Fill Your Hawaii Hw 14 Template

Navigating the complexities of tax obligations in Hawaii can feel overwhelming, especially when dealing with the HW-14 form, a critical document for employers across the state. This form, revamped for 2019 by the Hawaii Department of Taxation, is indispensable for reporting withholding taxes accurately and on time. Employers must file this return quarterly, adhering to the deadline which falls on the 15th day of the month following each quarter's end. It provides a structured way to report total wages paid—including special considerations like cost of living adjustments and third-party sick leave—alongside the total Hawaii income tax withheld from employees. Notably, the HW-14 form also accommodates those marking their final return and intention to cancel their withholding account. Instructions for attaching payment by check or money order are clear, emphasizing the convenience of also using e-pay options available through the state’s tax website. In cases of late filing, the form outlines the process for calculating penalties and interest due, ensuring employers can reconcile their accounts accurately. Through the precise details captured on this form, the Department of Taxation aims to streamline the process, making tax filing as hassle-free as possible for businesses of all sizes.

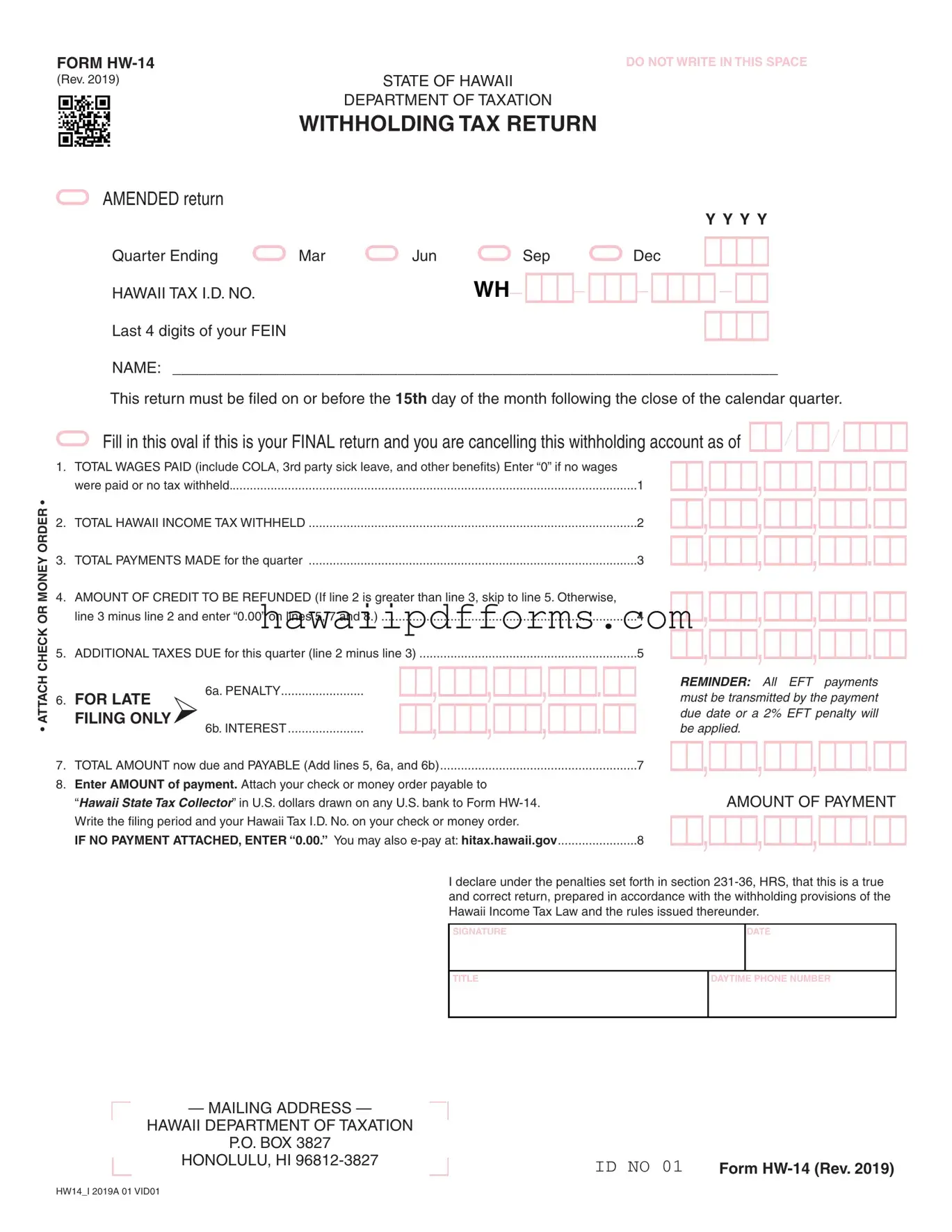

Document Example

FORM |

|

|

|

|

(Rev. 2019) |

|

STATE OF HAWAII |

|

|

|

|

DEPARTMENT OF TAXATION |

|

|

|

WITHHOLDING TAX RETURN |

|

||

AMENDED return |

|

|

|

|

|

|

|

|

Y Y Y Y |

Quarter Ending |

Mar |

Jun |

Sep |

Dec |

HAWAII TAX I.D. NO. |

|

WH |

|

|

Last 4 digits of your FEIN |

|

|

|

|

NAME: ______________________________________________________________________

This return must be filed on or before the 15th day of the month following the close of the calendar quarter.

• ATTACH CHECK OR MONEY ORDER •

Fill in this oval if this is your FINAL return and you are cancelling this withholding account as of

1. |

TOTAL WAGES PAID (include COLA, 3rd party sick leave, and other benefits) Enter “0” if no wages |

|

|

|

were paid or no tax withheld |

1 |

|

2. |

TOTAL HAWAII INCOME TAX WITHHELD |

2 |

|

3. |

TOTAL PAYMENTS MADE for the quarter |

