Legal Promissory Note Template for Hawaii

For anyone entering into a financial agreement in Hawaii, understanding the Hawaii Promissory Note form is crucial. This legal document plays a pivotal role in laying out the terms involving loans or credit between parties — detailing the amount borrowed, repayment schedule, interest rates, and what happens if the borrower fails to repay. It not only provides a clear and structured plan for repayment but also serves as a legally binding commitment between the lender and borrower. Often used for personal loans, real estate transactions, and business capital, this form is designed to protect both parties involved. It covers essential elements such as the identities of the lender and borrower, co-signer information if applicable, collateral security, and any applicable legal considerations specific to Hawaii's laws. The Hawaii Promissory Note form ensures transparency, reduces misunderstandings, and helps manage financial risks effectively.

Document Example

Hawaii Promissory Note Template

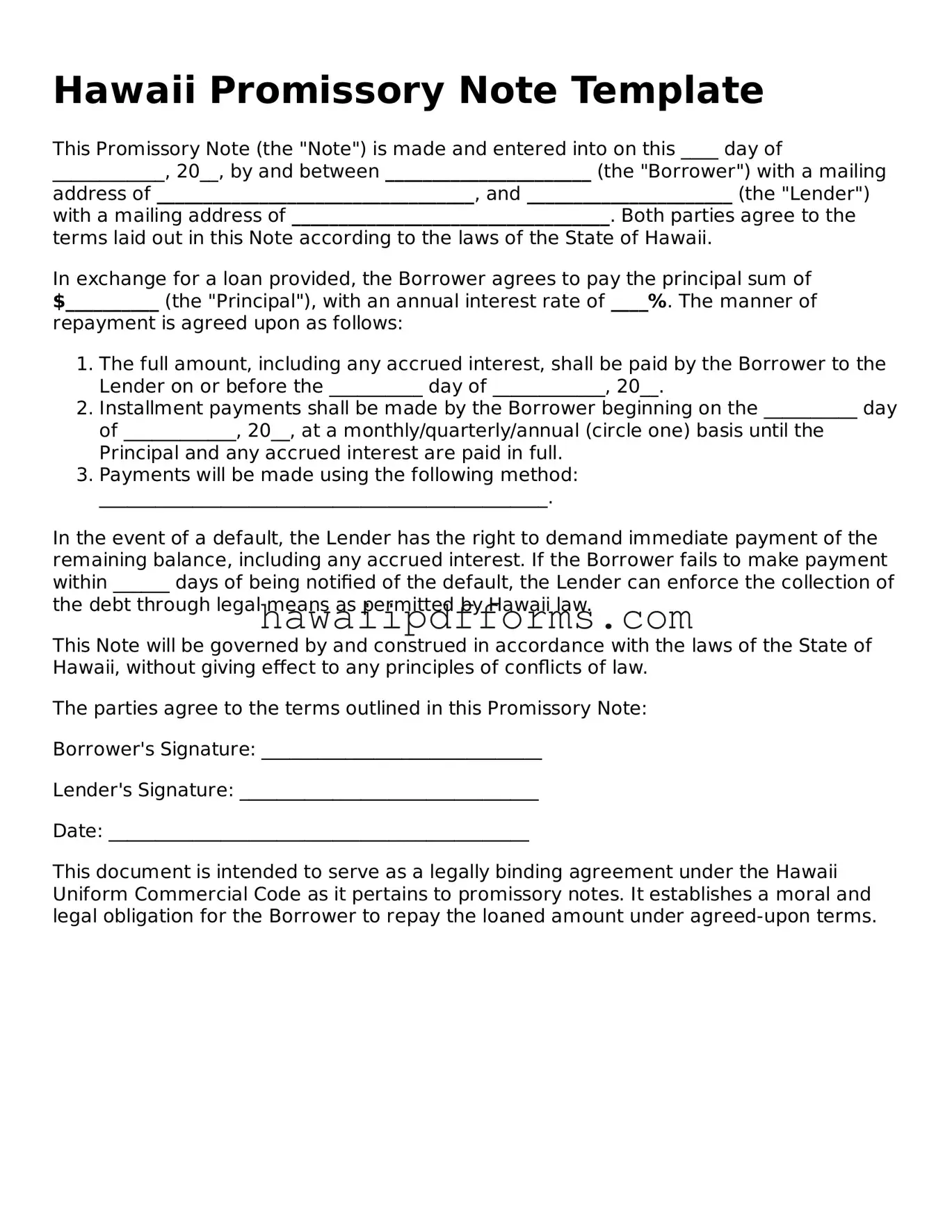

This Promissory Note (the "Note") is made and entered into on this ____ day of ____________, 20__, by and between ______________________ (the "Borrower") with a mailing address of __________________________________, and ______________________ (the "Lender") with a mailing address of __________________________________. Both parties agree to the terms laid out in this Note according to the laws of the State of Hawaii.

In exchange for a loan provided, the Borrower agrees to pay the principal sum of $__________ (the "Principal"), with an annual interest rate of ____%. The manner of repayment is agreed upon as follows:

- The full amount, including any accrued interest, shall be paid by the Borrower to the Lender on or before the __________ day of ____________, 20__.

- Installment payments shall be made by the Borrower beginning on the __________ day of ____________, 20__, at a monthly/quarterly/annual (circle one) basis until the Principal and any accrued interest are paid in full.

- Payments will be made using the following method: ________________________________________________.

In the event of a default, the Lender has the right to demand immediate payment of the remaining balance, including any accrued interest. If the Borrower fails to make payment within ______ days of being notified of the default, the Lender can enforce the collection of the debt through legal means as permitted by Hawaii law.

This Note will be governed by and construed in accordance with the laws of the State of Hawaii, without giving effect to any principles of conflicts of law.

The parties agree to the terms outlined in this Promissory Note:

Borrower's Signature: ______________________________

Lender's Signature: ________________________________

Date: _____________________________________________

