurate and true.

- Next to the signature, print the Name of Signatory for clarity on who has completed and signed the form on behalf of the purchasing business.

- Fill in your business address details under Address of Purchaser, including city, state, and postal/ZIP code.

- Last, specify the Title of the individual signing the form (e.g., Owner, Partner or Member, Officer, or Duly Authorized Agent) and the Date the form was filled out and signed.

Keep in mind, after completing the form, it should be retained with the seller’s records and not sent to the Department of Taxation. This form serves as part of the documentation that both parties may need to demonstrate compliance with tax regulations during audits or reviews. Making sure the information is accurate and thoroughly completed will safeguard against potential issues down the line.

Understanding Hawaii G 17

What is a Hawaii G 17 form?

The Hawaii G 17 form, also known as a Resale Certificate for Goods General Form, is a document issued by the State of Hawaii Department of Taxation. Businesses use it to inform sellers that the purchase of tangible personal property is for resale, thereby exempting the sale from the general excise tax at the point of purchase. The buyer is certifying that they will resell the items purchased and that they hold a valid Hawaii Tax Identification Number under the General Excise Tax Law.

Who needs to fill out the Hawaii G 17 form?

Any business that purchases goods for resale in Hawaii and wants to be exempt from paying general excise tax at the time of purchase needs to fill out the form. This includes businesses purchasing items for resale at retail or wholesale. The form must be completed by the purchaser or an authorized agent or representative of the purchasing business.

What information is required on the G 17 form?

- Hawaii Tax Identification Number of the purchaser

- Nature and character of the purchaser’s business

- Name and address of the seller

- Date of the certificate

- Signature, printed name, title, and address of the purchaser or authorized signatory

How does a business become eligible to use the G 17 form?

To use the G 17 form, a business must be registered with the Hawaii Department of Taxation and hold a valid General Excise Tax License. The business should be engaged in reselling tangible personal property and must be in compliance with all state tax laws.

Is the G 17 form applicable for services?

No, the G 17 form is specifically designed for transactions involving tangible personal property. It does not apply to purchases of services. For services, other tax provisions and forms may apply.

Can the G 17 form be revoked?

Yes, the purchaser can revoke the certificate at any time by providing written notice to the seller. This means that future purchases from the seller will not be covered by the certificate unless a new form is submitted.

What are the responsibilities of the seller when accepting a G 17 form?

Sellers are required to retain the completed G 17 form for their records but should not send it to the Department of Taxation. They should verify the validity of the purchaser’s Hawaii Tax Identification Number and ensure that the form is fully completed before accepting it. The seller is also responsible for charging the additional tax imposed on any transaction not covered by the certificate, as indicated by the purchaser.

What are the penalties for misuse of the G 17 form?

Using the G 17 form improperly, such as claiming exemption for items not intended for resale or providing false information, can lead to penalties under section 231-36 of the Hawaii Revised Statutes (HRS). These penalties may include fines and possible criminal charges.

How long is the G 17 form valid?

The G 17 form remains in effect until it is revoked in writing by the purchaser. There is no set expiration date, but businesses should ensure the information, especially the Hawaii Tax Identification Number, remains current.

Where can businesses obtain the G 17 form?

Businesses can download the G 17 form from the Hawaii Department of Taxation’s website or request a copy from the department directly. It's important to use the most current version of the form, which, as of the last update, is the 2016 revision.

Common mistakes

Filling out the Hawaii G-17 form, also known as the Resale Certificate for Goods, requires attention to detail. Here are 10 common mistakes people often make when completing this form:

-

Not printing or typing: The form clearly requests that all information be either printed or typed, which ensures legibility.

-

Incorrect Hawaii Tax Identification No.: This is a crucial detail which identifies the purchaser's business operation under the General Excise Tax Law in Hawaii.

-

Omitting the nature and character of the business: Providing an accurate description of the business is vital because it helps to determine the applicability of the certificate to the purchases made.

-

Incorrect or missing dates: The certificate must have an accurate date to establish the period for which the certificate applies.

-

Not specifying purchases that the certificate does not apply to: If certain purchases are not for resale, this needs to be mentioned in writing outside of this form.

-

Failing to check the appropriate box for the type of resale activity: This clarifies whether purchases are intended for resale at retail, wholesale, or for lease.

-

Neglecting to sign the Certificate: A signature is mandatory, validating the form as accurately completed and agreed to under penalties mentioned.

-

Not including the title of the signatory (Owner, Partner, Officer, or Agent): This confirms the authority of the person signing the document.

-

Failure to provide complete address information: Both the purchaser and the seller's address details are important for record-keeping and future communication.

