Fill Your Hawaii N 289 Template

The State of Hawaii Department of Taxation provides essential guidelines on the certification for exemption from withholding of tax on the disposition of Hawaii real property through Form N-289. This pivotal document, updated in 2008, outlines the requirements for transferors or sellers to certify their exemption from tax withholding upon the sale or transfer of real property in Hawaii. Specifically crafted to facilitate a smoother transaction between transferor/seller and transferee/buyer, the form underscores a vital compliance step for non-resident sellers involved in real estate transactions within the state. Highlighting the conditional exemptions, the form clearly delineates qualifications for exemptions such as residency status, application of nonrecognition provisions of the Internal Revenue Code or treaties, and the use of the property as a principal residence with a sale price not exceeding $300,000. In addition to depicting the necessary steps for certification, including the detailed documentation and the exacting qualifications under Hawaii Revised Statutes (HRS), the instructions articulate the obligations of the transferor/seller not to file this form with the Department of Taxation but rather to provide it to the transferee/buyer. This process is not only a testament to the standardized regulations in place for real estate transactions in Hawaii but also serves as a reminder of the importance of thorough documentation and adherence to statutory requirements to ensure the legality and integrity of property disposals, all the while maintaining a streamlined process for parties on both ends of the transaction.

Document Example

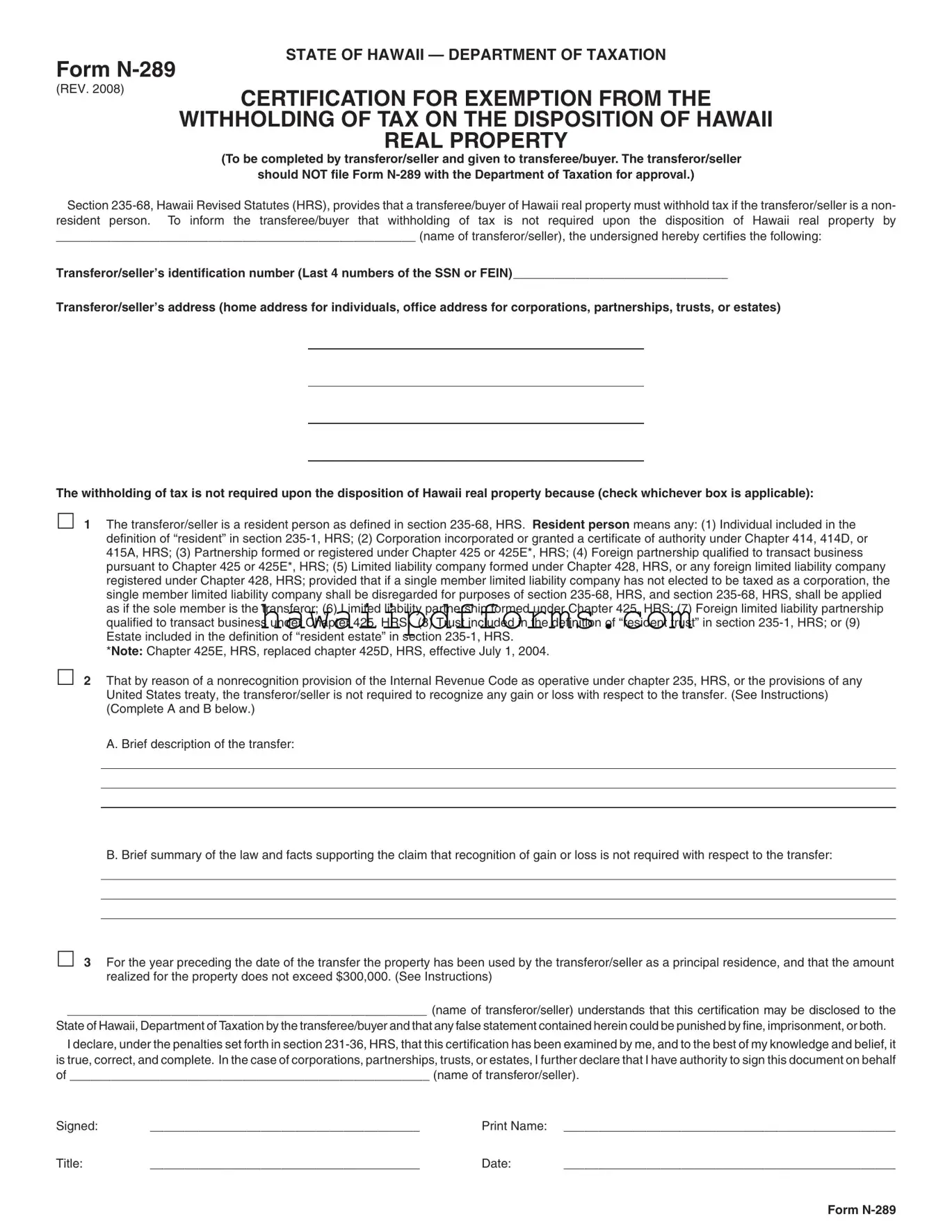

STATE OF HAWAII — DEPARTMENT OF TAXATION

Form

(REV. 2008)

CERTIFICATION FOR EXEMPTION FROM THE

WITHHOLDING OF TAX ON THE DISPOSITION OF HAWAII

REAL PROPERTY

(To be completed by transferor/seller and given to transferee/buyer. The transferor/seller should NOT file Form

Section

____________________________________________________ (name of transferor/seller), the undersigned hereby certifies the following:

Transferor/seller’s identification number (Last 4 numbers of the SSN or FEIN) _______________________________

Transferor/seller’s address (home address for individuals, office address for corporations, partnerships, trusts, or estates)

The withholding of tax is not required upon the disposition of Hawaii real property because (check whichever box is applicable):

1 The transferor/seller is a resident person as defined in section

*Note: Chapter 425E, HRS, replaced chapter 425D, HRS, effective July 1, 2004.

2 That by reason of a nonrecognition provision of the Internal Revenue Code as operative under chapter 235, HRS, or the provisions of any United States treaty, the transferor/seller is not required to recognize any gain or loss with respect to the transfer. (See Instructions) (Complete A and B below.)

A. Brief description of the transfer:

B. Brief summary of the law and facts supporting the claim that recognition of gain or loss is not required with respect to the transfer:

3 For the year preceding the date of the transfer the property has been used by the transferor/seller as a principal residence, and that the amount realized for the property does not exceed $300,000. (See Instructions)

____________________________________________________ (name of transferor/seller) understands that this certification may be disclosed to the

State of Hawaii, Department of Taxation by the transferee/buyer and that any false statement contained herein could be punished by fine, imprisonment, or both.

I declare, under the penalties set forth in section

Signed: |

_______________________________________ |

Print Name: |

________________________________________________ |

Title: |

_______________________________________ |

Date: |

________________________________________________ |

Form

INSTRUCTION |

STATE OF HAWAII — DEPARTMENT OF TAXATION |

FORM

(REV. 2008)

Instructions for Form

CERTIFICATION FOR EXEMPTION FROM THE WITHHOLDING OF TAX ON THE DISPOSITION OF HAWAII REAL PROPERTY

General Instructions

Purpose of Form

Use Form

Who Can Complete Form

The transferor/seller can complete Form

Where to Send Form

Form

Specific Instructions

At the top of Form

Check the applicable box to indicate the reason the withhold- ing of tax is not required upon the disposition of Hawaii real property.

Box number 1. Check box number 1 if the transferor/seller is a resident person as defined in section

Box number 2. Check box number 2 if by reason of a nonrecognition provision of the Internal Revenue Code as oper- ative under chapter 235, HRS, or the provisions of any United States treaty, the transferor/seller is not required to recognize any gain or loss with respect to the transfer. Complete sections A and B requesting a brief description of the transfer and a brief summary of the law and facts supporting the claim that recogni- tion of gain or loss is not required with respect to the transfer.

NOTE: If the withholding of tax is not required upon the dispo- sition of Hawaii real property because the disposition qualifies for the exclusion of gain from the sale of a principal residence under Internal Revenue Code section 121, check box number 2.

Box number 3. Check box number 3 if for the year preceding the date of the transfer the property has been used by the trans- feror/seller as a principal residence, and the amount realized for the property does not exceed $300,000. The "amount realized" means the sum of the cash paid, or to be paid (not including in- terest or original issue discount), the fair market value of other property transferred or to be transferred, and the amount of any liability assumed by the transferee/buyer or to which the Hawaii real property interest is subject to immediately before and after the transfer. Generally, the amount realized, for purposes of this withholding, is the sales or contract price.