This document is intended to serve as a legally binding agreement under the Hawaii Uniform Commercial Code as it pertains to promissory notes. It establishes a moral and legal obligation for the Borrower to repay the loaned amount under agreed-upon terms.

Form Specs

| Fact Number | Description |

|---|---|

| 1 | A Hawaii Promissory Note is a written promise to pay a specific sum of money to someone within a set period of time. |

| 2 | This form is governed by the laws of the State of Hawaii. |

| 3 | It can be either secured or unsecured. A secured note requires collateral, while an unsecured note does not. |

| 4 | Interest rates on these notes must comply with Hawaii's usury laws to avoid being deemed illegal. |

| 5 | The parties involved in the note must include their names and addresses for identification. |

| 6 | The amount of money being borrowed, along with the interest rate, must be clearly stated in the document. |

| 7 | Payment schedule details including the due dates, amount of each payment, and the total number of payments should be included. |

| 8 | In case of default, the note should specify the consequences and any potential for acceleration of payment. |

| 9 | Both the borrower and the lender must sign the note for it to be considered valid and enforceable. |

| 10 | If the promissory note is secured, a separate security agreement describing the collateral may be necessary. |

Guidelines on Utilizing Hawaii Promissory Note

Filling out the Hawaii Promissory Note form is an important step in formalizing a loan between two parties. This document establishes the borrower's promise to pay back the lender under agreed-upon terms, including the loan amount, interest rate, repayment schedule, and any other conditions relevant to the agreement. Accuracy and attention to detail are critical when completing this form to ensure that both the lender and borrower clearly understand their obligations and rights under the loan agreement. Here's a step-by-step guide to help you accurately fill out the Hawaii Promissory Note form.

- Date the Document: Start by entering the date at the top of the form. This marks when the promissory note becomes effective.

- Identify the Parties: Write the full legal names and addresses of the borrower and lender. Confirm that the information is correct to avoid any disputes about the identities of the parties involved.

- Loan Amount: Clearly state the principal amount being loaned. Ensure this figure is accurate, as it is the base amount the borrower is agreeing to repay.

- Interest Rate: Enter the agreed-upon annual interest rate. This should comply with Hawaii's usury laws to be legally enforceable.

- Repayment Terms: Describe the repayment terms in detail, including the schedule for payments (e.g., monthly), the amount of each payment, and when the first payment is due. Also, specify the final payment date when the loan must be paid in full.

