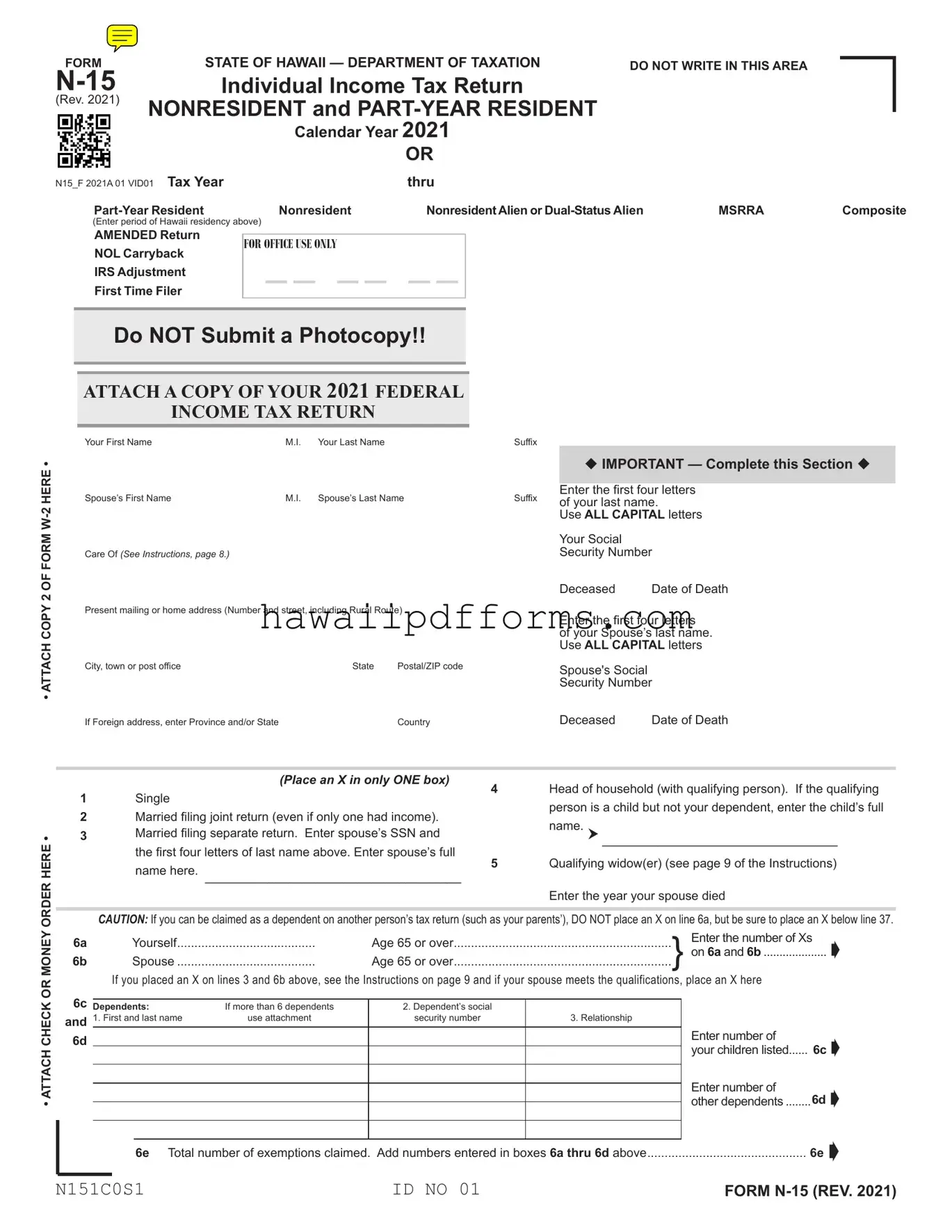

Fill Your Hawaii N15 Tax Template

The Hawaii N-15 Tax Form is an essential document for nonresidents and part-year residents who have earned income from the state of Hawaii during the tax year 2020. This form, crafted by the State of Hawaii Department of Taxation, has been meticulously designed to ensure that individuals who do not reside in Hawaii throughout the entire year, but who have generated income within the state, can accurately report and submit their state income tax returns. The N-15 form allows for detailed reporting of various types of income, such as wages, interest, dividends, and more, while also accommodating deductions, adjustments, and tax credits specific to Hawaii's tax system. Taxpayers can declare their residency status, which significantly impacts how their Hudson income is taxed. Special sections include allowances for military spouses under the Military Spouses Residency Relief Act (MSRRA), amended return options for those needing to correct previously submitted data, and sections for specifying payments made and refunds due. Furthermore, the form includes options for directing contributions to select funds, detailing dependents, and providing information on payment methods, which underscore its comprehensive nature in facilitating the tax filing process for its specified audience.

