Fill Your Hawaii M 38 Template

Understanding the intricacies of tax exemption for fuel used off public highways in Hawaii is essential for individuals and entities alike, which is where the Hawaii M-38 form comes into play. This form, a crucial document issued by the State of Hawaii Department of Taxation, serves as an exemption certificate for diesel oil and liquefied petroleum gas used off public highways, complying with Chapter 243 of the Hawaii Revised Statutes (HRS). Required to be prepared in triplicate, the form necessitates detailed information about the purchaser, including the business name, address, and the type of fuel purchased. Its primary purpose is to affirm that the fuel acquired is for operating motor vehicles or engines in areas other than the public highways, entailing specific obligations and conditions to avoid misuse. Moreover, the form lays out a framework for refund claims, the imposition of taxes in the absence of the certificate, and the circumstances under which additional information or taxes might be required. Through these provisions, the M-38 form plays a pivotal role in the administration and regulation of fuel tax exemptions in Hawaii, making it a significant document for businesses and individuals operating vehicles off the public roads.

Document Example

FORM |

|

STATE OF HAWAII |

|

|

Year |

|

||

(REV. 2001) |

|

DEPARTMENT OF TAXATION |

|

20 |

|

|

|

|

|

EXEMPTION CERTIFICATE |

|

|

|

|

|||

|

FOR DIESEL OIL AND LIQUEFIED PETROLEUM GAS USED OFF PUBLIC HIGHWAYS |

|

||||||

|

|

(Chapter 243, HRS) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of individual, corporation, or partnership |