NOTE: Although the withholding of tax may not be required upon the disposition of Hawaii real property, the trans- feror/seller is required under section

Signature

Form

Where to Get Information

Taxpayer Services Branch

P. O. Box 259

Honolulu, HI

Tel. No.:

Toll Free:

Document Characteristics

| Fact Number | Description |

|---|---|

| 1 | Form N-289 is titled as "Certification for Exemption from the Withholding of Tax on the Disposition of Hawaii Real Property". |

| 2 | The primary legislature governing this form is Section 235-68, Hawaii Revised Statutes (HRS). |

| 3 | Form N-289 is intended for use by the transferor/seller to certify that withholding of tax is not required when selling Hawaii real property. |

| 4 | The form must be completed and given to the transferee/buyer; it should not be filed with the Department of Taxation. |

| 5 | One of the exemptions for withholding tax includes the seller being a resident person as defined in Section 235-68, HRS. |

| 6 | Another exemption criterion is based on nonrecognition provisions of the Internal Revenue Code as applied under Chapter 235, HRS, or provisions of any United States treaty. |

| 7 | If the property was used by the transferor/seller as a principal residence in the year preceding the transfer, and the amount realized doesn't exceed $300,000, tax withholding is not required. |

| 8 | Submission of false information on Form N-289 could result in fines, imprisonment, or both. |

| 9 | Authorized signatures on Form N-289 include individual sellers, corporate officers, partners, trustees, or other fiduciaries. |

| 10 | For more information or assistance with Form N-289, contacts include the Taxpayer Services Branch with specific phone numbers and an address provided. |

Guidelines on Utilizing Hawaii N 289

Completing Form N-289 is a necessary step for transferor/sellers of Hawaii real estate to certify their exemption from withholding tax on the disposition of real property in Hawaii. This certification is crucial for informing the transferee/buyer that withholding of tax is not required under certain conditions defined by Hawaii state law. The form serves as a declaration of the seller’s residency status, applicability of nonrecognition provisions of tax law, or exemption due to the sale price of a principal residence. It’s important to carefully complete this form to ensure compliance with Hawaii tax laws and to prevent any potential legal issues that may arise from incorrect or incomplete information.

- Identification of the Transferor/Seller: At the top section of Form N-289, enter the full name, identification number (which is the last four digits of the Social Security Number, Individual Taxpayer Identification Number, or Federal Employer Identification Number), and address of the transferor/seller. Ensure the address corresponds with the type of seller (home address for individuals, office address for entities).

- Checking the Applicable Exemption Box: Identify the reason why tax withholding is not required on the sale of the property. Three options are provided:

- If the seller is a resident person as defined in section 235-68, Hawaii Revised Statutes (HRS), check the first box.

- If the transaction qualifies for a nonrecognition provision under the Internal Revenue Code or any U.S. treaty, check the second box and complete sections A and B detailing the transaction and supporting facts/law.

- If the property was used as the seller’s principal residence the preceding year and the sale price does not exceed $300,000, check the third box.

- Completing Sections A and B (if applicable): If the second box was checked, provide a brief description of the transfer (A) and a summary of the legal and factual basis for claiming nonrecognition of gain or loss on the transfer (B).

- Declaration: Read the declaration statement carefully. It warns about the potential consequences of providing false information, including fines and imprisonment.

- Sign and Date the Form: The form must be signed and dated by the transferor/seller. If the seller is an entity (corporation, partnership, trust, or estate), the individual signing must declare that they have the authority to do so on behalf of the entity. Include the printed name and title of the signer.

After completing Form N-289, it should be given to the transferee/buyer and not submitted to the Hawaii Department of Taxation. The transferee/buyer is responsible for retaining the form and attaching it to Forms N-288 and N-288A if not all sellers have provided a certification of exemption. This form is a critical component of real estate transactions in Hawaii, ensuring transparency and compliance with state tax regulations.

Understanding Hawaii N 289

What is the purpose of Hawaii Form N-289?