Document Example

FORM |

STATE OF HAWAII — DEPARTMENT OF TAXATION |

DO NOT WRITE IN THIS AREA |

|

|

||

Individual Income Tax Return |

|

|

|

|

||

(Rev. 2021) NONRESIDENT and |

|

|

|

|

||

|

|

|

|

|||

|

Calendar Year 2021 |

|

|

|

|

|

|

|

OR |

|

|

|

|

N15_F 2021A 01 VID01 Tax Year |

thru |

|

|

|

|

|

Nonresident |

Nonresident Alien or |

MSRRA |

Composite |

|||

(Enter period of Hawaii residency above) |

|

|

|

|

|

|

AMENDED Return

NOL Carryback

IRS Adjustment

First Time Filer

FOROFFICE USE ONLY

Do NOT Submit a Photocopy!!

• ATTACH COPY 2 OF FORM

ATTACH A COPY OF YOUR 2021 FEDERAL

INCOME TAX RETURN

Your First Name |

M.I. |

Your Last Name |

|

Suffix |

|

|

|

|

|

|

|

u IMPORTANT — Complete this Section u |

|

|

|

|

|

|

|

|

Spouse’s First Name |

M.I. |

Spouse’s Last Name |

Suffix |

Enter the first four letters |

||

of your last name. |

||||||

|

|

|

|

|

Use ALL CAPITAL letters |

|

|

|

|

|

|

Your Social |

|

Care Of (See Instructions, page 8.) |

|

|

|

|

Security Number |

|

|

|

|

|

|

Deceased |

Date of Death |

Present mailing or home address (Number and street, including Rural Route) |

|

Enter the first four letters |

||||

|

|

|

|

|

||

|

|

|

|

|

of your Spouse’s last name. |

|

|

|

|

|

|

Use ALL CAPITAL letters |

|

City, town or post office |

|

State |

Postal/ZIP code |

|

Spouse's Social |

|

|

|

|

|

|

Security Number |

|

If Foreign address, enter Province and/or State |

|

|

Country |

|

Deceased |

Date of Death |

ORDER HERE •

(Place an X in only ONE box)

1Single

2Married filing joint return (even if only one had income).

3Married filing separate return. Enter spouse’s SSN and the first four letters of last name above. Enter spouse’s full name here. _____________________________________

4Head of household (with qualifying person). If the qualifying person is a child but not your dependent, enter the child’s full

name. __________________________________

5Qualifying widow(er) (see page 9 of the Instructions) Enter the year your spouse died

• ATTACH CHECK OR MONEY

CAUTION: If you can be claimed as a dependent on another person’s tax return (such as your parents’), DO NOT place an X on line 6a, but be sure to place an X below line 37.

6a |

Yourself |

|

Age 65 or over |

Enter the number of Xs |

|

|||

|

||||||||

6b |

Spouse |

Age 65 or over |

|

|||||

|

If you placed an X on lines 3 and 6b above, see the Instructions on page 9 and if your spouse meets the qualifications, place an X here |

|

|

|||||

6c |

|

|

|

|

|

|

|

|

Dependents: |

If more than 6 dependents |

2. Dependent’s social |

|

|

|

|

||

and |

1. First and last name |

use attachment |

security number |

3. Relationship |

|

|

|

|

6d |

|

|

|

|

|

Enter number of |

|

6c  |

|

|

|

|

|

your children listed |

|

||

|

|

|

|

|

|

|

||

|

|

|

|

|

|

Enter number of |

6d  |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|||

|

|

|

|

|

|

other dependents |

||

|

|

|

|

|

|

|||

|

|

|

|

|

|

6e  |

||

|

|

|

|

|

|

|||

|

|

6e Total number of exemptions claimed. Add numbers entered in boxes 6a thru 6d above |