|

Hawaii GE/Use Id. No. (if any) |

|

|

|

|

|

|

|

|

|

PREPARE THIS CERTIFICATE |

|

|||

|

|

|

|

IN TRIPLICATE AS FOLLOWS: |

|

|||

|

Name under which business is operated |

|

|

|

||||

|

|

|

|

|

|

|

|

|

Please |

|

|

|

1. |

Original for Distributor |

|

||

|

|

|

2. Copy for Tax Office |

|

||||

Business address (Number and Street) |

|

|

|

|||||

or |

|

|

|

3. Copy for Taxpayer |

|

|||

Type |

|

|

|

For filing requirements, see the |

|

|||

City, Town |

|

Island |

|

|||||

|

|

|

|

instructions below for WHEN TO |

|

|||

|

|

|

|

FURNISH A CERTIFICATE. |

|

|||

|

Name of Distributor |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

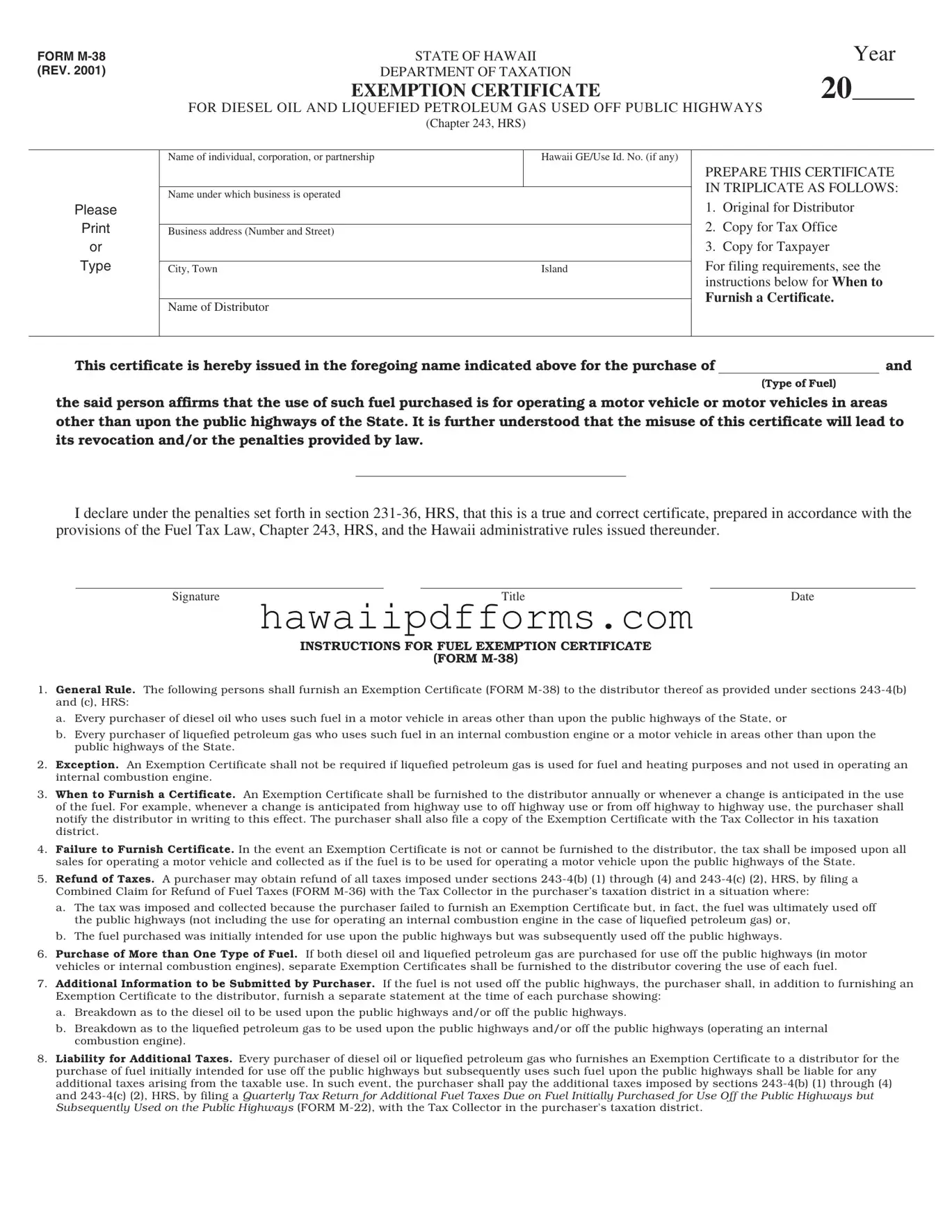

This certificate is hereby issued in the foregoing name indicated above for the purchase of |

|

|

and |

|

||||

|

|

|

|

|

(Type of Fuel) |

|

||

the said person affirms that the use of such fuel purchased is for operating a motor vehicle or motor vehicles in areas other than upon the public highways of the State. It is further understood that the misuse of this certificate will lead to its revocation and/or the penalties provided by law.

I declare under the penalties set forth in section

Signature |

Title |

Date |

INSTRUCTIONS FOR FUEL EXEMPTION CERTIFICATE

(FORM

1.General Rule. The following persons shall furnish an Exemption Certificate (FORM

a.Every purchaser of diesel oil who uses such fuel in a motor vehicle in areas other than upon the public highways of the State, or

b.Every purchaser of liquefied petroleum gas who uses such fuel in an internal combustion engine or a motor vehicle in areas other than upon the public highways of the State.

2.Exception. An Exemption Certificate shall not be required if liquefied petroleum gas is used for fuel and heating purposes and not used in operating an internal combustion engine.

3.When to Furnish a Certificate. An Exemption Certificate shall be furnished to the distributor annually or whenever a change is anticipated in the use of the fuel. For example, whenever a change is anticipated from highway use to off highway use or from off highway to highway use, the purchaser shall notify the distributor in writing to this effect. The purchaser shall also file a copy of the Exemption Certificate with the Tax Collector in his taxation district.

4.Failure to Furnish Certificate. In the event an Exemption Certificate is not or cannot be furnished to the distributor, the tax shall be imposed upon all sales for operating a motor vehicle and collected as if the fuel is to be used for operating a motor vehicle upon the public highways of the State.

5.Refund of Taxes. A purchaser may obtain refund of all taxes imposed under sections

a.The tax was imposed and collected because the purchaser failed to furnish an Exemption Certificate but, in fact, the fuel was ultimately used off the public highways (not including the use for operating an internal combustion engine in the case of liquefied petroleum gas) or,

b.The fuel purchased was initially intended for use upon the public highways but was subsequently used off the public highways.

6.Purchase of More than One Type of Fuel. If both diesel oil and liquefied petroleum gas are purchased for use off the public highways (in motor vehicles or internal combustion engines), separate Exemption Certificates shall be furnished to the distributor covering the use of each fuel.

7.Additional Information to be Submitted by Purchaser. If the fuel is not used off the public highways, the purchaser shall, in addition to furnishing an Exemption Certificate to the distributor, furnish a separate statement at the time of each purchase showing:

a.Breakdown as to the diesel oil to be used upon the public highways and/or off the public highways.

b.Breakdown as to the liquefied petroleum gas to be used upon the public highways and/or off the public highways (operating an internal combustion engine).