3 |

|

4. |

AMOUNT OF CREDIT TO BE REFUNDED (If line 2 is greater than line 3, skip to line 5. Otherwise, |

|

|

|

line 3 minus line 2 and enter “0.00” on lines 5, 7 and 8.) |

4 |

|

5. |

ADDITIONAL TAXES DUE for this quarter (line 2 minus line 3) |

5 |

|

|

|

|

REMINDER: All EFT payments |

|

|

6a. PENALTY |

|

6. |

FOR LATE |

|

must be transmitted by the payment |

|

|

|

due date or a 2% EFT penalty will |

|

FILING ONLY6b. INTEREST |

be applied. |

|

7. |

TOTAL AMOUNT now due and PAYABLE (Add lines 5, 6a, and 6b) |

7 |

|

8. |

Enter AMOUNT of payment. Attach your check or money order payable to |

|

|

|

“HAWAII STATE TAX COLLECTOR” in U.S. dollars drawn on any U.S. bank to Form |

AMOUNT OF PAYMENT |

|

|

Write the filing period and your Hawaii Tax I.D. No. on your check or money order. |

|

|

|

IF NO PAYMENT ATTACHED, ENTER “0.00.” You may also |

8 |

|

I declare under the penalties set forth in section

— MAILING ADDRESS —

HAWAII DEPARTMENT OF TAXATION

P.O. BOX 3827

HONOLULU, HI

ID NO 01 |

Form |

HW14_I 2019A 01 VID01

Document Characteristics

| Fact | Detail |

|---|---|

| Form Name | Form HW-14 |

| Revision Year | 2019 |

| Issuing Authority | State of Hawaii Department of Taxation |

| Type of Form | Withholding Tax Return |

| Amendment Option | Provides option for amended return |

| Filing Frequency | Quarterly |

| Due Date | On or before the 15th day of the month following the close of the calendar quarter |

| Final Return Option | Option to indicate final return and cancel withholding account |

| Payment Method | Check, Money Order, or E-payment |

Guidelines on Utilizing Hawaii Hw 14

Filing the Hawaii HW-14 form is a necessary step for entities to comply with state tax obligations. This document is utilized to report and remit income taxes withheld from employees to the State of Hawaii Department of Taxation. The procedure might seem complex at first glance, but by following a step-by-step approach, one can complete the form accurately. Whether you are submitting a standard return, amending a previous submission, or marking the end of your withholding account, attention to detail and accuracy are paramount. Proceed methodically to ensure all information is correct and submitted timely.