||||||

N151C0S1 |

ID NO 01 |

FORM

Form |

|

Page 2 of 4 |

|||

|

|

|

Your Social Security Number |

Your Spouse’s SSN |

|

N15_F 2021A 02 VID01 |

Name(s) as shown on return |

|

|

||

|

|

||||

|

|

|

|||

|

|

|

Col. A - Total Income |

Col. B - Hawaii Income |

|

7 |

Wages, salaries, tips, etc. (attach Form(s) |

7 |

|

||

8 |

Interest income from the worksheet on page 38 of |

|

|

||

|

the Instructions |

8 |

|

||

9 |

Ordinary dividends |

9 |

|

||

10 |

State income tax refund from the worksheet on |

|

|

||

|

page 38 of the Instructions |

10 |

|

||

11 |

Alimony received |

11 |

|

||

12 |

Business or farm income or (loss) |

12 |

|

||

13 |

Capital gain or (loss) from the worksheet on |

|

|

||

|

page 38 of the Instructions |

13 |

|

||

14 |

Supplemental gains or (losses) |

|

|

|

|

|

(attach Schedule |

14 |

|

||

15 |

IRA distributions |

15 |

|

||

16 |

Pensions and annuities (see Instructions and |

|

|

||

|

attach Schedule J, Form |

16 |

|

||

17 |

Rents, royalties, partnerships, estates, trusts, etc |

17 |

|

||

18 |

Unemployment compensation (insurance) |

18 |

|

||

19 |

Other income (state nature and source) |

|

|

||

|

________________________________ |

19 |

|

||

|

|

|

|||

20 |

Add lines 7 through 19 |

Total Income |

20 |

|

|

21 |

Certain business expenses of reservists, performing |

|

|

||

|

artists, and |

21 |

|

||

22 |

IRA deduction |

22 |

|

||

23 |

Student loan interest deduction from the worksheet |

|

|

||

|

on page 42 of the Instructions |

23 |

|

||

24 |

Health savings account deduction |

24 |

|

||

25 |

Moving expenses (attach Form |

25 |

|

||

26 |

Deductible part of |

26 |

|

||

27 |

27 |

|

|||

28 |

28 |

|

|||

29 |

Penalty on early withdrawal of savings |

29 |

|

||

30 |

Alimony paid (Enter name and SS No. of recipient) |

|

|

||

|

________________________________ |

30 |

|

||

|

|

|

|||

|

|

31 Payments to an individual housing account . |

31 |

|

|

|

|

32 First $7,152 of military reserve or Hawaii |

|

|

|

|

|

national guard duty pay |

32 |

|

|

|

|

|

|

|

|

N152C0S1 |

ID NO 01 |

FORM

Form |

Page 3 of 4 |

Your Social Security Number |

Your Spouse’s SSN |

Name(s) as shown on return

N15_F 2021A 03 VID01

33Exceptional trees deduction (attach affidavit)

|

(see page 21 of the Instructions) |

33 |

|

34 |

Add lines 21 through 33 |

......... Total Adjustments |

34 |

35 |

Line 20 minus line 34 .... |

Adjusted Gross Income |

35 |

36 |

Federal adjusted gross income (see page 22 of the Instructions) |

36 |

|

37 Ratio of Hawaii AGI to Total AGI. Divide line 35, Column B, by line 35, Column A (Compute to 3 decimal places and round to 2 decimal places) ... 37 CAUTION: If you can be claimed as a dependent on another person’s return, see the Instructions on page 22, and place an X here.

38If you do not itemize deductions, enter zero on line 39 and go to line 40a. Otherwise go to page 22 of the Instructions and enter your Hawaii itemized deductions here.

38a Medical and dental expenses |

|

(from Worksheet |

..............................38a |

38b |

Taxes (from Worksheet |

38b |

38c |

Interest expense (from Worksheet |

38c |

38d |

Contributions (from Worksheet |

38d |

38e |

Casualty and theft losses |

|

|

(from Worksheet |

38e |

38f |

Miscellaneous deductions |

|

|

(from Worksheet |

38f |

40a |

If you checked filing status box: 1 or 3 enter $2,200; |

|

|

2 or 5 enter $4,400; 4 enter $3,212 |

40a |

40b |

Multiply line 40a by the ratio on line 37 |

Prorated Standard Deduction 40b |

TOTAL ITEMIZED

DEDUCTIONS

39If your Hawaii adjusted gross income is above a certain amount, you may not be able to deduct all of your itemized deductions. See the

Instructions on page 27. Enter total here and go to line 41.

41 |

Line 35, Column B minus line 39 or 40b, whichever applies. (This line MUST be filled in) |

41 |

||

42a |

Multiply $1,144 by the total number of exemptions claimed on line 6e. If you and/or your spouse are blind, deaf, |

|

||

|

or disabled, place an X in the applicable box(es), and see the Instructions. |

|

||

|

Yourself |

Spouse |

42a |

|

42b |

Multiply line 42a by the ratio on line 37 |

Prorated Exemption(s) 42b |

||

43 |

Taxable Income. Line 41 minus line 42b (but not less than zero) |

Taxable Income 43 |

|||

44 |

Tax. Place an X if from: |

Tax Table; |

Tax Rate Schedule; or |

Capital Gains Tax |

|

|

( |

Place an X if tax from Forms |

|||

|

........................................................................................... |