-

Leaving out the obligation to pay additional tax: The purchaser acknowledges responsibility to pay any additional tax imposed upon the seller for transactions covered by this certificate.

Avoiding these mistakes can streamline business processes between purchasers and sellers, ensuring compliance with Hawaii's tax laws. Keeping a copy of the filled-out form for records is a best practice that every seller should follow, as recommended by the Department of Taxation.

Documents used along the form

When dealing with business transactions in Hawaii, especially those involving resale, the Hawaii G-17 form plays a crucial role. This document, required by the Department of Taxation, is just one piece of documentation among many that businesses might need. The following forms and documents often accompany the G-17 form to ensure compliance with Hawaii's tax laws and business regulations.

- Form G-45: Periodic General Excise / Use Tax Return - This form is used by businesses to report and pay the general excise tax on a periodic basis, often quarterly or semi-annually.

- Form G-49: Annual Return & Reconciliation of General Excise / Use Tax - Filed annually, this form reconciles the taxes paid throughout the year with the actual tax liability.

- Form BB-1: Basic Business Application - Required for all new businesses in Hawaii, this form registers the business with the state for tax purposes.

- Form G-6: Application for Exemption from General Excise Taxes - For organizations that are eligible for tax exemptions, detailing the nature of the exemption claimed.

- Form TA-1: Transient Accommodations Tax Registration - Necessary for businesses providing short-term lodging, registering them for the transient accommodations tax.

- Form VP-1: Vehicle Registration and Licensing - Essential for businesses requiring vehicle registration for operational purposes.

- Form HW-4: Employee's Withholding Allowance and Status Certificate - Used by employees to determine state income tax withholding.

- Form UC-B6: Quarterly Wage, Contribution and Employment and Training Assessment Report - Filed by employers to report wages, unemployment insurance contributions, and other related assessments.

- Form W-2: Wage and Tax Statement - An annual report detailing employees' earnings, as well as taxes withheld from their paychecks, mandatory for every employee.

Each of these forms and documents serves a specific function, from registering a new business to complying with tax obligations. Collectively, they ensure that businesses operate smoothly within the legal framework of Hawaii's commercial landscape. While handling these documents may seem daunting, they are essential for maintaining good standing with the state's Department of Taxation and other regulatory entities.

Similar forms

The Hawaii G-17 form is similar to other tax exemption or resale certificates used in various jurisdictions, each designed to document and facilitate transactions exempt from sales tax based on the nature of the purchase, namely for resale purposes. These documents are crucial for businesses engaged in retail and wholesale operations, ensuring compliance with tax laws and regulations while avoiding unnecessary tax burdens on goods that are meant for further sale.

Uniform Sales & Use Tax Exemption/Resale Certificate - Multijurisdiction: This certificate is similar to the Hawaii G-17 form in purpose, as it is also used by purchasers to buy goods tax-free for resale. However, the Multijurisdiction version is designed for use across multiple states, making it more versatile for businesses operating in more than one state. It covers the same basic declarations as the G-17 form, such as the nature of the purchaser's business and the intent to resell the purchased goods. The primary difference lies in its broader acceptance, which simplifies the purchasing process for businesses active in several states.

California Resale Certificate (BOE-230): Like Hawaii's G-17 form, California’s BOE-230 allows purchasers to buy goods without paying state sales tax if those goods are intended for resale. Both forms require similar information from the purchaser, including a declaration of intent to resell the goods and details about the purchaser’s business. The primary distinction between the two forms is their legal and tax jurisdiction, with the BOE-230 specifically addressing California's tax laws.

New York State Resale Certificate (ST-120): The ST-120 form serves a comparable purpose to the G-17, enabling purchasers to acquire goods tax-free for the purpose of resale. Both documents ensure that sales tax is only applied to the final consumer, not at intermediary stages of the sales process. The ST-120, like the G-17, requires purchasers to provide specific information about their business and the nature of the transaction. The critical difference is the adaptation to comply with New York's tax regulations, including specific certification that the purchaser is registered for New York State sales tax purposes.

Dos and Don'ts

Completing the Hawaii G-17 Resale Certificate accurately is crucial for compliance with tax laws. Follow these guidelines to ensure the process is done correctly.

What You Should Do:- Provide complete information: Fill in all required fields, including the purchaser’s Hawaii Tax Identification Number, business nature, and complete contact information for both the purchaser and the seller.

- Print or type legibly: Ensure all information is clear and easy to read to avoid misunderstandings or processing delays.

- Check applicable boxes: Indicate whether purchases are for resale at retail, leases under Chapter 237, HRS, and/or for resale at wholesale.

- Sign the certificate: The purchaser or an authorized agent must sign the certificate to validate it.

- Retain a copy: Sellers should keep the certificate on file and not send it to the Department of Taxation.