8.Liability for Additional Taxes. Every purchaser of diesel oil or liquefied petroleum gas who furnishes an Exemption Certificate to a distributor for the purchase of fuel initially intended for use off the public highways but subsequently uses such fuel upon the public highways shall be liable for any additional taxes arising from the taxable use. In such event, the purchaser shall pay the additional taxes imposed by sections

Document Characteristics

| Fact Name | Description |

|---|---|

| Purpose of Form M-38 | Exemption Certificate for Diesel Oil and Liquefied Petroleum Gas Used Off Public Highways. |

| Governing Law | Chapter 243, Hawaii Revised Statutes (HRS). |

| Form Submission Requirement | The form must be prepared in triplicate: one for the distributor, one for the Tax Office, and one for the taxpayer. |

| When to Furnish a Certificate | Annually or whenever there's a change in fuel use from off-highway to on-highway purposes or vice versa. |

| Failure to Furnish Certificate | Taxes will be imposed on all sales for fuel intended for use in operating a motor vehicle on public highways if the certificate is not provided. |

| Refund of Taxes | Purchasers can obtain a refund of taxes if the fuel was ultimately used off public highways by filing a Combined Claim for Refund of Fuel Taxes (Form M-36). |

Guidelines on Utilizing Hawaii M 38

After completing the Hawaii M-38 form, it is a critical step for individuals, corporations, or partnerships who utilize diesel oil and liquefied petroleum gas off public highways and seek tax exemption on these fuels in Hawaii. The form's provision is rooted in Chapter 243 of the Hawaii Revised Statutes (HRS), aiming to ensure proper tax practices. It's beneficial for those engaged in such operations to understand the process clearly, as failure to comply can result in the full imposition of taxes or penalties. Here are the essential steps to fill out the Hawaii M-38 form accurately:

- Gather the necessary information, including the name of the individual, corporation, or partnership, the Hawaii GE/Use ID No. (if you have one), and the name under which the business operates.

- Enter the business address, including the number and street, city, town, and island, in the designated fields.

- Specify the name of the distributor from whom the diesel oil or liquefied petroleum gas is being purchased.

- Indicate the type of fuel for which the exemption is sought by clearly writing either "diesel oil" or "liquefied petroleum gas" in the provided space.

- Confirm the intended use of purchased fuel is for operating motor vehicles or engines off the public highways by signing the declaration section of the form.

- The signatory must provide their signature, title, and the date to certify data accuracy under penalty per section 231-36, HRS.

- Prepare the certificate in triplicate as instructed: one copy for the distributor, one for the Tax Office, and one for your records.

- If anticipating a change in the use of the fuel or an annual update is due, submit a new Exemption Certificate to the distributor to ensure continued compliance.

- In case the exemption certificate is for both diesel oil and liquefied petroleum gas, separate certificates must be prepared for each fuel type.

- Keep a copy of the completed form for your records and send the original to the distributor, along with a copy to the Tax Office in the taxation district where the purchaser is located.

Following these steps ensures the smooth processing of the Hawaii M-38 form, enabling eligible parties to claim an exemption correctly. Remember, maintaining accurate records and promptly updating your exemption status as required can prevent unnecessary tax liabilities and ensure compliance with Hawaii's fuel tax laws.

Understanding Hawaii M 38

-

What is the purpose of Form M-38 in Hawaii?

The Form M-38 serves as an Exemption Certificate for Diesel Oil and Liquefied Petroleum Gas Used Off Public Highways in Hawaii. It's designed for individuals, partnerships, or corporations that purchase diesel oil or liquefied petroleum gas to operate motor vehicles or engines off public highways, allowing them to be exempt from certain taxes.

-

Who needs to submit Form M-38?

Form M-38 must be submitted by any purchaser of diesel oil or liquefied petroleum gas who intends to use the fuel in a motor vehicle or internal combustion engine in areas other than public highways. This includes both individuals and businesses that qualify under this exemption criteria.

-

Is there an exception to who must submit this certificate?

Yes, there is an exception. If the liquefied petroleum gas is used solely for fuel and heating purposes, not in operating an internal combustion engine, then an Exemption Certificate is not required.

-

When should the Form M-38 be furnished?

The Exemption Certificate should be provided to the distributor annually or whenever there is an anticipated change in the use of the fuel, such as switching from highway to off-highway use or vice versa. Additionally, a copy must be filed with the Tax Collector in the purchaser's taxation district.