Tax 44 |

|||

44a |

If tax is from the Capital Gains Tax Worksheet, enter |

|

|||

|

the net capital gain from line 8 of that worksheet |

44a |

|||

45 |

Refundable Food/Excise Tax Credit |

|

|

||

|

(attach Form |

.....45 |

|

||

46 |

Credit for |

|

|

||

|

Renters (attach Schedule X) |

46 |

|

||

47Credit for Child and Dependent Care

Expenses (attach Schedule X) |

47 |

|

|

||

48 Credit for Child Passenger Restraint |

|

|

|

||

System(s) (attach a copy of the invoice) |

48 |

|

|

||

49 |

Total refundable tax credits from |

|

|

|

|

|

|

Schedule CR (attach Schedule CR) |

49 |

|

|

50 |

Add lines 45 through 49 |

Total Refundable Credits |

50 |

||

|

51 |

Line 44 minus line 50. If line 51 is zero or less, see Instructions |

.............Adjusted Tax Liability |

51 |

|

N153C0S1 |

|

ID NO 01 |

|

||

Worksheet on page 41 of the Instructions.

FORM

Form |

Page 4 of 4 |

|

|

Your Social Security Number |

Your Spouse’s SSN |

|

Name(s) as shown on return |

|

N15_F 2021A 04 VID01 |

|

|

52 |

Total nonrefundable tax credits (attach Schedule CR) |

52 |

53 |

Line 51 minus line 52 |

Balance 53 |

54Hawaii State Income tax withheld (attach

(see page 30 of the Instructions for other attachments).....54

552021 estimated tax payments on

|

Forms |

TOTAL |

|

|

|

|

PAYMENTS |

56 |

Amount of estimated tax applied from 2020 return |

56 |

58 Add lines 54 through 57. |

|

|||

57 |

Amount paid with extension |

57 |

|

59If line 58 is larger than line 53, enter the amount OVERPAID

|

(line 58 minus line 53) (see Instructions) |

59 |

|

60 |

Contributions to (see page 30 of the Instructions): |

Yourself |

Spouse |

|

60a Hawaii Schools Repairs and Maintenance Fund |

$2 |

$2 |

|

60b Hawaii Public Libraries Fund |

$5 |

$5 |

|

60c Domestic and Sexual Violence / Child Abuse and Neglect Funds |

$5 |

$5 |

61 Add the amounts of the Xs on lines 60a through 60c and enter the total here |

61 |

||

62 |

Line 59 minus line 61 |

62 |

|

63Amount of line 62 to be applied to

|

your 2022 ESTIMATED TAX |

63 |

|

|

|

|

64a |

Amount to be REFUNDED TO YOU (line 62 minus line 63) If filing late, see page 31 of Instructions. |

Place an X here |

if this refund will |

|||

|

ultimately be deposited to a foreign |

|

|

|

||

64b |

Routing number |

64c Type: |

Checking |

Savings |

|

|

64d |

Account number |

|

........................... |

64a |

|

|

65 |

AMOUNT YOU OWE (line 53 minus line 58) |

|

65 |

|

|

|

66PAYMENT AMOUNT Submit payment online at hitax.hawaii.gov or attach check or

money order payable to “Hawaii State Tax Collector.” |

66 |

67Estimated tax penalty. (See page 31 of Instr.) Do not include this amount

|

in line 59 or 65. Check this box if Form |

67 |

|

68 |

AMENDED RETURN ONLY - Amount paid (overpaid) on original return. (See Instructions) (attach Sch. AMD) |

68 |

|

69 |

AMENDED RETURN ONLY - Balance due (refund) with amended return. (See Instructions) (attach Sch. AMD) |

69 |

|

DESIGNEE

If designating another person to discuss this return with the Hawaii Department of Taxation, complete the following. This is not a full power of attorney. See page 32 of the Instructions.

Designee’s name |

Phone no. |

Identification number |

HAWAII ELECTION |

|

Do you want $3 to go to the Hawaii Election Campaign Fund? |

Yes |

No |

CAMPAIGN FUND |

ÂIf joint return, does your spouse want $3 to go to the fund? |

Yes |

No |

|

(See page 32 of the Instructions) |

||||

Note: Placing an X in the “Yes” box will not increase your tax or reduce your refund.