- Determine if you are filing an amended return and check the corresponding oval if applicable.

- Identify the quarter for which you are filing by marking the appropriate "Quarter Ending" box with Mar, Jun, Sep, or Dec.

- Enter your Hawaii Tax I.D. No. in the designated space along with the last four digits of your FEIN.

- Provide the name of the entity or individual for whom the tax is being reported in the "NAME" field.

- If this will be your final return and you're ending your withholding account, fill in the oval indicating so.

- On line 1, specify the total wages paid for the quarter, including COLA, third-party sick leave, and other benefits. Insert "0" if no wages were paid or if no tax was withheld.

- On line 2, report the total Hawaii income tax withheld during the quarter.

- Enter the total payments made for the quarter on line 3.

- If line 2 is greater than line 3, proceed directly to line 5. Otherwise, calculate the amount of credit to be refunded by subtracting line 3 from line 2, and enter the result on line 4.

- Line 5 is for additional taxes due for this quarter (line 2 minus line 3).

- For late filings only, calculate the penalty and interest, and enter these amounts on lines 6a and 6b, respectively.

- Add up lines 5, 6a, and 6b to find the total amount now due and payable, and record this sum on line 7.

- On line 8, enter the amount of payment. If you're attaching a check or money order, make it payable to “HAWAII STATE TAX COLLECTOR” and indicate the filing period and your Hawaii Tax I.D. No. on it. If no payment is attached, enter "0.00".

- Remember, all EFT payments must be transmitted by the due date to avoid a 2% EFT penalty.

After completing the form, review it thoroughly for accuracy. Missing or incorrect information can result in processing delays or penalties. Signed and dated, mail your form to the "HAWAII DEPARTMENT OF TAXATION" at the address provided on the form. Timely submission is crucial; ensure your HW-14 form is postmarked by the 15th day of the month following the quarter's close. By diligently following these steps, you'll accurately fulfill your tax obligations and contribute to a smooth process.

Understanding Hawaii Hw 14

- What is Form HW-14 used for? Form HW-14, issued by the State of Hawaii Department of Taxation, serves as a Withholding Tax Return. It is primarily used by employers to report and remit income taxes withheld from employees' wages each quarter. This form is essential for compliance with Hawaii's income tax withholding requirements.

- When is Form HW-14 due? This form must be filed by the 15th day of the month following the close of each calendar quarter. The quarters end in March, June, September, and December, making the due dates April 15th, July 15th, October 15th, and January 15th, respectively.

- How do I know if I need to file an amended Form HW-14? An amended Form HW-14 is necessary if you need to correct any information submitted on a previously filed return for the same period. If you discover errors in the wage amounts, taxes withheld, or other details after submitting your original return, you should file an amended return to correct these errors.

- Can I cancel my withholding account using Form HW-14? Yes, you can cancel your withholding account. To do so, simply fill in the oval indicating that it is your FINAL return on the form. This action notifies the Department of Taxation that you are canceling the withholding account as of that return.

- What should I do if no wages were paid or no tax was withheld during the quarter? If no wages were paid or no Hawaii income tax was withheld during the quarter, enter "0" in both the Total Wages Paid and Total Hawaii Income Tax Withheld sections of the form.

- How are payments made to the Hawaii Department of Taxation? Payments can be made by attaching a check or money order payable to “HAWAII STATE TAX COLLECTOR” in U.S. dollars drawn on any U.S. bank to your Form HW-14. Remember to include the filing period and your Hawaii Tax I.D. No. on your check or money order. Alternatively, you can e-pay at the official Hawaii tax website.

- What are the penalties for filing Form HW-14 late? If you file Form HW-14 after the due date, you may be subject to a penalty for late filing. The penalty is calculated as a percentage of the additional taxes due, and interest may also be charged on the amount owed until it is paid in full.

- How do I calculate additional taxes due or a refund? To determine if additional taxes are due for the quarter, subtract the Total Payments Made (line 3) from the Total Hawaii Income Tax Withheld (line 2). If the amount withheld is greater than the payments made, you may be eligible for a refund. In this scenario, skip to the Amount of Credit to be Refunded section. If the payments made exceed the tax withheld, then no additional taxes are due, and no refund can be claimed.

