Fill Your N 301 Hawaii Template

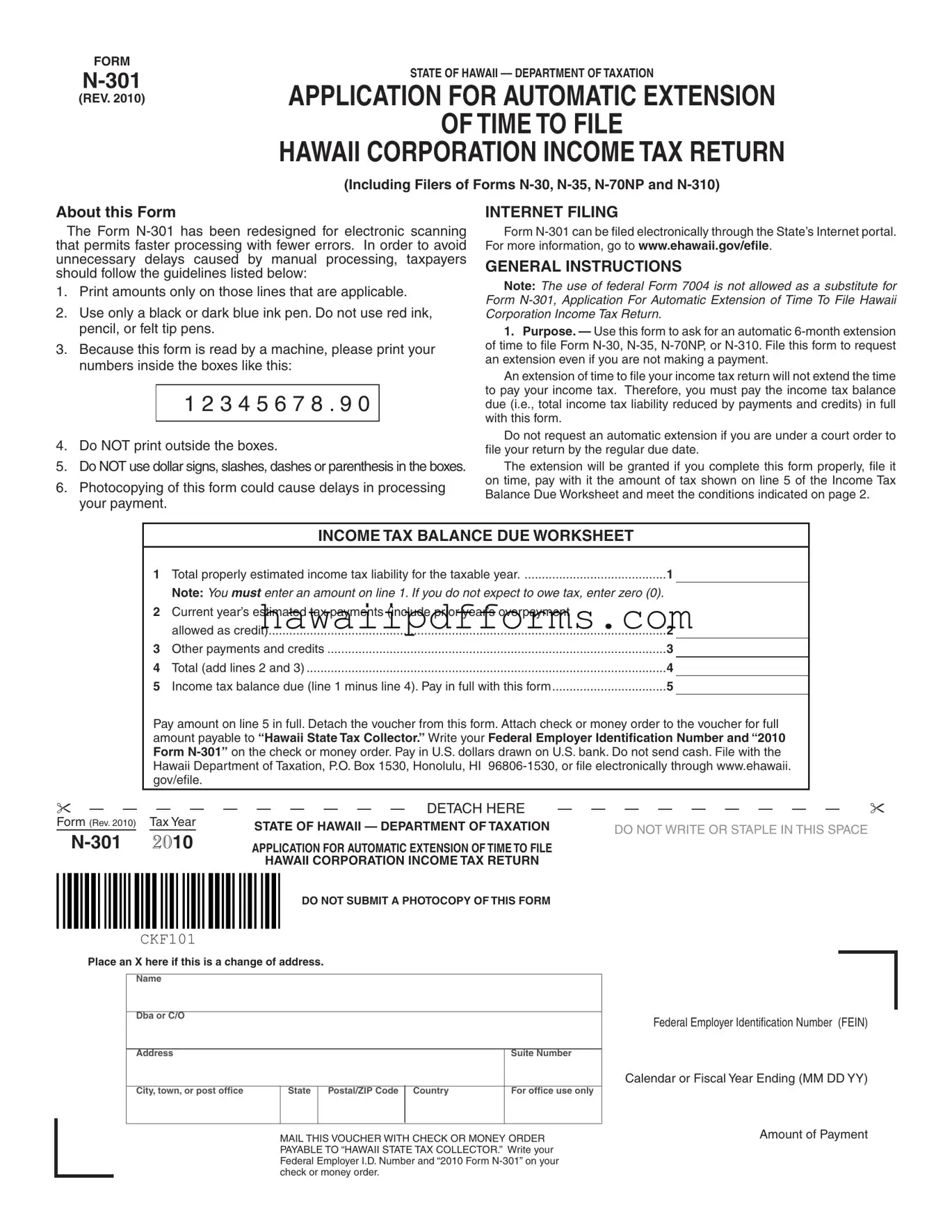

When it comes to managing corporate financial responsibilities in Hawaii, understanding the intricacies of Form N-301 is essential. This document, issued by the State of Hawaii Department of Taxation, serves as an application for an automatic extension of time to file Hawaii corporation income tax returns, including those for Forms N-30, N-35, N-70NP, and N-310. Redesigned to enhance electronic scanning, the form aims to streamline processing, reducing errors, and avoiding delays linked with manual processing. Taxpayers are instructed to print amounts in applicable lines using black or dark blue ink only, ensuring clarity for machine-reading without the need for manual correction. Notably, the form emphasizes that federal Form 7004 cannot substitute for N-301, underscoring the unique requirements for corporations operating within Hawaii. The form not only extends the filing period but stipulates that it doesn't prolong the time for tax payment, mandating the full payment of any due taxes alongside its submission. Electronic filing options are provided, offering convenience and further expediting the process. Moreover, specific guidelines are laid out for correctly estimating and paying taxes due, with detailed conditions for the extension to be granted, including a caveat that the extension period cannot exceed six months beyond the original due date. In essence, Form N-301 embodies a crucial compliance tool for corporations, ensuring they meet Hawaii's tax filing deadlines while providing a mechanism to manage their fiscal obligations effectively.

Document Example

FORM |

|

|

STATE OF HAWAII |

||

APPLICATION FOR AUTOMATIC EXTENSION |

||

(REV. 2010) |

OF TIME TO FILE

HAWAII CORPORATION INCOME TAX RETURN

(Including Filers of Forms

About this Form

The Form

1.Print amounts only on those lines that are applicable.

2.Use only a black or dark blue ink pen. Do not use red ink, pencil, or felt tip pens.

3.Because this form is read by a machine, please print your numbers inside the boxes like this:

1 2 3 4 5 6 7 8 . 9 0

4.Do NOT print outside the boxes.

5.Do NOT use dollar signs, slashes, dashes or parenthesis in the boxes.

6.Photocopying of this form could cause delays in processing your payment.