- Security (if applicable): If the loan is secured with collateral, describe the collateral in detail. This could include real estate, vehicles, or other valuables that the lender can claim if the borrower fails to repay the loan.

- Signatures: Both the borrower and the lender must sign the promissory note. Witness or notary public signatures may also be required depending on the loan's nature and amount.

- Other Provisions: Include any additional terms or conditions relevant to the loan agreement. This may cover penalties for late payments, provisions for loan prepayment, or steps to be taken in case of default.

After completing the form, review it thoroughly to ensure all information is correct and that it accurately reflects the agreement between the lender and borrower. Each party should keep a copy of the signed document for their records. Remember, a well-constructed promissory note can help prevent misunderstandings and legal disputes down the line by clearly outlining the terms and conditions of the loan.

Understanding Hawaii Promissory Note

-

What is a Hawaii Promissory Note?

A Hawaii Promissory Note is a legal agreement used to document a loan between two parties in the state of Hawaii. It outlines the amount of money borrowed, the interest rate if applicable, the repayment schedule, and any other terms related to the loan. This document serves as a formal promise from the borrower to repay the amount under the agreed-upon conditions.

-

Is a Hawaii Promissory Note legally binding?

Yes, a Hawaii Promissory Note is considered a legally binding document when it is completed properly and contains the signatures of both the borrower and the lender. To enhance the enforceability of the note, having it notarized or witnessed can be beneficial. This document can be used in a court of law to ensure repayment according to the specified terms.

-

Are there different types of Promissory Notes in Hawaii?

Yes, there are mainly two types of Promissory Notes in Hawaii:

- Secured Promissory Note: This type of note is backed by the borrower's assets as collateral. If the borrower defaults on the loan, the lender has the right to claim the collateral to recover the outstanding debt.

- Unsecured Promissory Note: This version does not require collateral. If the borrower defaults, the lender's recovery options are limited to legal action to enforce the note and might include wage garnishment or attachment of the borrower's assets.

-

What key elements should be included in a Hawaii Promissory Note?

To ensure the promissory note is comprehensive and enforceable, the following details should be included:

- Date of the Note

- Names and addresses of the borrower and the lender

- Principal amount loaned

- Interest rate (if applicable)

- Repayment schedule (including due dates and amounts)

- Final due date for the repayment of the loan

- Signatures of both the borrower and the lender

For a secured note, a description of the collateral should also be included.

-

How can a lender enforce a Promissory Note in Hawaii if the borrower fails to repay the loan?

Should a borrower fail to fulfill the repayment terms outlined in a Promissory Note, the lender may take legal action to enforce the document. For secured loans, the lender can seize the collateral. For unsecured loans, the lender might seek a court judgment to garnish wages or place liens on the borrower’s property. It's advised to send a formal notice of default to the borrower before undertaking any legal proceedings.

Common mistakes

The Hawaii Promissory Note form is a valuable document for laying out the terms of a loan in a clear, legal framework. It spells out repayment details, interest rates, and the obligations of all parties involved. When filling out this form, it’s vital to avoid common pitfalls to ensure its validity and protect the interests of both the lender and borrower. Below are five common mistakes to watch out for:

-

Not Specifying the Type of Interest Rate: One common oversight is failing to clearly state whether the interest rate is fixed or variable. This distinction is crucial because it affects how interest accumulates over time and can significantly impact the borrower's payments.

-

Omitting Key Terms: Every promissory note should include specific terms such as the loan amount, interest rate, repayment schedule, and any late fees. Leaving out any of these details can lead to misunderstandings and legal complications down the line.

-

Ignoring State-Specific Legal Requirements: The state of Hawaii may have unique legal requirements or restrictions relating to promissory notes. For instance, there might be caps on interest rates or specific clauses that need to be included. It's a common mistake to overlook these state-specific requirements.

-

Lack of a Co-signer Agreement: If a co-signer is part of the agreement, failing to include their details and what their financial obligations are can be a critical mistake. The presence of a co-signer adds an extra layer of security for the lender, and their rights and responsibilities should be clearly documented.

-

Forgetting to Include a Clause on Defaults: It's essential to describe what constitutes a default and the steps that will follow one. This includes any grace periods, additional fees, or actions that will be taken to recover the owed amount. Neglecting to include this information can make it difficult for the lender to act in case of non-payment.