- Where should I mail Form HW-14? The completed form, along with any payment due, should be mailed to the Hawaii Department of Taxation at P.O. Box 3827, Honolulu, HI 96812-3827.

- Can I make payments electronically? Yes, payments can also be made electronically through the Hawaii Department of Taxation’s online payment system. It's important to note that all Electronic Funds Transfer (EFT) payments must be transmitted by the payment due date to avoid a 2% EFT penalty.

Common mistakes

Correctly filling out tax forms is crucial to ensure compliance with tax laws and to avoid unnecessary penalties. The Form HW-14, a Withholding Tax Return used by employers in Hawaii, is no exception. There are several common mistakes people make when completing this form that can lead to errors in tax reporting. Here is an analysis of these mistakes:

-

Incorrectly entering the Hawaii Tax I.D. No. and FEIN: The Hawaii Tax I.D. No. and the Federal Employer Identification Number (FEIN) are essential for identifying the business. Mixing up these numbers or entering them incorrectly can result in the tax return being processed for the wrong entity.

-

Failing to accurately report Total Wages Paid, including COLA, 3rd party sick leave, and other benefits in the designated section: Often, employers might overlook or miscalculate the inclusion of compensations such as Cost of Living Adjustments (COLA), third-party sick leave, and other taxable benefits, resulting in an incorrect tax base.

-

Not correctly calculating the Total Hawaii Income Tax Withheld: Incorrect calculations here can stem from an inaccurate understanding of tax rates or not including all necessary employee withholdings. This mistake directly affects the tax due to the state.

-

Misinterpretation of how to fill out the section for Total Payments Made for the quarter and resulting confusion over Additional Taxes Due or Credit to be Refunded: Some employers might confuse the total payments made for the quarter with the funds actually withheld for taxes, leading to discrepancies in additional taxes due or refunds claimed.

-

Omitting or inaccurately filling the Additional Taxes Due, Penalty, and Interest sections for late filings: Penalties and interest for late filing are often overlooked or miscalculated by filers. Neglecting these sections not only affects the accuracy of the tax return but can also lead to further penalties.

To mitigate these errors, it is recommended that filers:

- Double-check the Hawaii Tax I.D. No. and FEIB for accuracy.

- Thoroughly review all compensations paid to employees to ensure all taxable wages are reported.

- Use the official tax rate guidelines to correctly calculate the Hawaii Income Tax Withheld.

- Clearly understand the distinction between total payments made and taxes withheld to accurately fill out the relevant sections.

- Pay close attention to the deadlines and correctly calculate any additional taxes, penalties, and interest due for late filings.

By avoiding these common mistakes and following the recommendations provided, employers can ensure that their Form HW-14 submissions are accurate and compliant with Hawaii's tax laws.

Documents used along the form

When dealing with the Hawaii HW-14 form, a Withholding Tax Return used by businesses to report and pay the state income tax withheld from employees' wages, it's not just about completing and submitting this form alone. This process often involves several other forms and documents that ensure compliance with Hawaii's tax laws and facilitate accurate reporting. Here's a brief look at some of these additional forms and documents that are frequently used alongside the HW-14 form.

- Form W-2, Wage and Tax Statement: This form is crucial for employers as it reports an employee's annual wages and the amount of taxes withheld from their paycheck. It's essential not only for filing federal taxes but also for state tax purposes, including Hawaii.

- Form HW-3, Employer's Annual Return & Reconciliation of Hawaii Income Tax Withheld from Wages: This annual reconciliation form is used by employers to summarize employee withholdings for the year. It complements the quarterly HW-14 by providing an annual overview.

- Form HW-6, Employer's Quarterly Return of Income Tax Withheld: Prior to the consolidation of some tax forms by the Department of Taxation, this form was used by employers to report the income tax withheld each quarter. It has similar reporting requirements to the HW-14 form.

- Form UC-B6, Quarterly Wage, Contribution and Employment and Training Assessment Report: Filed with the Hawaii Unemployment Insurance Division, this form reports wages for each employee and calculates unemployment insurance contributions. While it focuses on unemployment insurance, the data aligns with payroll information used for the HW-14.