- Update as necessary: If there are changes in the information provided or if the certificate needs to be revoked, send written notice to the seller.

- Understand applicable laws: Familiarize yourself with the relevant Hawaii Revised Statutes (HRS) and Hawaii Administrative Rules to ensure compliance.

- Leave fields blank: Incomplete forms may not be legally valid or could delay transactions.

- Use unclear handwriting: If the form is not typed, ensure handwritten information is neatly written and understandable.

- Forget to indicate the purchase type: Forgetting to check the correct boxes regarding the nature of purchases could lead to tax compliance issues.

- Omit the signature: An unsigned form is not valid for its intended purpose.

- Send the certificate to the wrong place: Remember, the certificate should be retained by the seller and not sent to the Department of Taxation.

- Ignore changes in business status: Not updating the certificate for changes like address or tax ID number could invalidate the form.

- Disregard tax obligations: Not paying attention to tax implications and obligations related to transactions covered by this certificate can result in penalties.

Misconceptions

Understanding the Hawaii G-17 form can sometimes be confusing, leading to misconceptions. It's essential to clarify these misunderstandings to ensure compliance with Hawaii's tax laws. Here are nine common misconceptions about the G-17 form and the actual facts:

It's only for big businesses: The G-17 form is applicable to all businesses, regardless of size, that engage in resale activities. Both small and large businesses must use it when purchasing goods for resale to document that the purchase is exempt from general excise tax.

One-time use: Actually, the G-17 form, once submitted to a seller, covers all future purchases unless specifically revoked. Businesses do not need to submit a new form for every transaction.

It exempts the buyer from all taxes: The form only exempts the purchaser from paying general excise tax on items purchased for resale. It does not exempt other types of taxes that may apply to the business.

Applies to services: The G-17 form is designed for tangible personal property. It does not apply to services, even if those services are for resale.

It's complex to fill out: While the form must be filled out correctly, it requires standard information about the purchaser's business and an acknowledgment of the purpose of purchases. Most businesses find it straightforward to complete.

Only the business owner can sign it: The form can be signed by the owner, partner, member, officer, or a duly authorized agent of the business. The key is the person signing has the authority to do so on behalf of the business.

It needs to be filed with the Department of Taxation: The seller retains the G-17 form. There is no requirement to send it to the Hawaii Department of Taxation.

Online sellers don't need to use it: The G-17 form applies to all types of sellers, including online sellers, when selling goods meant for resale within Hawaii. The platform of sale does not affect the requirement.

Using the form incorrectly has no penalties: Incorrect usage of the G-17 form can lead to penalties under the penalties set forth in section 231-36, Hawaii Revised Statutes (HRS). It's crucial to understand and accurately apply the form to avoid any legal consequences.

Clearing up misconceptions about the Hawaii G-17 form can help businesses better navigate tax regulations and ensure compliance. Understanding the correct use and requirements of the form is beneficial for all businesses engaged in resale activities in Hawaii.

Key takeaways

When dealing with the Hawaii G-17 form, there are several key aspects to keep in mind for both buyers and sellers. This form is designed to facilitate the process of buying and selling goods intended for resale, and understanding its proper use is vital for compliance with Hawaii's tax laws.

- Verification of the purchaser's tax status: The G-17 form requires the purchaser to provide their Hawaii Tax Identification Number, confirming their registration under the General Excise Tax Law. This step is crucial for the seller to ensure that the sale can legally be considered exempt from retail sales tax, as it is intended for resale.

- Specific application: This form, once filled out and signed, applies to all future purchases of tangible personal property made by the purchaser from the seller, except where the purchaser specifies otherwise in writing. This ongoing applicability can streamline transactions but requires both parties to keep accurate records.

- Purchases covered: It is important to note that the form clearly distinguishes the nature of the purchases covered. Purchases made with this certificate can be either for resale at retail or for resale at wholesale under Chapter 237 of the Hawaii Revised Statutes. This distinction is important for ensuring that the proper tax treatment is applied to each transaction.

- Responsibility for additional taxes: The form stipulates that if any additional tax is imposed on the seller for transactions covered by the certificate, the purchaser agrees to pay this additional amount. This provision is in place to protect sellers from being left liable for unanticipated taxes resulting from sales made under this certificate.

Create Common PDFs

Dogs in Hawaii - As a proactive measure, the form helps maintain Hawaii's status as a safe and desirable destination by carefully managing health risks among arrivals.

Hawaii Marriage Certificate - This application is crucial for non-residents of Hawaii, ensuring their marriage is valid and recognized.

Restraining Order Hawaii - It helps streamline the process of seeking protection from harassment for residents of Hawaii.