INTERNET FILING

Form

GENERAL INSTRUCTIONS

Note: The use of federal Form 7004 is not allowed as a substitute for Form

1.Purpose. — Use this form to ask for an automatic

An extension of time to file your income tax return will not extend the time to pay your income tax. Therefore, you must pay the income tax balance due (i.e., total income tax liability reduced by payments and credits) in full with this form.

Do not request an automatic extension if you are under a court order to file your return by the regular due date.

The extension will be granted if you complete this form properly, file it on time, pay with it the amount of tax shown on line 5 of the Income Tax Balance Due Worksheet and meet the conditions indicated on page 2.

|

|

|

INCOME TAX BALANCE DUE WORKSHEET |

|

|

|

|

|

|

1 |

Total properly estimated income tax liability for the taxable year |

1 |

|

|

|

||

|

|

Note: You MUST enter an amount on line 1. If you do not expect to owe tax, enter zero (0). |

|

|

||||

|

2 |

Current year’s estimated tax payments (include prior year’s overpayment |

|

|

|

|

||

|

|

allowed as credit) |

2 |

|

|

|

||

|

3 |

Other payments and credits |

3 |

|

|

|

||

|

4 |

Total (add lines 2 and 3) |

4 |

|

|

|

||

|

5 |

Income tax balance due (line 1 minus line 4). Pay in full with this form |

5 |

|

|

|

||

|

Pay amount on line 5 in full. Detach the voucher from this form. Attach check or money order to the voucher for full |

|

|

|||||

|

amount payable to “Hawaii State Tax Collector.” Write your Federal Employer Identification Number and “2010 |

|

|

|||||

|

Form |

|

|

|||||

|

Hawaii Department of Taxation, P.O. Box 1530, Honolulu, HI |

|

|

|||||

|

gov/efile. |

|

|

|

|

|

|

|

— — |

|

|

|

|

|

|

|

|

— |

— |

— — — — — — DETACH HERE |

— — — |

— — — — — — |

||||

Form (Rev. 2010) |

Tax Year |

STATE OF HAWAII — DEPARTMENT OF TAXATION |

DO NOT WRITE OR STAPLE IN THIS SPACE |

|

||||

|

|

|

|

|||||

2010 |

|

|

||||||

APPLICATION FOR AUTOMATIC EXTENSION OF TIME TO FILE |

|

|

|

|

|

|||

HAWAII CORPORATION INCOME TAX RETURN

DO NOT SUBMIT A PHOTOCOPY OF THIS FORM

CKF101

Place an X here if this is a change of address.