- Form 1099-MISC, Miscellaneous Income: For independent contractors or freelancers who aren't traditional employees, this form reports payments made to them. Employers need to manage these forms in conjunction with the HW-14 form if they withhold state income tax for these contractors.

Each of these documents plays a role in the larger framework of payroll and tax reporting requirements for businesses operating in Hawaii. Keeping accurate records and ensuring timely submissions can help businesses avoid penalties and maintain compliance with state regulations. Whether dealing with traditional employees or contractors, understanding these forms and how they interact with the HW-14 form is crucial for any employer.

Similar forms

The Hawaii HW-14 form is similar to other tax documents that businesses must file with various governmental agencies. These documents essentially serve the purpose of reporting and calculating taxes due, based on different types of transactions or income. Understanding the similarities between the HW-14 and other forms can help taxpayers ensure compliance and improve their overall tax filing process.

The Federal Form 941, or the Employer's Quarterly Federal Tax Return, shares several similarities with the HW-14 form. Like Form HW-14, which requires details on total wages paid, total Hawaii income tax withheld, and payments made for the quarter, Form 941 requires employers to report wages paid, federal income tax withheld, and both employee and employer shares of Social Security and Medicare taxes. Both forms are filed quarterly and serve to reconcile taxes withheld from employees' paychecks with the actual amounts owed to the tax authorities. Furthermore, these forms allow for reporting adjustments to taxes previously withheld, indicating any over- or under-payments.

Form W-3, the Transmittal of Wage and Tax Statements, is another document with functions similar to those of the Hawaii HW-14. While Form W-3 is primarily used for summarizing the information reported on all an employer's W-2 forms at the end of the year, it also involves reporting the total amount of taxes withheld from employees’ wages, akin to part of what is done with Form HW-14. The key similarity lies in their role in consolidating tax withholding information for submission to tax authorities. However, Form W-3 is filed annually and with the Social Security Administration, along with copies of the W-2s for all employees, thus serving a different cycle in the tax reporting process.

Each of these forms, including the HW-14, plays a pivotal role in the fiscal responsibility of businesses, ensuring that withheld taxes are accurately reported and appropriately remitted to either federal or state tax authorities. By understanding how these documents correlate, taxpayers can navigate their obligations more confidently, thereby maintaining compliance with both federal and state tax laws.

Dos and Don'ts

When filling out the Hawaii HW-14 form, understanding the right and wrong approaches can make a significant difference. Here are 5 things you should and shouldn't do:

Do's:

- Ensure all information is accurate and complete, including the Hawaii Tax I.D. No., name, and all amounts reported.

- Report total wages paid, including COLA, 3rd party sick leave, and other benefits accurately in the designated section.

- Calculate and enter the total Hawaii income tax withheld with precision to avoid discrepancies.

- If attaching a check or money order, confirm it is payable to “HAWAII STATE TAX COLLECTOR” and drawn on a U.S. bank. Also, ensure the filing period and your Hawaii Tax I.D. No. are written on it.

- File the return on or before the 15th day of the month following the close of the calendar quarter to avoid penalties and interest for late filing.

Don'ts:

- Leave any fields blank if they are applicable. Enter “0” or “0.00” where no amount is to report or no payment is attached.

- Forget to fill in the oval if this is your final return and you are cancelling this withholding account.

- Omit the attachment of your check or money order when a payment is due. Ensure it’s appropriately attached to Form HW-14.

- Ignore the penalties for late filing, such as filling out the penalty (line 6a) and interest (line 6b) sections only if your filing is late.

- Delay the e-payment beyond the due date if you opt to pay electronically, as failing to do so will result in a 2% EFT penalty.

Misconceptions

Understanding the Hawaii HW-14 form, a critical document for the correct processing of withholding taxes in Hawaii, is essential for businesses and accountants. However, there are common misconceptions surrounding the form, leading to confusion and potential errors in tax filings. Below is a clarification of some of these misconceptions:

- It's only for businesses. While primarily used by businesses to report employee tax withholdings, it must also be filed by any entity that has withheld Hawaii state income tax, including non-profit organizations and government agencies.