-

What happens if the Form M-38 is not furnished?

If the certificate is not furnished to the distributor, taxes will be imposed and collected for all sales as if the fuel is to be used on public highways. This means the purchaser will not be eligible for the tax exemption.

-

Can a purchaser obtain a refund of taxes?

Yes, purchasers can obtain a refund of all taxes imposed if the fuel was ultimately used off public highways but was taxed due to the failure to furnish an Exemption Certificate, or if the fuel initially intended for highway use was subsequently used off highways. This requires filing a Combined Claim for Refund of Fuel Taxes (Form M-36) with the Tax Collector.

-

What if a purchaser buys more than one type of fuel?

If a purchaser buys both diesel oil and liquefied petroleum gas for use off public highways, separate Exemption Certificates must be furnished for each type of fuel detailing their respective non-highway uses.

-

What are the liabilities for additional taxes?

Purchasers who initially buy fuel for off-highway use but then use it on public highways must pay additional taxes. They are responsible for filing a Quarterly Tax Return for Additional Fuel Taxes Due on Fuel Initially Purchased for Use Off the Public Highways but Subsequently Used on the Public Highways (Form M-22) with the Tax Collector, covering the taxes due for the highway use.

Common mistakes

When completing the Hawaii M-38 form, which is the Exemption Certificate for Diesel Oil and Liquefied Petroleum Gas Used Off Public Highways, individuals and entities often overlook crucial details. This oversight can lead to errors, impacting the success of their application. Here are four common mistakes to avoid:

- Not preparing the certificate in triplicate: The instructions state that the certificate must be prepared in three copies. The original should be for the distributor, a copy for the Tax Office, and another for the taxpayer. Neglecting to distribute these copies appropriately can lead to recordkeeping and verification issues.

- Failure to furnish the certificate annually or when changes occur: Many forget the requirement to furnish this certificate to the distributor annually or whenever a change in the use of the fuel is anticipated. This oversight can lead to complications, especially if the fuel's usage changes from off-highway to highway use or vice versa.

- Omitting additional information when the fuel is used on public highways: If the fuel, initially intended for off-highway use, ends up being used on public highways, the purchaser must provide a detailed breakdown of the use. This includes specifying the amounts for diesel oil or liquefied petroleum gas. Failure to provide this breakdown can result in incorrect taxation or penalties.

- Incorrectly handling the liability for additional taxes: If the fuel purchased for off-highway use is later used on the highways, the purchaser is liable for additional taxes. Not filing the Quarterly Tax Return for Additional Fuel Taxes Due (FORM M-22) to cover this taxable use is a common mistake. This error can lead to unforeseen liabilities and possible legal complications.

Ensuring accuracy and compliance when filling out the M-38 form is crucial for individuals and entities. It's not only about adhering to regulations but also about securing the appropriate tax exemptions and avoiding penalties. Always review the form and its requirements carefully, and when in doubt, consult with a professional to avoid these common pitfalls.

Documents used along the form

The Hawaii M-38 Form is a crucial document for individuals, corporations, or partnerships in Hawaii that purchase diesel oil and liquefied petroleum gas for use off public highways. It ensures that purchasers are exempt from certain taxes typically applied to fuel used on public roads. To effectively navigate the regulations and requirements surrounding fuel use and taxation, many other forms and documents may be utilized alongside the M-38 Form. Understanding these associated documents can provide a comprehensive guide to managing fuel usage and taxation for off-highway purposes.

- Form M-36 - Combined Claim for Refund of Fuel Taxes: This form allows purchasers to claim a refund for taxes paid on diesel or liquefied petroleum gas that was eventually used off public highways, under certain conditions outlined in the Hawaii Revised Statutes.

- Form M-22 - Quarterly Tax Return for Additional Fuel Taxes Due: If fuel originally intended for off-highway use is used on public highways, this form is required to report and pay additional taxes due.

- Statement of Fuel Use: A separate statement that purchasers provide at the time of purchase, detailing the intended use of diesel oil or liquefied petroleum gas on or off the public highways.

- Form G-45 - General Excise/Use Tax Return: While not exclusively for fuel, this form might be necessary if fuel purchases or usage affects a business's overall taxable income and expenses in Hawaii.

- Form BB-1 - State of Hawaii Basic Business Application: Businesses purchasing fuel for off-highway use may need this form to register with the state for tax purposes, including general excise tax.