Name

Dba or C/O

Address |

|

|

|

Suite Number |

|

|

|

|

|

City, town, or post office |

State |

Postal/ZIP Code |

Country |

For office use only |

|

|

|

|

|

MAIL THIS VOUCHER WITH CHECK OR MONEY ORDER PAYABLE TO “HAWAII STATE TAX COLLECTOR.” Write your Federal Employer I.D. Number and “2010 Form

Federal Employer Identification Number (FEIN)

Calendar or Fiscal Year Ending (MM DD YY)

Amount of Payment

FORM |

|

(REV. 2010) |

PAGE 2 |

In no case shall the extension be granted for a period of more than 6 months beyond the prescribed due date of the return.

For extension requirement purposes, Hawaii does not conform to Treasury Regs. section

An automatic extension of time for filing a return shall be allowed upon the following two conditions:

• You complete this form properly, file it, and pay any or properly estimated balance due on line 5 of the Income Tax Balance Due Worksheet by the prescribed due date for the return for which the extension applies.

• Within the time specified by the automatic extension, the return shall be filed, accompanied by payment of the tax to the extent not already paid.

One hundred percent of the properly estimated tax liability must be paid on or before the prescribed due date of your return. Properly estimated tax liability means the taxpayer made a bonafide and reasonable attempt at the time the extension was submitted to locate and gather all of the necessary information to make a proper estimate of tax liability for the taxable year. Payment of properly estimated tax liability will be presumed if the tax still owing after the prescribed due date of the return is 10 percent or less of the total tax shown as due on the return.

The Director of Taxation may terminate the automatic extension at any time by mailing a notice of termination to the entity or to the person who requested the extension for the entity. The notice will be mailed at least 10 days prior to the termination date designated in the notice.

Note: Only those taxpayers whose automatic extension has been rejected will be notified by the Department of Taxation.

2.How To Obtain Tax Forms. — To request tax forms and publications by mail, you may call

Tax forms are also available on the Internet. The Department of Taxation’s site on the Internet is: www.hawaii.gov/tax.

3.When to File. — File one copy of this application on or before the prescribed due date of the entity’s income tax return. If the prescribed due date falls on a Saturday, Sunday, or legal holiday file by the next regular workday.

You may file the applicable income tax return any time before the

4.Where to File. — File Form

5.Consolidated Returns. — If a consolidated return is to be filed, a parent corporation may request automatic extensions for itself and its

subsidiaries by filing one Form

6. How to Fill Out This Form.

• Enter the corporation’s name and address on the appropriate lines. • Using black or blue ink, enter the corporation’s FEIN, the date of

the end of the tax year, and the amount of the payment in the space provided.

• If no payment is being made with this form, enter “0.00” in amount of payment space.

• It is suggested that you make a photocopy of this form for your records before you detach the voucher. Do not, however, submit a photocopy of this form.

• Detach the voucher where indicated. Submit only the voucher portion of this form with your payment.

• Attach your check or money order payable to “Hawaii State Tax Collector” to the front of the voucher. Write your FEIN and “2010 Form

7.Making a Payment. — If a payment is being made with this form, make your check or money order payable to “Hawaii State Tax Collector.” Write your FEIN and “2010 Form

8.How to Claim Credit for Payment Made With This Form. — Show the amount paid (line 5) with this form on the applicable income tax return.

9.Penalties

Late Filing of Return. — The penalty for failure to file a return on time is assessed on the tax due at a rate of 5% per month, or part of a month, up to a maximum of 25%.

Failure to Pay After Filing Timely Return. — The penalty for failure to pay the tax after filing a timely return is 20% of the tax unpaid within 60 days of the prescribed due date. The

These penalties are in addition to any interest charged on underpayment or nonpayment of tax.