Form N-289 is designed to inform the transferee/buywall - buyer that tax withholding is not required upon the disposition of Hawaii real property under specific circumstances. These circumstances include when the transferor/seller is a resident of Hawaii, when the disposition is covered by a nonrecognition provision of the Internal Revenue Code as it applies under Hawaii law, or when the property was used by the seller as a principal residence and the amount realized does not exceed $300,000.

Who needs to complete Form N-289?

The transferor/seller of Hawaii real property is responsible for completing Form N-289. This form is pertinent when they are either a resident, are engaged in transactions not recognized for gain or loss under specific provisions, or when the property in question has served as their principal residence and the sale does not exceed the threshold amount.

Where should Form N-289 be sent?

Form N-289 should not be sent to the Department of Taxation. Instead, it must be completed by the transferor/seller and given to the transferee/buyer. The form serves as a certification of exemption from withholding tax, and it is the responsibility of the transferee/buyer to retain this form and not forward it to the Department of Taxation unless specified conditions require otherwise.

What information is required on Form N-289?

The form requires identifying information about the transferor/seller, including their name, identification number (the last four digits of their Social Security Number or Federal Employer Identification Number), and address. It also requires the transferor/seller to check the appropriate box indicating the reason tax withholding is not required and provide details supporting the claim, especially if the exclusion relates to the nonrecognition of gain or loss or the sale of a principal residence.

What happens if information on Form N-289 is found to be false?

The transferor/seller understands that providing false information on Form N-289 can lead to penalties, including fines and imprisonment. The form includes a declaration that, to the best of the transferor/seller's knowledge, the information provided is accurate, truthful, and complete. This declaration is made under the penalties set forth in section 231-36 of the Hawaii Revised Statutes.

Common mistakes

When filling out the Hawaii N-289 form, several common mistakes can lead to issues with the process. Here are five errors to avoid:

- Entering incorrect identification numbers: People often input either the wrong identification number or format, especially the last 4 digits of their Social Security Number (SSN) or Federal Employer Identification Number (FEIN).

- Omitting the transferor/seller’s address: The form requires a complete address, but it's often left incomplete. Remember, individuals should provide their home address, while corporations, partnerships, trusts, or estates should provide their office address.

- Failure to check the appropriate exemption box: It is essential to correctly identify the reason why withholding of tax is not required upon the disposition of Hawaii real property. This includes accurately determining whether the transferor/seller is a resident, the transfer qualifies under a nonrecognition provision, or if the property was used as a principal residence with the amount realized not exceeding $300,000.

- Providing insufficient details in Sections A and B when box number 2 is checked: If selecting the nonrecognition provision exemption, a brief description of the transfer and a summary of the law and facts that support the claim are required but often inadequately provided.

- Forgetting to sign the form or providing an unauthorized signature: The form must be signed by an individual with the authority to do so on behalf of the transfered seller. Neglecting to sign or signatures by persons without authority can invalidate the form.

In summary, when completing the Hawaii N-289 form, it's crucial to:

- Double-check the identification number entered for accuracy and correct format.

- Ensure the full and appropriate address is provided, based on the entity type of the transferor/seller.

- Correctly identify the applicable exemption reason and check the appropriate box.

- Provide detailed information in Sections A and B when necessary.

- Have the form signed by an individual authorized to do so.

Documents used along the form

When dealing with the disposition of Hawaii real property, especially under circumstances that do not require the withholding of tax, it is crucial to have all necessary documentation in order. The Hawaii N-289 form plays a fundamental role in these situations, helping certify that a seller is exempt from tax withholding under specific conditions. However, to ensure a smooth and compliant transaction, several other forms and documents may be required or highly recommended to supplement the N-289 form.

- Form N-288, Individual Withholding Tax Return: This form is necessary for reporting and paying the estimated tax withholding on the sale of Hawaii real property. It is used when the seller is a nonresident, and tax withholding is required.

- Form N-288A, Statement of Withholding on Dispositions by Nonresident Persons of Hawaii Real Property Interests: This document provides the details of the transaction, including the calculation of the withholding tax amount. It accompanies Form N-288 and is submitted to the Department of Taxation.