Avoiding these mistakes will help ensure that a Hawaii Promissory Note is legally binding and clear in its terms. This not only protects all parties but also minimizes the potential for future disputes.

Documents used along the form

When it comes to financial agreements, especially ones that involve lending money, a Hawaii Promissory Note Form is typically one part of the documentation needed to finalize the agreement. This form outlines the terms of the loan, including repayment schedule, interest rate, and the obligation of the borrower to repay the sum. Alongside this document, several other forms and documents are commonly used to ensure legal protection and clarity for both parties involved.

- Loan Agreement - A comprehensive contract that provides detailed information about the terms and conditions of the loan. It includes the obligations of both the borrower and the lender and serves as a more detailed document than the promissory note.

- Security Agreement - If the loan is secured, this document outlines the collateral that the borrower agrees to pledge as security for the loan. It details what happens if the loan is not repaid.

- Guaranty - A document where a third party agrees to be responsible for the debt if the original borrower fails to repay. This is often used in situations where the borrower's creditworthiness is in question.

- Amortization Schedule - A table detailing each periodic payment on a loan over time. It breaks down the amount going towards interest and the amount applied to the principal loan balance.

- Mortgage or Deed of Trust - For real estate transactions, this document places a lien on the purchased property as collateral for the loan. It outlines the rights and responsibilities of each party regarding the property.

- Late Fee Agreement - A document that specifies any fees or additional interest that will be applied to the loan for late payments. This ensures that the borrower is aware of the consequences of failing to make timely payments.

Utilizing these documents in conjunction with a Hawaii Promissory Note Form provides a robust framework for any loan transaction, ensuring all aspects are clearly outlined and legally binding. Each document plays a vital role in protecting the interests of both the lender and the borrower, making the lending process transparent and straightforward.

Similar forms

The Hawaii Promissory Note form is similar to other legal agreements and documents that facilitate financial transactions and the borrowing of money. This document specifically outlines the terms and conditions under which money is borrowed and the repayment plan. Similar documents include loan agreements, IOUs, and mortgage agreements. Each of these documents shares the common goal of providing a clear understanding between parties involved in a loan, yet they differ in terms of complexity, formality, and legal implications.

In particular, a loan agreement is quite similar to the Hawaii Promissory Note form. Both documents detail the amount of money loaned, the interest rate, and the repayment schedule. However, a loan agreement typically involves a more comprehensive outline of the terms and conditions, including clauses on default, governing law, and dispute resolution. This document is often used in more complex financial transactions and is accompanied by greater legal protections for both the lender and the borrower.

Another document, the IOU (I Owe You), also shares similarities with the Hawaii Promissory Note. An IOU is a simple, informal document that acknowledges a debt owed. While it details the borrower's name, the amount owed, and sometimes the repayment date, it lacks the legal and binding language found in promissory notes or loan agreements. IOUs are typically used for small, personal loans between individuals who have a mutual trust.

Finally, a mortgage agreement is related to the Hawaii Promissory Note but is specific to the financing of real property. This document not only outlines the loan amount, interest rate, and repayment terms but also secures the loan with the property itself. If the borrower fails to meet the repayment terms, the lender has the right to foreclose on the property. While a promissory note might be a part of the mortgage process, the mortgage agreement incorporates specific protections and conditions related to property transactions.

Dos and Don'ts

When filling out a Hawaii Promissory Note form, understanding the best practices can significantly impact the enforceability and clarity of the agreement. Below are essential dos and don'ts to guide you through the process.

Things You Should Do:

Include clear identification of both the lender and borrower, making sure to list their full legal names, addresses, and contact information to eliminate any ambiguity.

Specify the amount of money being borrowed and ensure that this amount is written in both words and figures for clarity and to prevent alterations.

Clearly define the repayment terms including the interest rate, payment schedule (monthly, quarterly), due dates, and the maturity date of the promissory note.

State the applicable interest rate, ensuring it complies with Hawaii’s legal usury limits to avoid rendering the note unenforceable.

Outline the consequences of late payments or default in detail, such as late fees or acceleration clauses, to inform both parties of their rights and obligations.