10.Interest. — Interest at the rate of 2/3 of 1% per month or part of a month shall be assessed on unpaid taxes and penalties beginning with the first calendar day after the date prescribed for payment, whether or not that first calendar day falls on a Saturday, Sunday, or legal holiday. Form

REASONS FOR REJECTION OF EXTENSION

1. The request was not in this office or mailed on or before the date prescribed by law for filing this return.

2. Separate requests are required for each type of tax and for each taxpayer involved.

3. The income tax return was not filed within the time specified by the automatic extension.

Document Characteristics

| Fact Name | Detail |

|---|---|

| Applicable Forms | This form applies to filers of Forms N-30, N-35, N-70NP, and N-310 needing an extension for filing Hawaii corporation income tax returns. |

| Automatic Extension Duration | Form N-301 grants an automatic 6-month extension of time to file the specified Hawaii corporation income tax returns. |

| Filing Medium Options | The form can be filed electronically through the State of Hawaii’s Internet portal, in addition to the traditional mailing option. |

| Payment Instructions | If a payment is due, it should be made in full with the form, payable to “Hawaii State Tax Collector” with the FEIN and “2010 Form N-301” noted on the check or money order. |

| Governing Law | For extension requirement purposes, Hawaii does not conform to Treasury Regs. section 1.1502-76 but allows an extension beyond 6 months under specific circumstances for corporations filing a short year federal return. |

Guidelines on Utilizing N 301 Hawaii

Filing the N-301 Hawaii form is a necessary step for corporations seeking an extension on their income tax return filing deadline. Careful adherence to the detailed instructions ensures a smooth process, minimizing errors and delays. The following guidelines have been crafted to assist in accurately completing and submitting the form to avoid common pitfalls and to ensure that the request for an extension is processed efficiently.

- Ensure to only print amounts on applicable lines utilizing black or dark blue ink pen for clear readability and to avoid processing issues.

- Do not use red ink, pencil, or felt tip pens as the form is designed for electronic scanning which might not accurately capture these mediums.

- When entering numbers in boxes, print clearly within the confines to prevent misreads by scanning machinery. Example format should follow: 1 2 3 4 5 6 7 8 . 9 0, avoiding any characters outside the designated boxes.

- Avoid using dollar signs, slashes, dashes, or parenthesis in the boxes to ensure the machine can accurately process the form.

- If applicable, the option for electronic filing via the State’s Internet portal should be considered for a more streamlined submission process. Visit www.ehawaii.gov/efile for more information.

- Upon completion, detach the voucher part of the form if a payment is being made. Attach a check or money order payable to “Hawaii State Tax Collector” for the full amount owed. Ensure the Federal Employer Identification Number (FEIN) and “2010 Form N-301” are written on the check or money order.

- Submit the voucher and payment to the Hawaii Department of Taxation at P.O. Box 1530, Honolulu, HI 96806-1530, or choose to file electronically through the suggested internet portal.

- For those not making a payment with the form, enter “0.00” in the amount of payment space, ensuring the form is still submitted by the due date to request the filing extension.

It's important to submit the form by the prescribed due date to avoid any penalties or interest on late payments which do not cease with the filing of an extension request. An extension grants additional time to file the income tax return but not an extension of time to pay any owed taxes. Ensure all sections are completed accurately and that any payment due with the form is made to prevent unnecessary delay or rejection of the extension request.

Understanding N 301 Hawaii

Frequently Asked Questions (FAQ) about Form N-301, Application for Automatic Extension of Time to File Hawaii Corporation Income Tax Return

- What is Form N-301 used for?

Form N-301 serves as a request for an automatic 6-month extension of time to file certain Hawaii corporation income tax returns, specifically forms N-30, N-35, N-70NP, and N-310. This extension allows corporations more time to gather necessary documents and information to prepare their tax returns. However, it's crucial to note that this extension pertains only to filing the return, not to the payment of taxes due.

- Can federal Form 7004 be used in place of Form N-301 for Hawaii extensions?

No, federal Form 7004 cannot be substituted for Form N-301 when requesting an automatic extension to file a Hawaii corporation income tax return. Hawaii has its own requirements and form for this purpose.

- Is there a penalty for not using Form N-301 correctly?

Yes, delays in processing might occur if the form is not filled out correctly. For instance, using the wrong ink color or photocopying the form can lead to these delays. To ensure smooth processing, it is advised to follow the specified guidelines such as using black or dark blue ink and not photocopying the form.