- Form VP-1 - Vehicle Permit Application: If off-highway use includes operating vehicles in restricted or specially designated areas, this application might be necessary to obtain the required permits.

- Form DOT-4 - Report of Fuel Usage: For commercial entities using fuel off public highways, this report may be required to document usage and ensure compliance with state regulations.

- Form A-6 - Tax Clearance Application: In some cases, to validate that all applicable state taxes have been paid, including those related to fuel usage, this form may be required for various licensing and registration purposes.

In conclusion, effectively managing fuel purchases and usage off public highways in Hawaii involves understanding and completing numerous forms and documents beyond just the M-38 Form. Each document plays a unique role in ensuring compliance, securing exemptions or refunds, and adhering to regulatory obligations. Individuals and businesses engaged in such activities must maintain thorough records and remain informed about the latest state requirements and procedures to navigate the complexities of fuel taxation and usage confidently.

Similar forms

The Hawaii M-38 form is similar to the Combined Claim for Refund of Fuel Taxes (Form M-36) in several ways. Both forms are integral to the administration of fuel tax laws under Chapter 243 of the Hawaii Revised Statutes. The M-38 form is used to certify that diesel oil and liquefied petroleum gas are being used off public highways, which qualifies the purchaser for an exemption from certain taxes. On the other hand, Form M-36 allows purchasers to claim a refund for taxes paid on fuel that was ultimately used off public highways or for uses other than originally intended. While the M-38 form is employed at the beginning of the fuel purchasing process to certify intended use, the M-36 form comes into play after the fact, enabling purchasers to rectify situations where they were unable to present an exemption certificate at the time of purchase or when the fuel's use changes.

Another document similar to the Hawaii M-38 form is the Quarterly Tax Return for Additional Fuel Taxes Due on Fuel Initially Purchased for Use Off the Public Highways but Subsequently Used on the Public Highways (Form M-22). While the M-38 form is used to declare an intent to use fuel in a tax-exempt manner, Form M-22 is employed when fuel, originally purchased for off-highway use and likely certified with an M-38, ends up being used on public highways. This change in usage results in a liability for additional taxes. Therefore, Form M-22 serves as the mechanism through which purchasers report and pay these taxes. Both forms are pivotal in ensuring the appropriate use of fuel in accordance with state tax laws, but they serve different points in the lifecycle of fuel usage and taxation; the M-38 form anticipates a tax exemption, whereas the M-22 accounts for situations where tax exemptions are negated by changes in fuel use.

Dos and Don'ts

When completing the Hawaii M-38 form for an exemption certificate for diesel oil and liquefied petroleum gas used off public highways, it’s essential to pay attention to both what you should and shouldn’t do to ensure the process is smooth and compliant. Below are key guidelines to follow:

What you should do:

- Prepare the certificate in triplicate: Make sure you have one copy for the distributor, one for the tax office, and one for your records.

- Provide accurate information: Ensure all details about your business and the type of fuel used are correct to avoid any discrepancies or legal issues.

- Notify the distributor of any changes: If there’s a change in how the fuel will be used (from off highway to on highway use or vice versa), promptly inform the distributor in writing.

- File a copy with the Tax Collector: Besides furnishing the exemption certificate to the distributor, also file a copy within your taxation district to remain compliant.

- Apply for refunds when applicable: If you’re eligible for a refund of taxes imposed due to a change in the use of the fuel that wasn’t initially anticipated, don’t forget to file a Combined Claim for Refund of Fuel Taxes (FORM M-36).

What you shouldn’t do:

- Overlook the need to furnish separate certificates for each fuel type: If you purchase both diesel oil and liquefied petroleum gas for off highway use, remember each requires its own exemption certificate.

- Ignore additional taxes if fuel usage changes: If the fuel initially intended for off highway use is later used on public highways, be prepared to pay any additional taxes due by filing the appropriate quarterly tax return.

- Fail to provide required breakdowns of fuel use: If the fuel is used both on and off the public highways, a detailed breakdown must be furnished at the time of each purchase.

- Forget to prepare the certificate accurately and truthfully: Misrepresenting information on the exemption certificate can lead to revocation and penalties under the law.

- Delay notifying the distributor of usage changes: Procrastination can complicate tax implications and refunds, so communicate any alterations in fuel use as soon as possible.

Misconceptions

One common misconception is that the Hawaii M-38 form is only for individual use. In reality, this form is applicable to individuals, corporations, or partnerships that purchase diesel oil and liquefied petroleum gas for use off public highways. The form's inclusive design ensures a broad range of entities can benefit from the exemption certificate.