PLEASE SIGN HERE

DECLARATION — I declare, under the penalties set forth in section

|

Your signature |

|

|

Date |

|

Spouse’s signature (if filing jointly, BOTH must sign) |

Date |

||||||

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Your Occupation |

|

|

Daytime Phone Number |

|

Your Spouse’s Occupation |

|

|

Daytime Phone Number |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

||

Paid |

Preparer’s |

|

|

|

|

Date |

Check if |

|

Preparer’s identification number |

|

|||

Preparer’s |

Signature |

|

|

|

|

|

|

|

|

|

|||

Information |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Federal E.I. No. |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|||||

|

|

Preparer’s Name |

|

|

|

|

|

|

|||||

|

|

Firm’s name (or yours |

|

|

|

Phone No |

|

|

|

|

|

||

|

|

if |

|

|

|

|

|

|

|

|

|||

|

|

Address, and ZIP Code |

|

|

|

|

|

|

|

|

|

||

N154C0S1 |

ID NO 01 |

FORM

Document Characteristics

| Fact | Detail |

|---|---|

| Form Type | N-15 Individual Income Tax Return |

| Revision Year | 2020 |

| Applicability | Nonresident and Part-Year Resident |

| Special Categories | Nonresident Alien or Dual-Status Alien, MSRRA, Composite |

| Options Available | AMENDED Return, NOL Carryback, IRS Adjustment, First Time Filer |

| Attachment Requirements | Copy of FORM W-2, 2020 Federal Income Tax Return |

| Filing Options | Single, Married (joint or separate), Head of household, Qualifying widow(er) |

| Governing Law | Hawaii Income Tax Law, Chapter 235, HRS |

Guidelines on Utilizing Hawaii N15 Tax

Filing taxes can sometimes feel like navigating through a maze, but understanding the steps to complete the Hawaii N-15 tax form can simplify the process. This guide is here to help you accurately complete your form, whether you're a nonresident or part-year resident of Hawaii for the tax year 2020. By breaking down the form into manageable steps, you can ensure that you're providing all the necessary information and taking advantage of any tax benefits available to you.

- Start by entering your full name, including your middle initial (M.I.), and if applicable, your suffix (e.g., Jr., Sr.) in the designated spaces on the form.

- Fill in your spouse’s first name, middle initial (M.I.), and suffix if you are filing a joint return.

- Provide your current mailing address, including the number and street, city, town or post office, state, and ZIP code. For foreign addresses, include the province and/or state, and country name.

- Enter the first four letters of your last name and your spouse’s last name (if applicable) in capital letters in the fields provided.

- Fill out your Social Security Number (SSN) and, if filing jointly, your spouse's SSN.

- Indicate your filing status by placing an "X" in the appropriate box. The options include single, married filing jointly, married filing separately, head of household, or qualifying widow(er).

- Enter details about your dependents, including their first and last names, social security numbers, and relationship to you. Calculate the total number of exemptions you are claiming and enter this amount.

- Report your income in the respective sections starting from line 7 through 19. Attach all required forms such as W-2s or schedules if you have income from wages, interest, dividends, business or farm operations, capital gains, etc.

- Calculate your total income and enter this amount on line 20.

- Deduct any specific expenses or adjustments to income on lines 21 through 33, such as IRA contributions, student loan interest, and moving expenses. Add these adjustments and enter the total on line 34.

- Subtract your total adjustments from your total income to find your adjusted gross income and enter this on line 35.

- If applicable, compute your Hawaii taxable income by following instructions for lines 36 through 43, including deductions and exemptions relevant to Hawaii income.

- Determine the tax owed by referring to the tax tables or schedules provided in the instructions, and enter this amount on line 44.

- Claim any applicable credits such as the Refundable Food/Excise Tax Credit, Credit for Low-Income Household Renters, etc., and enter the total refundable credits on line 50.

- Calculate your adjusted tax liability by subtracting your total refundable credits from your tax owed (line 51).

- Include information about Hawaii tax withheld, estimated tax payments, and any payments made with an extension. Add these amounts to calculate your total payments and enter this on line 58.

- If you are due a refund, or owe additional tax, calculate these amounts and complete sections 59 through 69 accordingly, including your bank information for direct deposit if desired.

- Sign and date the form. If you are filing jointly, make sure both you and your spouse sign. Also, complete the section for third-party designee if you want someone else to discuss this return with the Hawaii Department of Taxation.

Meticulously reviewing your completed form before submission is crucial to ensure accuracy and completeness. This step not only helps in avoiding common mistakes but also in speeding up the processing of your tax return. Remember, accurately filing your tax return is an important duty that contributes to your financial well-being.

Understanding Hawaii N15 Tax

Who needs to file the Hawaii N-15 Tax Form?