- How can I file Form N-301?

Form N-301 can be filed electronically through the State's Internet portal or by mailing it to the Hawaii Department of Taxation. Electronic filing is encouraged for faster processing with fewer errors. Detailed instructions for electronic filing can be found at www.ehawaii.gov/efile.

- When is Form N-301 due?

This form must be filed on or before the prescribed due date of the entity’s income tax return. If the due date falls on a weekend or legal holiday, the form should be filed by the next regular workday. Filing by the correct date ensures the automatic extension is granted.

- How do I make a payment with Form N-301?

If you owe income tax, the estimated balance due should be paid in full with Form N-301. Payments should be made by check or money order payable to "Hawaii State Tax Collector," and the payment should be attached to the detached voucher portion of the form. Remember to include the corporation's Federal Employer Identification Number (FEIN) and the form number on the payment.

- What if I make a mistake estimating the tax liability?

Estimating your tax liability accurately is important. If you underestimate, you might face interest and penalties. However, the extension will be considered valid if at least 90% of the actual tax due is paid by the original due date. It's always better to overestimate than underestimate your tax liability.

- Can a consolidated return request an extension using Form N-301?

Yes, if filing a consolidated return, the parent corporation can file a single Form N-301 to request extensions for itself and its subsidiaries. An attachment listing the name, address, and FEIN of each subsidiary for which the extension is requested must be included.

- What are the penalties for late filing or payment?

Late filing of the return after the extension period has expired incurs a penalty of 5% per month on any unpaid tax, up to a maximum of 25%. There's also a separate penalty for failing to pay the tax amount due within 60 days of the return's prescribed due date, which is 20% of the unpaid tax. Additional interest charges apply to both unpaid taxes and penalties.

Common mistakes

When completing the Form N-301 for Hawaii, individuals often make mistakes that can affect the processing time and accuracy of their application for an automatic extension of time to file their Hawaii Corporation Income Tax Return. Being aware of common errors can help ensure that the process goes smoothly. Here are the most frequent mistakes to avoid:

- Not using black or dark blue ink: The form specifies that all entries should be made using only black or dark blue ink. Using other colors or pencil can lead to read errors by the scanning machines.

- Failing to print numbers inside the boxes: Numbers should be printed clearly within the designated boxes. If numbers extend outside the boxes, it may be difficult for the electronic scanning systems to read them correctly.

- Using prohibited characters: Dollar signs, slashes, dashes, or parenthesis are not permitted in the boxes. These can cause confusion or errors during processing.

- Submitting a photocopy of the form: Photocopied forms may not scan as well as the original, leading to processing delays. Always submit the original form provided by the Department of Taxation.

- Incorrectly calculating the income tax balance due: It's important to accurately calculate and enter the income tax balance due on line 5 of the Income Tax Balance Due Worksheet. This involves correctly estimating your income tax liability and subtracting your payments and credits.

- Not attaching the check or money order to the voucher: If making a payment with the form, the check or money order should be attached to the voucher portion of Form N-301. This ensures your payment is processed accurately and in a timely manner.

- Omitting the Federal Employer Identification Number (FEIN) on the check or money order: Your FEIN and the form number "2010 Form N-301" should be written on the payment to correctly associate it with your form submission.

- Attempting to file using an incorrect method: Ensure that you are filing the form either through the recommended electronic portal or by mailing it to the correct address as specified. Using outdated or incorrect filing methods can lead to delays.

Avoiding these common mistakes can help streamline the process of requesting an automatic extension for filing your Hawaii Corporation Income Tax Return, ensuring that your application is processed efficiently and accurately.

Documents used along the form

When dealing with corporate tax filings in Hawaii, Form N-301 is crucial for securing an automatic extension for filing income tax returns. However, this form doesn't operate in isolation. To ensure full compliance with tax regulations and to streamline the process, various other forms and documents often accompany Form N-301. Let's take a closer look at several of these important documents.