- Filing is required only if taxes were withheld. Entities must file the HW-14 form even if no taxes were withheld during the quarter. A report showing no withholding should still be submitted to maintain accurate records and compliance.

- The form is optional for those making Electronic Funds Transfers (EFT). Even if you submit payments via EFT, the HW-14 must still be filed to report the total wages paid, tax withheld, and reconcile the payments made for the quarter.

- Amended returns are complicated. Filing an amended HW-14 form is straightforward. Simply mark the "AMENDED return" box at the top of the form to indicate that it corrects a previously submitted filing.

- The penalty and interest sections are only for late filings. While Sections 6a and 6b pertain to penalties and interest for late filings, it's crucial to understand that inaccuracies or under-reporting can also result in penalties and interest calculated from the due date of the original return.

- Final returns are only for businesses closing. Marking the form as a "FINAL return" is necessary not only for entities ceasing operations but also for those who no longer have employees or are no longer required to withhold Hawaii state income tax.

- Personal checks are not accepted. The form specifies that payment should be made with a check or money order payable to "HAWAII STATE TAX COLLECTOR," including personal checks, as long as they are drawn from a U.S. bank and in U.S. dollars.

- Every section requires a dollar amount entry. If there is no amount to report in a section, entering "0.00" is appropriate and necessary for the form to be processed correctly.

- All entities must pay via EFT. While EFT is encouraged for its convenience and security, the reminder about the 2% EFT penalty applies specifically to those entities mandated by the state to make electronic payments, which may not include all filers.

Correctly understanding and applying the guidelines for the HW-14 form ensures compliance with Hawaii's tax regulations, avoiding unnecessary penalties, and ensuring accurate financial reporting.

Key takeaways

When handling the Hawaii HW-14 form, which pertains to withholding tax returns, individuals and businesses need to be aware of several crucial points to ensure compliance and accuracy in their submission. This document plays an essential role in tax administration, aiding both the taxpayer and the state in maintaining up-to-date and accurate financial records.

Timely Filing: The Hawaii HW-14 form must be submitted by the 15th day of the month following the close of each calendar quarter. These quarters end in March, June, September, and December. Timely filing is important to avoid penalties and interest charges due to late submissions. As such, marking your calendar or setting reminders could prevent oversight and ensure compliance with state deadlines.

Amendment and Final Returns: If circumstances require an amendment to a previously filed HW-14, or if this submission represents the final return marking the cessation of the withholding account, specific ovals on the form need to be filled to indicate these statuses. This distinction is crucial for the Department of Taxation to process and understand the context of the submission accurately.

Payment Information: Alongside the HW-14 form, any payments made towards the withholding tax must be attached in the form of a check or money order payable to the "HAWAII STATE TAX COLLECTOR." When submitting payments, it is critical to ensure they are made in U.S. dollars drawn on any U.S. bank, with the filing period and Hawaii Tax I.D. No. clearly noted on the payment document. This ensures that payments are correctly accounted for and attributed to the right entity and period.

Electronic Filing and Payment Options: The State of Hawaii encourages electronic filing and payments through its official tax portal. This not only streamlines the submission process but also facilitates quicker processing of returns and payments. However, it's worth noting that all electronic fund transfers (EFT) must be executed by the due date to avoid a 2% EFT penalty. Therefore, familiarizing oneself with the e-file system can be advantageous in adhering to deadlines and minimizing potential penalties.

Understanding and adhering to these key aspects can significantly affect the ease and correctness of submitting the HW-14 form. Moreover, staying informed about submission requirements and available resources can aid in reducing errors and ensuring that engagements with the Hawaii Department of Taxation are smooth and fruitful.

Create Common PDFs

Hawaii State Tax Forms - Form G-45 includes clear sections for listing gross proceeds, exemptions/deductions, and ultimately, the taxable income for accurate tax computation.

Food License Hawaii - Applicants must use an approved commercial kitchen for food preparation, and the permit number for this kitchen must be included.

Power of Attorney Vs Guardianship - Includes provisions for the termination of guardianship, outlining the process for reevaluation and release of guardianship duties as circumstances change.