The Hawaii N-15 Tax Form is designed for nonresidents and part-year residents of Hawaii. This includes those who earned income from sources within Hawaii but were not residents for the entire tax year, as well as nonresident aliens and individuals with dual-status alien situations for the specified tax year.What income types are reported on the N-15 Form?

Income that must be reported includes wages, salaries, tips, interest income, dividends, state income tax refunds (subject to certain conditions), alimony received, business or farm income, capital gains, supplemental gains, IRA distributions, pensions, annuities, and other sources such as rents, royalties, unemployment compensation, and any miscellaneous income sourced from Hawaii.Can I claim deductions on the N-15 Form?

Yes, you can claim various deductions like IRA deductions, student loan interest deduction, health savings account deduction, moving expenses for work-related relocation, deductible part of self-employment tax, self-employed health insurance deduction, and more. It's important to accurately calculate these to understand your taxable income properly.How are itemized deductions handled for part-year residents or nonresidents?

Part-year residents and nonresidents can itemize their deductions or take the standard deduction, similar to residents. However, if you choose to itemize, you may only deduct expenses related to income that's taxable in Hawaii. Make sure to follow the specific instructions for itemizing deductions on this form, as they could be different from federal itemized deductions.What are the tax credits available on the Hawaii N-15 Form?

There are several refundable and nonrefundable tax credits available, such as the Refundable Food/Excise Tax Credit, Credit for Low-Income Household Renters, Credit for Child and Dependent Care Expenses, Credit for Child Passenger Restraint System(s), and various other credits for specific situations and qualifications.How does one calculate the tax owed or refund due on the N-15?

To calculate the tax owed or refund due, you'll subtract any tax credits from your adjusted tax liability. If you've made payments through withholding or estimated tax payments that exceed your tax liability, you'll likely receive a refund. Conversely, if your payments were less than what you owe, the remaining amount is what you'll need to pay.What should be attached to the N-15 Form upon submission?

When submitting the N-15 Form, make sure to attach a copy of your W-2 forms (if applicable), a copy of your federal income tax return, and any other required documents for specific deductions or credits you're claiming. This documentation is necessary to verify the income and deductions reported on your return.Where and how can the N-15 Form be submitted?

The N-15 Form can be submitted either by mail or electronically, through the state's official tax filing website. Electronic filing is often faster, and can lead to quicker processing of any refunds due. However, if you owe tax, you can also make payments online, which is convenient and ensures timely receipt by the Department of Taxation.

Common mistakes

When completing the Hawaii N-15 Tax Form, individuals often encounter various mistakes that could impact the accuracy and processing of their tax returns. Highlighted below are eight common errors:

- Not attaching required documents like copy 2 of Form W-2 or the federal income tax return.

- Incorrectly filling out personal information, such as social security numbers or the first four letters of last names in all capital letters.

- Choosing the wrong filing status or not correctly entering information about a spouse when filing a joint or separate return.

- Failure to accurately report income, such as wages or interest income, resulting in either underreporting or overreporting income.

- Miscalculating adjustments to income, which could include business expenses or IRA deductions, leading to an incorrect adjusted gross income.

- Not utilizing the correct worksheets for deductions and exemptions, particularly when itemizing deductions or calculating exemptions based on the ratio of Hawaii AGI to total AGI.

- Omitting to claim eligible credits such as the Refundable Food/Excise Tax Credit or Credit for Low-Income Household Renters, potentially missing out on beneficial tax breaks.

- Error in determining tax liability or refund due, which can result from incorrect tax calculations, overlooking the prorated standard deduction, or failing to apply nonrefundable and refundable tax credits properly.

Beyond these common errors, individuals should also ensure that all designee information is complete if they wish to designate another person to discuss the return. Additionally, deciding about contributions to the Hawaii Election Campaign Fund should be made clearly, as it does not affect the tax liability or refund. Completing the N-15 Tax Form accurately ensures timely processing and avoids potential fines or delays..

Documents used along the form

Filing the Hawaii N-15 Tax Form is an important process for nonresidents and part-year residents that requires careful attention and often multiple supporting documents. To ensure accurate reporting and compliance with Hawaii's Department of Taxation, individuals may need to include various forms and documents alongside their N-15 form. Below is a list of documents often used in conjunction with the Hawaii N-15 Tax Form, each described briefly to understand its purpose and significance.

- Form W-2: Shows the amount of wages earned and taxes withheld by an employer. It's necessary for reporting income on the N-15 form.

- Federal Income Tax Return: Used to provide information on your federal tax situation, which can affect your state tax filing.

- Schedule D-1: Required if you have supplemental gains or losses to report. This schedule helps detail these transactions.