- Form N-30: This is the Hawaii Corporation Income Tax Return form. It's the primary form corporations use to report their income tax to the state. For those seeking an extension via Form N-30, it's essential that it be filed after receiving the extension.

- Form N-35: Used by Hawaii's S corporations, this form serves to report income, deductions, and credits of the corporation. It is similar to Form N-30 but tailored for the S corporation tax structure. Form N-70NP: This form is designated for nonprofit organizations claiming exemption from Hawaii's income tax. Nonprofits utilize this form to maintain compliance while claiming their exempt status.

- Form N-310: This form is used to pay estimated tax for corporations. For corporations that must make quarterly payments, this document is necessary for managing installments throughout the tax year.

- Income Tax Balance Due Worksheet: Found within the N-301 form instructions, this worksheet helps corporations calculate the total income tax liability due. This calculation is crucial for determining the amount that should be paid with the N-301 form if an extension is filed.

- Check or Money Order: While not a form, submitting a check or money order for any taxes owed with the Form N-301 is necessary. Ensuring that the correct amount is paid and that the payment is properly attached to the voucher section of Form N-301 is crucial for successful processing.

- Letter of Explanation: If filing under a short year or under specific circumstances that need clarification, a letter of explanation attached to the front of the Hawaii return when it is filed can provide necessary context to the Hawaii Department of Taxation.

Understanding and preparing these documents in concert with Form N-301 can significantly ease the process of filing for a tax extension and ensure compliance with Hawaii's tax regulations. Each document serves a specific purpose in the broader context of tax administration, offering a structured way for corporations to navigate their fiscal responsibilities while meeting regulatory requirements.

Similar forms

The N-301 Hawaii form, designed for requesting an automatic extension of time to file various Hawaii Corporation Income Tax Returns, holds similarities with other documents related to the tax extension filing process; however, its strict stipulations and specialized purpose set it apart, emphasizing the necessity for precise and timely submissions tailored to Hawaii's tax code. Among these documents, two noteworthy forms include the IRS Form 4868 and the IRS Form 7004, each catering to different subsets of tax filers but serving a similar overarching goal.

IRS Form 4868 serves as the Application for Automatic Extension of Time To File U.S. Individual Income Tax Return. Similar to the Hawaii N-301 form, Form 4868 allows taxpayers to obtain a six-month extension to file their federal income tax returns. Both forms necessitate the taxpayer's estimation of taxes owed and stress timely submission to avoid penalties. However, while N-301 is specific to corporations within Hawaii, including those needing to file forms like N-30 or N-35, Form 4868 caters to individual taxpayers. The focus on individual rather than corporate filers marks a delineation between these forms, though their functional intent—to affording additional time for accurate tax return completion—remains consistent.

IRS Form 9004, or the Application for Automatic Extension of Time To File Certain Business Income Tax, Information, and Other Returns, closely parallels the N-301 form in its target demographic of corporations and businesses requiring extra time to compile and submit their tax documentation. Essential similarities include the provision for a six-month filing extension and the requirement for an estimated tax liability to be paid by the original due date. Where they diverge is in their scope of applicability; IRS Form 7004 encompasses a broad range of business entities and tax situations on a federal level, whereas the N-301 is uniquely tailored to Hawaii's state tax obligations for corporations, underscoring the form's specificity to regional fiscal mandates.

Dos and Don'ts

When it comes to filling out the Form N-301 for an automatic extension of time to file Hawaii Corporation Income Tax Return, taking the right steps can help ensure a smooth process. Here are some essential do's and don'ts to keep in mind:

- Do print amounts only on lines that apply to your situation. It’s important to keep your form as clean and accurate as possible.

- Do use a black or dark blue ink pen to ensure the machinery can read your form correctly.

- Do make sure to print your numbers clearly inside the boxes to avoid any processing delays due to illegibility.

- Do file Form N-301 electronically via the state's Internet portal if you can, for faster processing.

- Do pay any tax balance due shown on line 5 of the Income Tax Balance Due Worksheet in full with this form.

- Don’t use red ink, pencil, or felt tip pens, as these can cause processing errors.

- Don’t print outside the boxes, use dollar signs, slashes, dashes, or parentheses, to prevent confusion during processing.