Many believe the exemption applies automatically to all diesel and liquefied petroleum gas purchases. However, the exemption is specifically for those instances where the fuel is used in motor vehicles or internal combustion engines operating in areas other than upon the public highways of the State. This means eligibility for exemption requires specific use conditions to be met.

A third misunderstanding is that the M-38 form once submitted covers all future fuel purchases without the need for renewal. In contrast, the certificate must be furnished to the distributor annually or whenever there is a change in the use of the fuel, underlining the need for regular updates to maintain exemption status.

Some think filing this form is optional and overlook its importance. Failure to furnish the exemption certificate results in the normal imposition of tax on all fuel sales, indicating the critical nature of adhering to the filing requirements outlined for the exemption to apply.

There's also a misconception that the exemption does not apply to liquefied petroleum gas used in internal combustion engines if not used on public highways. The form clarifies that the exemption also covers liquefied petroleum gas used in internal combustion engines or motor vehicles in areas other than upon public highways, subject to specific conditions laid out in the instructions.

Another misunderstanding is regarding tax refunds. Some individuals are not aware that they may obtain a refund of all taxes imposed if the fuel was ultimately used off the public highways, or if initially intended for highway use, was subsequently used off the public highways. This offers a remedy for cases where taxes were paid under circumstances qualifying for exemption.

There is confusion over the purchase of multiple fuel types. Purchasers of both diesel oil and liquefied petroleum gas for off-highway use must furnish separate exemption certificates for each fuel type, ensuring that the exemption is properly documented for each category of fuel used.

Lastly, there's a misconception that there is no liability for misuse of the fuel once an exemption certificate is granted. Should the fuel initially intended for off-highway use be used on public highways, the purchaser is liable for additional taxes. This emphasizes the importance of accurate reporting and adherence to the intended use as stated in the exemption certificate.

Key takeaways

Filling out and properly using the Hawaii M-38 form is essential for individuals and businesses seeking exemption from fuel tax for diesel oil and liquefied petroleum gas used off public highways. Below are several key takeaways to ensure compliance and avoid potential pitfalls:

- Individuals or entities purchasing diesel oil or liquefied petroleum gas for use in motor vehicles off public highways must furnish an Exemption Certificate (Form M-38) to the distributor as stipulated under sections 243-4(b) and (c), HRS.

- The Form M-38 needs to be prepared in triplicate: the original for the distributor, a copy for the Tax Office, and a copy for the taxpayer's records.

- A notable exception exists where an Exemption Certificate is not required for liquefied petroleum gas used exclusively for fuel and heating purposes, not in operating an internal combustion engine.

- Certificates should be furnished annually or whenever a change in the use of the fuel is anticipated. Purchasers must notify the distributor in writing about such changes.

- In situations where an Exemption Certificate is not furnished, taxes will be imposed and collected as if the fuel were intended for use in operating a motor vehicle on public highways.

- Purchasers may qualify for a tax refund under specific conditions, particularly if the tax was imposed due to a failure to furnish an Exemption Certificate, yet the fuel was ultimately used off public highways.

- Separate Exemption Certificates are required if both diesel oil and liquefied petroleum gas are being purchased for off-highway use.

- Purchasers must provide a breakdown of how the diesel oil and liquefied petroleum gas will be used (on or off public highways) at the time of purchase if the fuel is not exclusively used off public highways.

- Additional taxes are levied on purchasers who initially use the fuel off public highways but later use it on public highways. Such individuals are liable for the additional taxes and must file a Quarterly Tax Return for Additional Fuel Taxes Due (Form M-22).

- Compliance with the specifics of the form and timely submission are crucial to leverage the benefits of fuel tax exemptions and avoid legal and financial repercussions.

Understanding and adhering to these guidelines can profoundly impact the proper handling of the Hawaii M-38 form, ensuring that the exemptions are applied correctly and efficiently, benefiting those eligible while maintaining adherence to state tax laws.

Create Common PDFs

G-17 Form - The Hawaii G-17 form serves as a resale certificate, essential for businesses engaged in goods resale, ensuring compliance with Hawaii’s General Excise Tax Law.

1128 Form - A key feature of the form is the patient acknowledgement section, where patients, guardians, or representatives confirm the accuracy of the information provided.

Hawaii T1 - This form indicates the nonrefundable nature of the $50 filing fee for trade name registration in Hawaii.