- Schedule J (Form N-11/N-15/N-40): Used for reporting income from pensions, annuities, and IRA distributions. It helps calculate the taxable amount of these payments.

- Form N-139: Provides information on moving expenses if you have relocated, which can sometimes be deducted.

- Form N-311: Used to claim the refundable Food/Excise Tax Credit, which can provide a refund or reduce the amount owed.

- Schedule X: Needed for specific credits like the Low-Income Household Renters Credit or the Credit for Child and Dependent Care Expenses.

- Schedule CR: A comprehensive form for claiming various tax credits that may reduce the amount of tax owed.

- Form W-2s: Attachments required if you've had multiple employers or sources of income that need to be reported separately.

Correctly identifying and including these documents with your Hawaii N-15 Tax Form can significantly streamline the filing process. It ensures that all sources of income, deductions, and credits are accurately accounted for, potentially leading to a more favorable tax outcome. Always make sure to review the latest forms and instructions provided by the Hawaii Department of Taxation as requirements can change.

Similar forms

The Hawaii N-15 Tax Form is similar to the IRS Form 1040NR, which is used by nonresident aliens and dual-status aliens for filing federal income taxes in the United States. Both forms are designed to cater to individuals who have income coming from a specific state or the U.S. but are not residents for tax purposes. They include sections for reporting income, adjustments to income, and allowable deductions that are pertinent to nonresidents or part-year residents. This similarity ensures that nonresidents comply with tax obligations in a manner that reflects their unique status, allowing for income that was earned within the jurisdiction (Hawaii for Form N-15 and the U.S. for Form 1040NR) to be taxed appropriately. Each form provides instructions for calculating state or federal adjusted gross income, taking into account the different sources of income relevant to nonresidents, such as wages, dividends, and scholarships.

Analogously, the Hawaii N-15 Tax Form can be compared to the California Form 540NR. This form is used by nonresidents or part-year residents to file their California state income tax returns. Similar to the Hawaii N-15, California's Form 4040NR allows filers to report income that is attributable to the specific state, make necessary adjustments, and claim deductions or credits that are available to nonresidents or part-year residents. A key aspect of both forms is their ability to accommodate filers who have income sources within the state but do not meet the residency criteria for a full tax year, ensuring that individuals only pay taxes on the income earned within the respective state. Additionally, both forms include specific instructions for prorating deductions and credits based on the amount of income that is subject to state tax, helping individuals accurately fulfill their tax responsibilities.

Dos and Don'ts

When you are filling out the Hawaii N-15 Tax Form, there are specific steps you should follow and mistakes you should avoid to ensure accuracy and compliance with Hawaii tax law. Paying close attention to the details and instructions provided by the Department of Taxation is crucial. Here are some vital do's and don'ts:

- Do include your Social Security Number and, if applicable, your spouse's as well. It is essential for processing your tax return.

- Do accurately report all income, deductions, and credits to which you are entitled. Double-check the form's instructions for specific details on how to do this correctly.

- Do attach a copy of your federal income tax return and Form W-2, if required. These documents provide necessary information and verify your income statements.

- Do choose the correct filing status. Your filing status affects your tax rates, standard deduction amounts, and eligibility for certain tax credits.

- Do use the correct form for your residency status. The N-15 form is specifically for nonresident and part-year resident filers. Ensure this applies to you before proceeding.

- Do sign and date the form. An unsigned tax return is like an unsigned check – it's not valid.

- Do double-check your math and the information provided to reduce the chances of errors. Mistakes can delay processing and affect your tax liability or refund.

- Don't overlook the importance of the mailing address. Ensure it's accurate and clearly legible to avoid any miscommunication or loss of correspondence from the Department of Tax compteForm.

- Don't submit a photocopy of the form. The Department of Taxation requires an original form for processing.

- Don't guess on amounts or leave sections blank. If you're unsure, review the instructions again, use the department's resources, or consult with a tax professional.

- Don't forget to claim all dependents and exemptions you're entitled to but ensure they meet the eligibility criteria outlined in the instructions.

- Don't neglect to attach required schedules or documentation for specific income sources, deductions, or credits claimed on your return.

- Don't file late without necessary extensions. Late filing can result in penalties and interest charges on taxes owed.

- Don't send cash through the mail if you owe taxes. Use a check, money order, or make a payment online. Ensure it is correctly addressed and payable to the "Hawaii State Tax Collector."

Following these guidelines will help ensure that your Hawaii N-15 Tax Form is filled accurately and in compliance with tax laws, thereby minimizing the potential for errors and the likelihood of an audit. Should you have any doubt, referring to the comprehensive instructions provided with the form or seeking professional advice is wise.