- Form N-289A, Certificate for Exemption from Withholding for Dispositions by Nonresident Persons of Hawaii Real Property Interests: Similar to Form N-289, this certificate is used under specific other conditions that warrant exemption from withholding tax. It provides an alternative basis for exemption not covered by Form N-289.

- Hawaii Real Property Tax Declaration: In the process of property transfer, this declaration form is filed with the county in which the property is located. It details the property's value, ownership transfer, and other pertinent information for real property taxation purposes.

- Closing Statement (HUD-1): Although not a tax form, the HUD-1 Settlement Statement is often required in real estate transactions. It itemizes all charges to the buyer and seller and provides a detailed account of the financial transaction, including the sales price, loan amounts, and tax levies.

These documents ensure compliance with Hawaii's tax laws and provide a clear record of the transfer and its financial aspects. When selling or transferring real estate in Hawaii, understanding the purpose of each form and accurately completing the required paperwork is essential for both the transferor and the transferee. Properly managing these documents can help facilitate a smoother property transaction, reduce potential legal hurdles, and ensure that all parties are well-informed about their tax responsibilities and exemptions.

Similar forms

The Hawaii N-289 form is similar to a few other tax-related documents in the United States, each designed for specific situations involving the transfer, sale, or disposition of assets. Understanding the similarities can help clarify when and why each form is used.

Federal Form 8288, U.S. Withholding Tax Return for Dispositions by Foreign Persons of U.S. Real Property Interests, shares certain similarities with the Hawaii N-289 form. Like the N-289, Form 8288 is used in real estate transactions and focuses on the withholding of tax. However, while the N-289 deals with Hawaii state tax exemptions for both resident and non-resident sellers, Form 8288 is used at the federal level to report and remit withholding taxes specific to foreign persons disposing of U.S. real property interests. Both forms are integral to ensuring compliance with tax obligations stemming from real estate transactions and require detailed information about the sale and the parties involved.

Form 1099-S, Proceeds From Real Estate Transactions, also bears resemblance to Hawaii's N-289 form in that it pertains to real estate transactions. Form 1099-S is used to report the sale or exchange of real estate. While the N-289 form is an exemption certification for withholding tax on the sale of Hawaii real property by demonstrating the seller's resident status or claiming other specific exemptions, Form 1099-S captures the overall proceeds from real estate transactions. Both documents are crucial for accurate tax reporting and help sellers and buyers fulfill their tax responsibilities related to real estate sales.

Form 6252, Installment Sale Income, while not identical, is another tax document related to the disposition of property, mirroring one aspect of the Hawaii N-289. This form is used when the seller receives payment for a property over a period that extends beyond the tax year. While Form 6252 focuses on the income aspect of installment sales, the N-289 emphasizes the withholding tax exemption applicable to certain qualifying Hawai'i real estate transactions. Both forms play important roles in reporting and potentially mitigating tax liabilities associated with property sales, although they focus on different elements of these transactions.

Dos and Don'ts

When filling out the Hawaii N-289 form, certain steps should be followed to ensure accuracy and compliance. Here's a list of things you should and shouldn't do:

- Do double-check the transferor/seller’s identification number. Use the last 4 digits of the SSN, FEIN, or ITIN to prevent any delays in processing.

- Do clearly specify the transferor/seller's correct address, whether it’s a home address for individuals or an office address for corporations and other entities.

- Do carefully select the applicable reason for exemption from withholding tax to ensure it accurately represents the transaction specifics.

- Do provide a brief but thorough description of the transfer and a summary of the law and facts if claiming exemption based on nonrecognition provisions.

- Don’t file the Form N-289 with the Department of Taxation. It should be completed and given to the transferee/buyer.

- Don’t leave the signature section blank. Ensure the document is signed by someone with the authority to do so on behalf of the transferor/seller.

Following these dos and don'ts will help in the smooth processing of your Hawaii N-289 form, making the transaction smoother for both the transferor and the transferee.

Misconceptions

Understanding the intricacies of Hawaii's Form N-289, which is crucial for real estate transactions, often invites a variety of misconceptions. Clarifying these misunderstandings can ensure that both transferors (sellers) and transferees (buyers) navigate their transactions with greater confidence and compliance. Here are ten common misconceptions and the truth behind each:

Form N-289 must be filed with the Department of Taxation. This form is actually not submitted to the Department of Taxation but instead is provided by the seller to the buyer to certify that withholding tax is not required on the sale.