- Don’t submit a photocopy of this form, as photocopies could delay processing.

- Don’t ignore the requirement to also pay the estimated tax liability; an extension to file is not an extension to pay any taxes due.

Remember, properly filing Form N-301 by its due date, and paying any taxes owed, will help avoid penalties and interest. Ensuring your form is readable, accurate, and complete can lead to a smoother extension process.

Misconceptions

When it comes to filing tax documents, it's easy for myths and misconceptions to take root, especially for forms like the N-301 in Hawaii. Here's a closer look at some common misunderstandings:

Substitute federal forms can be used in place of Form N-301. This is incorrect. Hawaii's Form N-301 is mandatory for requesting an automatic extension for corporate income tax returns, and a federal Form 7004 cannot be used as a substitute.

Electronic filing isn't an option for Form N-301. Actually, Form N-301 can be filed electronically through Hawaii's online tax portal, offering a more efficient processing route than paper submissions.

Extensions extend the payment deadline. A common misconception is that filing Form N-301 extends the time to pay taxes due. However, the form only extends the time to file. Taxes owed must still be paid by the original deadline to avoid penalties.

Any writing implement is acceptable for filling out Form N-301. This is not the case. To ensure the form is readable by scanning systems, only black or dark blue ink pens should be used. Using other colors or pencils could lead to processing delays.

Photocopies of the form are acceptable for submission. Taxpayers should not submit photocopies of Form N-301. Photocopying can cause delays in processing, so always use the original form provided by the Department of Taxation or file electronically.

Dollar signs and other symbols are required when entering amounts. When completing Form N-301, taxpayers should not use dollar signs, slashes, dashes, or parentheses in the boxes. Such markings can interfere with the electronic scanning of the form.

You can request an extension at any time. An extension request must be filed on or before the due date of the tax return for it to be valid. Requests submitted after this deadline are not accepted, debunking the belief that extensions can be requested at any time.

Every corporation can apply for an extension. If a corporation is under a court order to file by the original deadline, it should not request an automatic extension. The extension is designed for those who can meet the criteria set out in the form's instructions, not for circumventing legal obligations.

Understanding these points clarifies the process and ensures that corporations can file Form N-301 correctly, avoiding common pitfalls and misconceptions.

Key takeaways

Understanding the N-301 Hawaii Form: Key Takeaways

The Form N-301 is crucial for businesses in Hawaii seeking an automatic 6-month extension to file their income tax returns. It's designed to streamline processing and minimize errors. Here are ten key points to consider:

- Ensure to print amounts only on relevant lines using black or dark blue ink to avoid processing delays. Avoid red ink, pencil, or felt tip pens.

- Machine readability is pivotal; numbers should be printed clearly inside the boxes without extending outside or including symbols like dollar signs or slashes.

- Photocopies of the Form N-301 may lead to processing delays, emphasizing the importance of submitting original forms.

- The form allows for electronic filing via the state’s internet portal, offering a convenient and faster alternative to paper filing.

- It's not permitted to use federal Form 7004 as a substitute for the N-301, highlighting the specificity required for Hawaii corporation income tax return extensions.

- Filing the Form N-301 grants an automatic extension but does not extend the time to pay income tax due; thus, any outstanding balance should be paid with the form to avoid penalties.

- For a successful extension, the form must be correctly completed, filed on time, accompanied by the correctly estimated tax due if applicable, and under no court orders that prevent delay.

- Extensions beyond 6 months are not permitted, and corporations must adhere to strict guidelines, especially those filing for a short year.

- Corporate taxpayers are encouraged to file their tax returns within the 6-month extension period with any remaining tax balance to avoid termination of the extension or additional penalties.

- The form also stipulates the importance of accurate tax liability estimation and adherence to due dates, with specific guidance on how to obtain forms, filing deadlines, and payment instructions to ensure compliance and avoid penalties and interest charges.

Create Common PDFs

Hawaii T1 - The Hawaii T1 application requires applicants to clearly print or type in black ink for legibility.

Divorce Papers Hawaii - Apart from finances, it includes directives on personal belongings, household effects, and other tangible assets.