Misconceptions

Understanding the intricacies of tax forms is crucial for ensuring compliance with tax laws, particularly for residents and nonresidents of Hawaii. The State of Hawaii's N-15 Tax Form is tailored for nonresidents and part-year residents who need to file income tax returns. However, there are several misconceptions surrounding this form that can lead to misunderstandings or even misfiling. By clarifying these misconceptions, taxpayers can better navigate their obligations and avoid common pitfalls.

Misconception 1: The N-15 Form is only for nonresidents. While designed primarily for nonresidents and part-year residents of Hawaii to report their income, it's also applicable for residents who have income sourced from other states or countries and for those who have moved into or out of Hawaii within the tax year.

Misconception 2: All income must be reported on the N-15 Form. Taxpayers should only report income that is sourced to Hawaii. For example, income from employment performed in Hawaii, or income from property located in the state. Personal services performed outside of Hawaii by a nonresident do not need to be included.

- Misconception 3: Filing status options are limited on the N-15 Form. The form allows for various filing statuses including single, married filing jointly, married filing separately, head of household, and qualifying widow(er), similar to federal tax forms.

- Misconception 4: Taxpayers can't claim dependents on the N-15. Dependents can indeed be claimed, provided they meet specific requirements, such as the dependent's relationship to the taxpayer, income thresholds, and residency status.

- Misconception 5: Part-year residents must file two separate N-15 Forms. Part-year residents use a single N-15 Form to report their total income for the year, with a section dedicated to differentiating between income earned while a resident and income earned while a nonresident.

- Misconception 6: Nonresidents are taxed at a higher rate on the N-15. Hawaii's income tax rates apply equally to residents and nonresidents; the difference is in the source and amount of income that is subject to taxation.

- Misconception 7: Taxpayers cannot deduct expenses on the N-15. Deductions are allowed on the N-15 form, including certain business expenses, moving expenses, and contributions to retirement plans, similar to deductions allowed on federal tax returns.

- Misconception 8: Extensions to file the N-15 are not allowed. Extensions can be granted, aligning with federal extension policies, though taxpayers are encouraged to pay estimated taxes by the original due date to avoid penalties and interest.

By demystifying these misconceptions, taxpayers can approach the filing of the Hawaii N-15 Tax Form with greater confidence and accuracy. It is important to thoroughly review the form and its instructions, or consult with a tax professional, to ensure compliance and optimize tax outcomes.

Key takeaways

Filling out the Hawaii N-15 tax form is a detailed process that requires attention to specific instructions and accurate information. This form is designed for nonresidents and part-year residents of Hawaii, including nonresident aliens, to file their state income tax returns. Here are key takeaways to guide you through the process:

- Know Your Residency Status: Before you start filling out the form, determine whether you are a nonresident, part-year resident, nonresident alien, or dual-status alien. This classification affects how you will be taxed and which income is taxable by the State of Hawaii.

- Attach Required Documents: Ensure you attach a copy of your federal tax return and Form W-2 to your N-15 form. These documents are crucial for verifying income and tax information.

- Choose the Correct Filing Status: Your filing status affects your tax rate and available deductions. Make sure to use the same filing status on your Hawaii return as you did on your federal return, unless your residency status in Hawaii differs from your federal status.

- Report All Sources of Income: Include all sources of income, whether from wages, dividends, interest, or any other source. For nonresidents, only income earned from Hawaii sources should be reported, while part-year residents must report all income received while a resident plus any income sourced to Hawaii during the nonresident portion of the year.

- Understand Deductions and Credits: Familiarize yourself with the deductions and credits you're eligible for. Some may differ from those on your federal return. For instance, there could be differences in itemized deductions and standard deduction amounts.

- Complete Deductions and Tax Credits Sections Carefully: Deductions reduce your taxable income, potentially lowering your tax bill. Credits may reduce your tax directly. For example, there are credits for low-income household renters, child and dependent care expenses, and renewable energy technologies.

- Direct Deposit for Refunds: If you're expecting a refund, providing your banking information for direct deposit can expedite the process. Ensure that the routing number and account number are entered correctly to avoid any delays.

Accuracy is key when filling out the N-15 form. Double-check your figures and information before submission to avoid errors that could lead to delays or audits. Remember, tax laws and regulations change, so it's important to use the most current form and instructions when filing your return.

Create Common PDFs

Restraining Order Hawaii - This form allows individuals in Hawaii to seek protection against physical threats or harm by another person.

N-15 - To ensure proper credit to their account, filers must include their Hawaii Tax I.D. No. on their check or money order.