Sign and date the promissory note in the presence of a witness or notary public to enhance the document’s legal validity.

Things You Shouldn't Do:

Avoid using vague or ambiguous language that can lead to misunderstandings or disputes over the interpretation of the agreement.

Do not leave any sections incomplete; an incomplete form may be considered invalid or may not provide adequate legal protection.

Refrain from setting an interest rate above Hawaii's legal maximum to avoid the note being considered usurious and potentially void.

Never backdate or postdate the promissory note, as doing so could be construed as an attempt to mislead or commit fraud.

Avoid neglecting to specify what will constitute a default under the terms of the promissory note, as this ambiguity can complicate enforcement.

Do not bypass the step of having the note witnessed or notarized, depending on the requirements, as this could impact the enforceability of the document.

Misconceptions

When it comes to the Hawaii Promissory Note form, there are several misconceptions that can lead to confusion. Understanding these common mistakes can ensure individuals navigate these legal waters more accurately.

It's only for formal lending institutions: One common misunderstanding is that promissory notes are tools reserved exclusively for banks or formal lending institutions. However, in Hawaii, a promissory note can be used by anyone lending money, be it a friend, family member, or private lender. It's a versatile document that secures the terms of a loan, irrespective of the lender's identity.

It doesn't need to be witnessed or notarized: While Hawaii law does not mandate that a promissory note must be witnessed or notarized to be considered valid, having it notarized can add an extra layer of authenticity and could enforce its credibility if there's ever a dispute. Notarization ensures that the signatories of the document are indeed who they claim to be.

A verbal agreement can substitute for it: Relying solely on a verbal agreement in place of a written promissory note can be problematic. Verbal agreements are significantly more difficult to prove in court. A written promissory note, on the other hand, clearly outlines the loan's terms, including repayment schedule and interest rates, providing tangible evidence should issues arise.

It's too complicated to create without legal help: While seeking legal advice can be beneficial, especially for large loan amounts or complex agreements, drafting a promissory note in Hawaii does not require a lawyer. Plenty of resources and templates are available to help individuals prepare a promissory note that meets their specific needs. However, for peace of mind and ensuring all legal bases are covered, consulting with a professional may still be advisable.

Key takeaways

Understanding the Hawaii Promissory Note form is crucial for anyone engaging in lending or borrowing money in the state. This document serves as a legally binding agreement between a lender and a borrower, outlining the repayment terms for the loan. To ensure both parties are protected and understand their obligations, consider the following key takeaways:

- Ensure Accuracy: When filling out the Hawaii Promissory Note form, it’s essential to provide accurate and complete information. This includes the full names and addresses of both the lender and the borrower, the total amount of money borrowed, and the interest rate, if applicable.

- Understand Interest Rates: Hawaii law may have specific stipulations regarding interest rates. It is vital to understand these regulations to ensure that the interest rate on the promissory note is legal. Typically, the rate should not exceed the maximum allowed by law to avoid being deemed usurious.

- Repayment Terms: The promissory note should clearly specify the repayment terms, including the schedule for repayments (monthly, quarterly, or at another agreed interval), the due date for the first payment, and when the loan should be fully repaid. This clarity helps prevent misunderstandings and ensures both parties are aware of their commitments.

- Legal Obligations and Consequences: Both the lender and the borrower should understand the legal obligations and consequences outlined in the promissory note. This includes what happens in the case of a default by the borrower, such as late fees, acceleration of the loan, or legal action. Signing a promissory note is a serious commitment, and both parties should be fully aware of the terms and implications.

In summary, whether you are lending or borrowing money in Hawaii, the promissory note is a critical document that must be handled with care. Paying attention to the details and fully understanding the terms and conditions can help ensure a smooth financial transaction and avoid potential legal complications down the road.

Additional Hawaii Templates

Last Will Vs Living Will - Clarifying funeral arrangements and other final wishes can be included, relieving the family of making those difficult decisions.

Hawaii Divorce Laws - It can protect inherited assets or gifts from being subject to division, respecting the personal and familial significance of those items.

What's an Nda - Manufacturing agreements often come with NDAs to shield the specifics of product designs, formulas, and manufacturing techniques.