Only non-residents are required to complete Form N-289. Any seller can complete Form N-289, resident or non-resident, provided they meet the qualifications for exemption from withholding tax on the disposition of their property.

The form is only for individuals. Not just individuals, but corporations, partnerships, trusts, or estates that are transferring property can also use Form N-289 to certify their exemption from withholding tax.

Filing this form means you don't have to pay any taxes on the sale. The purpose of the form is to certify exemption from withholding at the time of sale, not to exempt the seller from all tax obligations related to the property's sale.

Any type of property sale qualifies for Form N-289. Form N-289 is specific to real property, and its use is confined to certain criteria like residency status of the seller or use of the property as a principal residence.

If you use Form N-289, you don’t need an attorney or a real estate professional. While Form N-289 simplifies the tax process, legal or real estate advice might still be necessary, especially for complex transactions.

The form covers all parties in the transaction. Every seller involved in the property transfer must complete their own Form N-289 to certify their individual exemption from withholding tax.

You can only declare one reason for exemption on the form. Sellers should check all boxes that apply to their situation, providing a more comprehensive declaration of their reasons for claiming exemption.

The form is a one-time certification that doesn’t need updates. If circumstances change affecting eligibility for the exemption, such as a change in residency status, the relevant parties must be informed, and the transaction's details might need to be reevaluated.

Once completed, there's no need to keep a copy of Form N-289. It’s important for both the buyer and seller to keep copies of Form N-289 as part of their transaction records for future reference or in case of audit.

Critical as it is in the realm of Hawaii real estate transactions, accurate understanding and application of Form N-289 protect against potential legal and financial complications. It underscores the importance of diligence and clarity in handling real estate transactions, safeguarding the interests of all parties involved.

Key takeaways

Understanding the Hawaii N-289 form is essential for individuals engaged in real estate transactions, specifically when selling property in Hawaii. This form plays a crucial role in informing the buyer about the tax withholding requirements, or the lack thereof, on the disposition of real property by non-resident sellers. Here are ten key takeaways to assist in filling out and using the form effectively:

- The Hawaii N-289 form is designed to certify exemptions from withholding tax on the sale or disposition of Hawaii real property.

- This certification is necessary for transactions where the seller is a non-resident of Hawaii but claims an exemption from withholding tax under specified conditions.

- Completing the form: The seller or transferor is responsible for filling out the form, including their identification number, address, and the specific exemption reason.

- The form identifies three primary reasons for exemption: residency status, non-recognition of gain or loss under specific Internal Revenue Code provisions or U.S. treaties, and the sale of a principal residence for less than $300,000.

- Resident person: The term "resident person" encompasses a broad range of entities, including individuals, various types of corporations, partnerships, limited liability companies (LLCs), and trusts or estates deemed resident under Hawaii law.

- In instances where the sale involves the non-recognition of gain or loss, detailed descriptions of the transfer and supporting facts and laws must be provided in the form.

- For a property used as a principal residence where the sale amount does not exceed $300,000, the seller must certify this condition on the form.

- Submission and retention: The completed N-289 form should not be submitted to the Hawaii Department of Taxation by the seller. Instead, it must be given to the buyer or transferee.

- The buyer is required to retain the form and only submit it to the Department of Taxation if not all sellers have provided a certification, in which case it accompanies other specific taxation forms.

- The declaration at the end of the form must be signed by an authorized individual, asserting the truth and accuracy of the information provided and acknowledging the potential consequences of false statements.

It's also important to note that while this exemption deals specifically with withholding tax at the time of property transfer, sellers are still obligated under Hawaii statute to report the sale and potentially pay taxes on gains through their income tax returns. Helpful resources and more detailed information can be obtained by contacting the Hawaii Department of Taxation directly.

Create Common PDFs

Hawaii Llc Cost - Form X-8 is a straightforward approach for businesses to keep their state records current.

Cslb Meaning - Facilitates regulatory compliance by naming a dedicated employee to oversee construction standards and practices.

Incorporate in Hawaii - Specific to the State of Hawaii, the form outlines a clear pathway for companies deciding to legally dissolve, with the Department of Commerce and Consumer Affairs overseeing the process.